A few days ago, Jonathan Cohn of the Huffington Post wrote about a new phenomenon sweeping the nation: Republican candidates, all of whom have repeatedly either voted to repeal the Patient Protection & Affordable Care Act or who have repeatedly called for it to be repealed, are suddenly falling all over themselves to try and claim that they support patient protections for those with pre-existing conditions...usually by invoking family members who suffer from various ailments.

Cohn's examples include GOP Congressman Mike Bishop (MI-08), who claims his wife has rheumatoid arthritis; Dana Rohrabacher (CA-48), who says his daughter survived childhood leukemia; John Faso (NY-19) and Mario Diaz-Balart (FL-25), both of whose wives survived cancer; and Josh Hawley (MO-AG, running for MO-Sen), whose son has a rare chronic disease.

Yes, that's right...while the 2019 Open Enrollment Period doesn't start for the rest of the country until November 1st, the Golden State has decided to kick things off two weeks early (16 days early, technically): Covered California, the largest state-based ACA exchange, is officially open for business for 2019 enrollment as of today!

In addition, while you can't actually enroll for 2019 coverage in any other state until November 1st, in several states you can window shop to find out what your 2019 policy options and pricing will be, along with estimates about what sort of financial assistance you'll qualify for once you actually do go through the enrollment process.

The states which are already open for window shopping already include:

UPDATE 10/30/18: Thanks to some additional reviews/checking by Dave Anderson, Louise Norris, Andrew Sprung and myself, I've been able to update the spreadsheet further; the blog post has also been updated correspondingly.

Last year, while Congressional Republicans were doing everything possible to officially repeal the Affordable Care Act via legislative means, Donald Trump spent months repeatedly threatening to cause the ACA individual market exchanges to either "explode" or "implode" (depending on the day) by, among other things, cutting off Cost Sharing Reduction reimbursement payments to insurance carriers.

For as much as I write about healthcare policy, I actually don't write about Medicare itself all that often...at least not Medicare as it's defined today.

CMS announces 2019 Medicare Parts A & B premiums and deductibles

Today, the Centers for Medicare & Medicaid Services (CMS) announced the 2019 premiums, deductibles, and coinsurance amounts for Medicare Parts A and B.

"Seriously, though, HHS should really start releasing the official (accurate) numbers of actual signups for all 50 states (or at the very least, the 36 states that they're responsible for) on a daily--or at least, weekly--basis. I don't care if it's a pitifully small number. 100,000? 10,000? 100? 10? Even if it's in single digits, release the damned numbers. Be upfront about it. Everyone knows by now how f***** up the website is, so be honest and just give out the accurate numbers as they come in."

Two days later, on October 13th, I registered "ObamacareSignups.net" (which soon changed to ACASignups.net, not because I had a problem with "Obamacare" but because it was easier to type) and posted an announcement over at dKos, asking for some crowdsourcing assistance.

Wisconsin has an interesting situation. On the one hand, the state has what should be a robust, highly-competitive individual insurance market,with over a dozen carriers offering policies throughout the state. Granted, some of them are likely limited to only a handful of counties, but in theory they should be doing pretty well compared to rural states like Oklahoma or Wyoming, which only have a single carrier on the exchange.

On the other hand, last year Wisconsin ahd among the highest average premium rate increases in the country. Rates were projected to increase by an already-awful 36%, but when the dust settled the average unsubsidized ACA enrollee in Wisconsin was paying a whopping 44% more than they did in 2017 (it was around 45.8% higher as of the end of Open Enrollment but later dropped a bit as the year has passed and net attrition has tweaked the enrollment base).

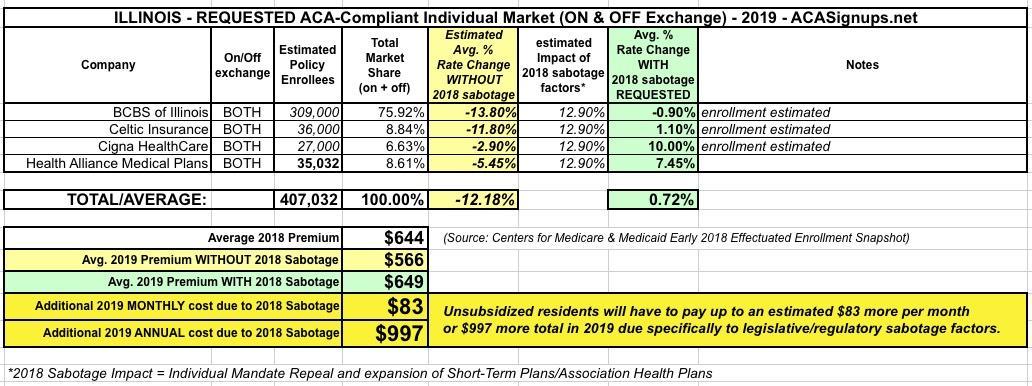

I ran the numbers for Illinois' requested 2019 ACA individual market rate changes back in August. At the time, the weighted year-over-year average was a mere 0.7% increase, with Cigna and Health Alliance's 10% and 7.5% being mostly cancelled out by Celtic's 1.1% and especially Blue Cross Blue Shield's slight drop of 0.9%. Since BCBSIL holds something like 3/4 of the state's individual market share, that alone mostly wiped out the other increases.

Unfortunately, I don't have access to the hard enrollment numbers, so this was a rough estimate based on 2017's breakout. Here's what it looked like at the time:

The final unsubsidized rates are down about one point more, down 6.3% from 2018 rates. However, as all three current carriers clearly noted in August, the repeal of the ACA's individual mandate and expansion of short-term and association health plans (aka #ShortAssPlans) still caused a significant premium increase, which means without those factors, 2019 rates would likely be down significantly more...likely nearly 20% instead of 6.3%:

With the 2019 Open Enrollment Period quickly approaching, I'm spending a lot of time swapping out the requested carrier rate changes from earlier this summer with the approved rate changes from state regulators.

Hawaii only has two carriers participating in the ACA-compliant individual market: HMSA and Kaiser, which requested rate increases of 2.72% and 28.6% respectively back in August. With a roughly 57/42 market share split, this resulted in a weighted average rate increase of 13.8%, which would likely have been closer to 3.8% if the ACA's individual mandate penalty hadn't been repealed.