We appreciate getting to meet with you and your team yesterday to update you on BlueCross’s position relative to the individual Marketplace for Tennessee as the first deadline for 2018 approaches.

As most people know by now (well, most people in Tennessee, anyway), Humana decided a full two months ago to bail on the entire individual market, across the board--every state, both on and off the exchange, the works. This stung in quite a few counties across 11 different states, but the one which everyone is freaking out about is Tennessee...because there are 16 counties where Humana was the only carrier participating on the ACA exchange. Here's the list of Tennessee counties Humana is available in this year; note that there's an additional 14 counties where there's one other carrier available at the moment.

As noted a few weeks ago, Humana has already decided that regardless of what actions Donald Trump, Tom Price or Congressional Republicans end up doing (or not doing), they expect the 2018 individual market to be a big mess they want no part of...either on or off the exchanges:

...based on its initial analysis of data associated with the company’s healthcare exchange membership following the 2017 open enrollment period, Humana is seeing further signs of an unbalanced risk pool. Therefore, the company has decided that it cannot continue to offer this coverage for 2018. Through the remainder of 2017, Humana remains committed to serving its current members across 11 states where it offers Individual Commercial products. And, as it has done in the past, Humana will work closely with its state partners as it navigates this process.

Again, it's important to stress that Humana isn't just bailing on exchange participation, but to the best of my knowledge, they're pulling up stakes off-excahnge as well.

Regarding the company’s individual commercial medical coverage (Individual Commercial), substantially all of which is offered on-exchange through the federal Marketplaces, Humana has worked over the past several years to address market and programmatic challenges in order to keep coverage options available wherever it could offer a viable product. This has included pursuing business changes, such as modifying networks, restructuring product offerings, reducing the company’s geographic footprint and increasing premiums.

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

Normally I post screenshots from the revised/updated SERFF filings and/or updates at RateReview.HealthCare.Gov, but it takes forever and I think I've more than established my credibility on this sort of thing, so forgive me for not doing so here. Besides, #OE4 is approaching so rapidly now that this entire project will become moot soon enough, as people start actually shopping around and finding out just what their premium changes will be for 2017.

The other reason I'm not too concerned about documenting the latest batch of updates/additional data is because in the end none of it is making much of a difference to the larger national average anyway; no matter how the individual carrier rates jump around in various states, the overall, national weighted average still seems to hover right around the 25% level.

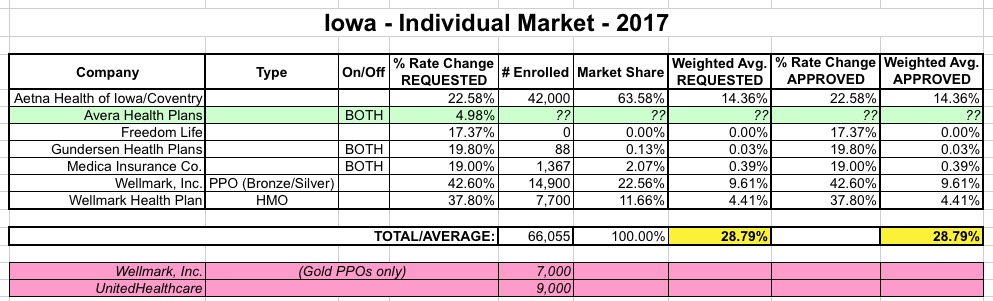

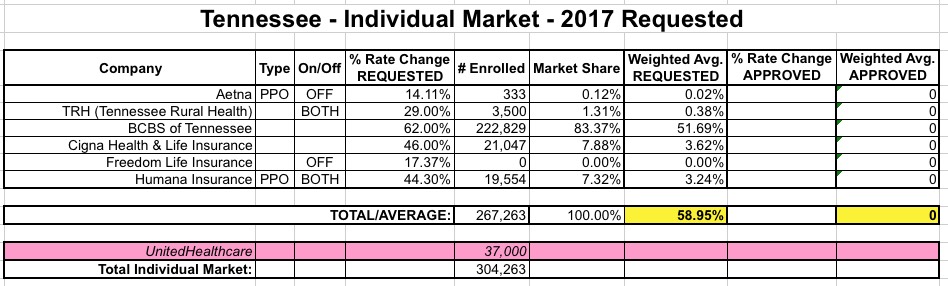

Still, for the record, here's the latest...in four states (Iowa, Indiana, Maine & Tennessee) I've just updated the requested and/or approved average increases. In the other four (Massachusetts, Montana, North & South Dakota) I've added the approved rate hikes as well.

Things are looking pretty good for the ACA exchanges in states like Rhode Island, North Dakota and Massachusetts, where they're looking at single-digit rate hikes next year. However, they're looking pretty dire in states like Arizona, Montana and Oklahoma, where the average hikes are likely to be around 50% or higher for many people.

As noted a couple of weeks ago, all three of the major insurance carriers participating in Tennessee's individual market ACA exchange asked for massive rate hikes this year, ranging from 44-62%. Blue Cross Blue Shield asked for 62% in the first place; Cigna and Humana resubmitted their original requests for higher ones.

Tennessee's insurance regulator approved hefty rate increases for the three carriers on the Obamacare exchange in an attempt to stabilize the already-limited number of insurers in the state.

...BlueCross BlueShield of Tennessee is the only insurer to sell statewide and there was the possibility that Cigna and Humana would reduce their footprints or leave the market altogether.

Cigna and Humana would have to revise their requests up to 50% apiece in order for the statewide average to end up hitting the 60% threshold, but that's not exactly a vote of confidence when it's already in the 56% range to begin with.

In its latest filing, Cigna is proposing an average 46 percent increase — double its first 23 percent increase request.

Humana, which requested a 29 percent average increase in June, is requesting an average 44.3 percent increase, according to a filing with the state regulators.

Here's what that looks like on the weighted average table:

In an effort to prevent more insurers from abandoning the Obamacare exchange in Tennessee, the state's insurance regulator is allowing health insurers refile 2017 rate requests by Aug. 12 after Cigna and Humana said their previously requested premium hikes were too low.