OK, I'm just seeing this now so I could be seriously misreading the article, but if I'm not, this is quite the eye-opener:

Virginia is on the cusp of expanding Medicaid to 400,000 low-income residents, after a veteran Republican state senator said Friday that he is willing to split with his party and help Democrats realize a goal they have been chasing for years.

Virginia state Sen. Frank Wagner (Virginia Beach) said he supports allowing more poor people to enroll in the federal-state healthcare program on two conditions.

He wants the plan structured so that Medicaid recipients do not suddenly lose coverage if their earnings rise. And he wants a tax credit or some other help for middle-income people who already have insurance but are struggling to pay soaring premiums and co-pays.

Earlier today I wrote an extensive post about California's individual market, specifically breaking out the number of off-exchange policies, including a rare look at some hard grandfathered plan enrollment numbers.

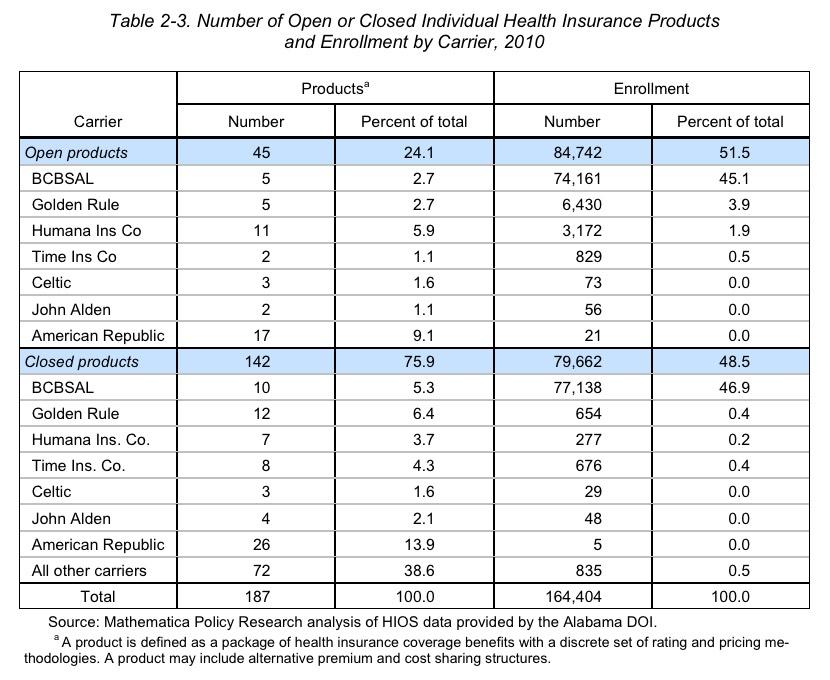

I've also managed to dig up a fascinating document from 2010 buried on the Alabama Insurance Department's website, which provides quite a bit of demographic insight into Alabama'soverall health insurance market. While all of this info is now 8 years out of date (and even precedes the first ACA open enrollment period), it does provide a few clues into estimating what's going on in Alabama today.

This first table shows exactly what Alabama's individual market looked like: 164,404 people were enrolled in pre-ACA "major medical" policies in 2010:

The California Health Care Foundation is a nonprofit philanthropic organization. From their About page:

The California Health Care Foundation is dedicated to advancing meaningful, measurable improvements in the way the health care delivery system provides care to the people of California, particularly those with low incomes and those whose needs are not well served by the status quo. We work to ensure that people have access to the care they need, when they need it, at a price they can afford.

A few days ago, I ran a comparison of the average unsubsidized (full price) 2018 premium increases for each state which I had projected last fall against a study last month by the Urban Institute in which they reported the actual average premium increases, by state, of some of the ACA policies available on the exchange. Urban wasn't able to examine every plan, but they did a full analysis on the Lowest Cost Silver, 2nd Lowest Cost Silver (benchmark plan) and Lowest Cost Gold policies in each market and statewide.

Urban's analysis concluded that depending on how you looked at their data, the overall national average increase was between 29-32% year over year...versus my own national projection of around 29.7%.

I didn't fare so well at the state level: I was within 5 percentage points of their actual averages in 31 states, and within 10 points in 6 more. I was way off in the other 14 for various reasons.

OK, I'm finally able to get back to digging into the meat of the FINALLY just-released 2018 Open Enrollment Report from the Centers for Medicare & Medicaid.

In Part 2, I'm looking at the actual 2018 Open Enrollment Period Public Use Files, which break out a ton of demographic info by state, county and even zip code depending on the state (some of it is available for all 50 states + DC, while other data is only available for the 39 states hosted by HealthCare.Gov).

First up: As I noted earlier today, there's around a 10,000 enrollee discrepancy between the national total I came up with back in early February and CMS's official total. I compared my state-by-state totals against CMS's report and found differences in 5 of the state-based exchanges:

NOTE: THIS IS A LIVE BLOG, SO CHECK BACK FREQUENTLY FOR UPDATES.

Yes, at long last (3 weeks later than last year, which itself was 4 days later than in 2016), the Centers for Medicare and Medicaid has finally released the official, final 2018 Open Enrollment Report.Let's dig in!

This report summarizes enrollment activity in the individual Exchanges during the Open Enrollment Period for the 2018 plan year (2018 OEP) for all 50 states and the District of Columbia. Approximately 11.8 million consumers selected or were automatically re-enrolled in Exchange plans during the 2018 OEP. An accompanying public use file (PUF) includes detailed state-level data on plan selections and demographic characteristics of consumers. The methodology for this report and detailed metric definitions are included with the public use file.

The Kaiser Family Foundation runs a widely-respected monthly natonal tracking poll about healthcare issues. The questions they ask sometimes change from month to month, and this month they asked a whole bunch of questions about...the Individual Market and the ACA exchanges. In other words, pretty much a bonanza of data-nuggety goodness for this site:

As part of the Republican tax reform plan signed into law at the end of 2017, lawmakers eliminated the ACA’s individual mandate penalty starting in 2019. About one-fifth of non-group enrollees (19 percent) are aware the mandate penalty has been repealed but is still in effect for this year. Regardless of the lack of awareness, nine in ten non-group enrollees say they intend to continue to buy their own insurance even with the repeal of the individual mandate. About one-third (34 percent) say the mandate was a “major reason” why they chose to buy insurance.

Republicans also want to use the funding bill to go after Obamacare. They would prohibit funding for administering or enforcing the health care law, prohibit the administration from collecting a fee from insurance companies to run the insurance exchanges and eliminate more than half a billion dollars in funding for managing the program at the Centers for Medicare and Medicaid Services.

(sigh) I'm not quite sure how "prohibiting funding for administration" differs from "eliminating funding for managing the program", but it amounts to the same thing: They're trying to shut down CMS's ability to actually run the ACA.

The good news is that none of that ended up making it into the omnibus bill.

Regular readers know that I've developed a tradition over the past three years of tracking the average unsubsidized premium rate increases for the ACA-compliant individual market, painstakingly poring over the rate filings for every carrier in every state and running a weighted average by their market share.

Every year there are numerous challenges and headaches which get in the way, including things as obvious as "not every carrier publishes the number of enrollees they have covered" to complex situations like "carrier X is dropping out of the on-exchange market in half the counties of the state but is sticking around in the off-exchange market". In addition, many carriers submit an initial rate request...followed a few months later by a revised one...neither of which might end up matching the final premium changes approved by state regulators. Sometimes there may be 2-3 more revised filings along the way which muddy the waters even further.