*(OK, that's hyperbole...unsubsidized enrollees are still left holding the bag for thousands of dollars in unnecessary premium payments for at least another year or so, and there's still no guarantee of the final ruling...see below...)

Almost exactly a year ago, Donald Trump, after 9 months of bluster about doing so so, finally pulled the trigger on his threat to cut off Cost Sharing Reduction reimbursement payments to insurance carriers for the deductibles, co-pays and other out-of-pocket expenses which they agree to cover every month for around 7 million low-income ACA exchange policy enrollees.

Trumps stated goal in doing so was, of course, to "blow up" the ACA, to cause it to "implode" (which is actually the opposite of blowing something up, but that's a different discussion) and ultimately fail in the process.

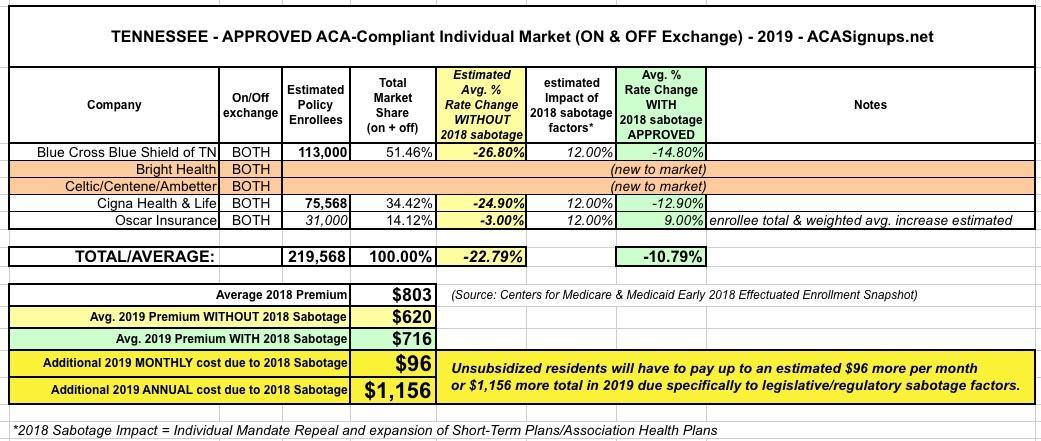

When I last posted about 2019 ACA-compliant individual market premium changes in Tennessee back in August, I noted that premiums statewide had gone from dropping 5.7% to dropping 10.8% on average after the Trump Administration first stated that they were going to unnecessarily "freeze" the ACA's Risk Adjustment fund transfers in response to a lawsuit ruling only to reverse themselves a week or so later and state that they were going to go ahead and process RA fund transfers after all.

In other words, the Trump Administration once again deliberately caused a panic across the industry only to "save" the industry from the very threat which they had posed in the first place.

In any event, here's what I thought the Tennessee's premium situation looked like when the dust settled:

Back in August, Blue Cross Blue Shield of South Carolina, the only carrier offering policies on SC's individual insurance market, asked for a 9.2% average premium rate increase for 2019 statewide. This consisted of 9.3% for their most popular plans (which cover over 200,000 South Carolinans) and 6.9% for 6,800 BlueChoice plan enrollees (BlueChoice is only available off-exchange).

2019 PRELIMINARY HEALTH INSURANCE PLANS RATE CHANGES FOR INDIVIDUAL MARKET COVERAGE

The SCDOI has approved the rates and forms for health insurance issuers that are planning to offer ACAcompliant products in the individual market in 2019.

Most Connect for Health Colorado® Customers Will See Decrease in Premiums for 2019 as Marketplace Stabilizes

DENVER — With rate increases lower than the state has seen in years, Connect for Health Colorado® customers who qualify for financial help are looking at an average decrease in their net (after tax credit) premium of 24 percent next year.

