MASSACHUSETTS: The MA Health Connector allows for online premium payments (and in fact, payments have to be made to the exchange, not to the insurance company itself). The good news is that the website & billing system appear to be working properly this year, a vast improvement over last year's disaster. The bad news (or, odd news anyway) is that for some reason the system requires you to pay using only direct electronic fund transfers or a written check--it does not accept credit card payments!

I don't know if this is for technical reasons (which I doubt) or policy reasons (avoiding the 2.5% transaction fees or whatever), but it seems very odd to me.

HAWAII: Not only hasn't the HI Health Connector provided any enrollment updates since open enrollment started again on November 15th, they haven't even updated their enrollment report section since July 26th! Guys, either post an update or at least remove the link entirely; keeping it as is, locked in on 7/26 is just embarrassing.

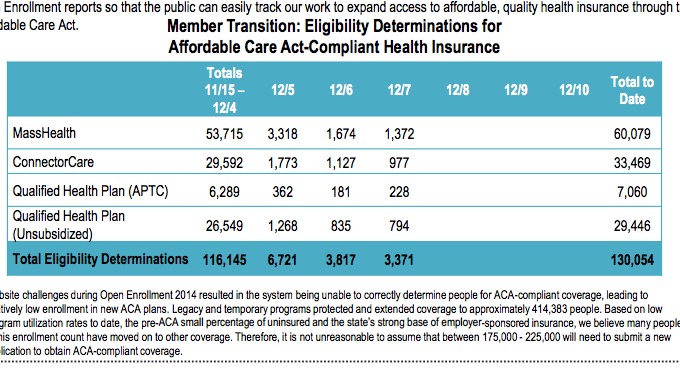

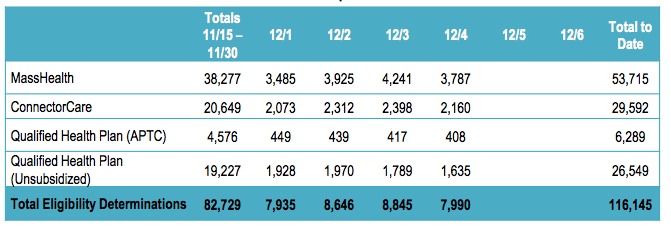

Hmmm...for some reason, the MA Health Connector chose to give a daily report today instead of the weekly report which they've been doing on Mondays.

On the one hand, this is OK because it still includes the daily breakdown of QHP determinations. On the other hand, the weekly reports gave the hard QHP selection numbers, which aren't included here.

I'm going to assume that the ratio of actual selections has moved up to around 60% over the weekend (from the 48-50% it was at earlier) as we move towards the January cut-off point. If so, that means that QHP selections in Massachusetts should now be well above the 2014 total (31,695) and should be somewhere around 36,400 as of last night:

Meanwhile, Medicaid (MassHealth) enrollments have broken the 60K mark; I've been informed that these are effective immediately.

I've projected that total QHP enrollments nationally hit around 1.57 million as of Friday (12/05) night (of which about 1.18 million should have been via HC.gov).

As of last night (Sunday the 7th), the totals should be roughly 1.74 million nationally (1.30 million HC.gov). Until now, enrollments nationally should have been averaging roughly 75-80K/day (except for a lull on Thanksgiving, of course).

As you can see on The Graph, however, I now expect things to start ramping up dramatically: Likely 200K/day for 9 days straight, hitting around 3.4 million manual enrollments via either renewals, re-enrollments or brand-new enrollments through the 14th.

Then, on December 15th, I'm expecting something like 3.5 million current enrollees to be auto-renewed all in one shot, plus another 200-300K manual enrollments that day alone, which should push the total well over the 7 million mark.

Last year, the Kaiser Family Foundation ran an in-depth report which broke out a rough estimate of how many people in each state fell into various ACA categories (Medicaid expansion, eligible for QHP tax credits, not eligible due to being an undocumented immigrant, "Medicaid Gap" and so on). Based on that report, it looked like the total number of currently (at that time) uninsured people eligible for Medicaid--whether via expansion or "woodworker" status--was around 14 million, plus another 4.8 million who fell into the Medicaid Gap for non-expansion states.

New Hampshire's ACA Medicaid expansion program got a late start, not kicking off until July 1st of this year. That makes the fact that they've already reached 50% of their total potential enrollment all the more impressive:

State officials had expected 30,000 to 40,000 of the estimated 50,000 eligible adults would sign up in the first year either through the state's managed care program for Medicaid or a program that subsidizes existing employer coverage. As of mid-week, just fewer than 25,300 had signed up.

OK, the headline and lede paragraph are pretty lame since they make it sound like Oregon's OE2 enrollment is down 90% from last year. This is pretty stupid, of course, since it only covers the first 2 weeks of a 93-day enrollment period, and since there will obviously be a huge spike in enrollments late next week and then again in mid-February.

Still, this is the first hard 2015 enrollment data I've seen for Oregon, and it's especially interesting given a) Oregon's disastrous 2014 exchange experience and b) the subsequent move to Healthcare.Gov this time around (I have yet to see a similar story about Nevada, but will be on the lookout for it):

Cover Oregon officials say just 7,200 Oregonians had selected a private health insurance plan through the federal portal by the end of November.

The article also gives a current update on the 2014 off-season/attrition situation:

About 77,000 Oregonians were enrolled through Cover Oregon in 2014. A total of 105,000 actually enrolled but some dropped off due to cancellations and terminations.

As a bonus, this is also pretty much the first hard off-exchange data I have this year:

Another day, another 2,300 (estimated) QHP selections for Massachusetts. Assuming I'm right about that number (or even close to it), that means their total should now sit at around 31,750.

As I noted yesterday, Massachusetts has already reached their 2014 Open Enrollment Period total...in just 20 days.

At the current pace, MA is now on track to hit a bare minimum of 148K QHPs, without taking into account the double-surges around 12/23 and 2/15 to come.

Maryland just released their second official 2015 Open Enrollment report, and the numbers continue to impress:

As of Dec. 4, a total of 51,796 Marylanders have enrolled in quality, affordable health coverage for calendar year 2015 since the 90 day open enrollment period began Nov. 15. This includes 29,543 individuals enrolled in private Qualified Health Plans and 22,253 individuals enrolled in Medicaid.

From Nov. 15 to Dec. 4, 62,713 consumer accounts were created; 66,752 calls were made to the Consumer Support Center and 339,578 individuals visited the MarylandHealthConnection.gov website.

Marylanders must enroll or renew their plans by Dec. 18 for insurance that starts New Year’s Day. Open enrollment for 2015 ends Feb. 15.

For comparison, during the 2014 OE period, MD enrolled 67,757 people. They're already at 43.6% of that in just 20 days this time around.