The Colorado Division of Insurance today issued final approval for individual health insurance plans that will increase by an average of 5.6% in 2019. The relatively small increase in monthly premiums and the return of all seven health insurance companies to the Connect for Health Colorado, the state’s health insurance Marketplace, are signs of a stabilizing market for Coloradans who buy their own health insurance coverage.

I just received the following press release from the Iowa Insurance Division...

2019 Health Insurance Enrollment Deadline Approaches

Des Moines – Open enrollment begins November 1 and ends December 15 for Iowans purchasing or changing their Affordable Care Act (ACA) individual health coverage to become effective January 1, 2019.

“As the open enrollment season begins, Iowans should thoroughly research all coverage options. The ACA-compliant insurance market is available to Iowans, however, most Iowans have been priced out of that market if they are not currently receiving federal subsidies to help pay premiums and, in some instances, deductibles. I would encourage consumers to meet with a licensed insurance agent to determine the best plan for themselves and their families,” Iowa Insurance Commissioner Doug Ommen said. “Changes made at the Iowa state legislature and by the federal government have provided a few more options in addition to ACA-compliant coverage for Iowans to review as they plan out their health needs for 2019.”

UPDATE 3:50pm: OK, it sounds like you can completely disregard all the Medicaid-related stuff below; apparently there was a communication error. I've confirmed with the Whitmer campaign that the proposed reinsurance plan would not be tied in with Michigan's ACA Medicaid expansion program at all, nor would it have any impact on the Medicaid eligigibility threshold, which means this would indeed be a standard ACA individual market reinsurance program after all...which is what I assumed in the first place, and which would be perfectly fine!

I probably won't have any other blog posts today as I'm off to Lansing, Michigan this morning to attend this:

The fight to stop health care repeal isn’t over yet — far from it. At stake right now: Higher costs. Medicaid. Medicare. Coverage for pre-existing conditions. Prohibitions on discrimination against women and people over age 50.

If you’re sick and tired of the Republican war on health care, join people across the country who are joining Protect Our Care’s nationwide bus tour. Make your voice heard at the Protect Our Care bus stop in Lansing.

Join us at the Michigan State Capitol in Lansing on Wednesday, October 3 to voice your opposition to Republicans’ repeal-and-sabotage agenda, which has cut health care coverage and driven up health care costs for millions.

Minnesota, currently entering their second year of their official reinsurance waiver program to help keep unsubsidized premiums down, announced their preliminary 2019 rate hikes way back in June. At the time, the carriers were looking at roughly an 8% average reduction in rates next year...although they would be dropping prices by more like 15% if not for the ACA's individual mandate being repealed and the expansion of #ShortAssPlans.

Today the Minnesota Dept. of Commerce posted the approved 2019 premium changes, and there's been some dramatic reductionsfor three of the five carriers offering policies in the state. Group Health and Medica were approved as is, but Blue Plus was told to drop their rates a whopping 27.7% instead of the 11.8% they were planning on. Ucare was shaved down from a 7 point reduction to 10 points, and PreferredOne (which only sells individual market policies off-exchange and only has 300 enrollees anyway) was knocked down from a 3-point reduction to 11 points.

The official annual ACA Open Enrollment Period (OEP) starting and ending dates have jumped around a lot since the exchanges kicked off back on October 1, 2013.

For the first OEP, people were given 6 months since the technology and the process were brand new to everyone...and thank God they were given the technical mess that the federal exchange (HealthCare.Gov) as well as many of the state-based exchanges experienced at launch. Things were eventually worked out, but not only was that extra time in spring 2014 vitally important, many people still needed some extra time beyond that as well. The official deadline to enroll for 2014 coverage was March 31, but the HHS Dept. gave people who had started their application by then an extra 15-day "overtime" period to complete the process.

For the 2015 OEP, the official dates were from November 15 - February 15th, cutting the time period down to three months. This time there was a one-week "overtime" period tacked onto the end.

For 2016 and 2017, HHS settled on November 1st - January 31st, which seemed to make sense since it was easier to remember: November, December, January.