As I noted earlier today, there’s a gazillion ways the Trump Administration could sabotage (and in some cases, is already sabotaging) the 2018 Open Enrollment period this fall, doing everything in their power to dampen, obstruct and otherwise minimize the number of people who actually enroll in a healthcare policy via the federal ACA exchanges.

However, as I've noted before (and as the CBO confirmed last week), due to the confusing, inside out way in which the APTC and CSR subsidy formulas happen to work, there's also the potential for one of the most pressing sabotage schemes by Trump and the GOP to backfire completely, leading to the potential for a significant increase in ACA exchange enrollment.

I've noted before that even if the Trump Administration does ensure CSR reimbursement payments and does enforce the individual mandate in 2018, there are literally dozens of other ways that Trump and HHS Secretary Tom Price could sabotage the 2018 Open Enrollment Period. Here's just a few, several of which they've already been caught doing:

Minimal or non-existent advertising/outreach/promotional efforts

Understaffing of call centers/support staff, leading to absurdly long hold times

Deliberately underthrottled server bandwidth, slowing HC.gov down or even taking it offline, especially during peak hours

"Accidentally" misentered enrollment instructions or policy specifications

Confusing or missing confirmation/status notification messages either on the site, via email or both

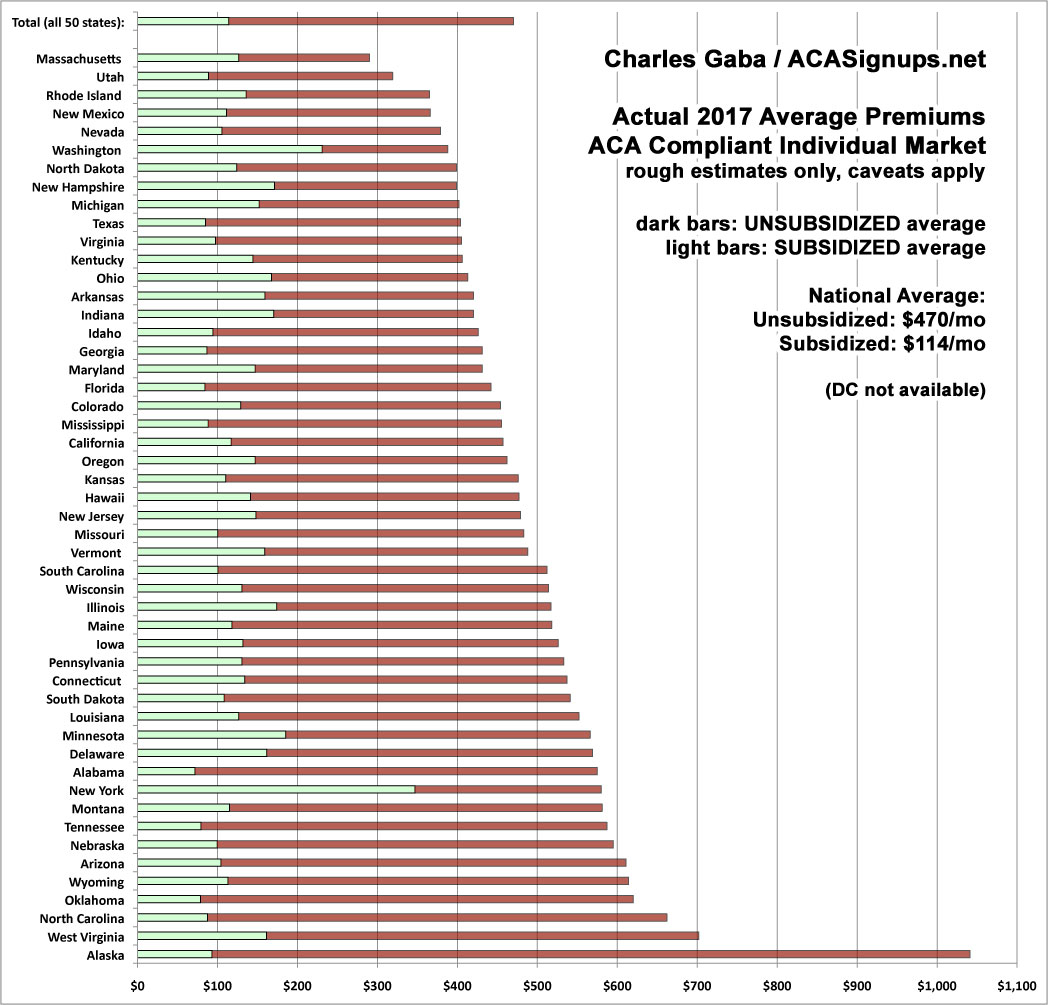

For all the fuss and bother about how much premiums are expected to go up on a percentage basis next year, using percentages can be misleading, since the lower the premium is to begin with, the more dramatic a percentage increase is going to seem relative to where it started.

With that in mind, I've decided to mush together two recent projects of mine: First, my debunking/correction of the May ASPE report which disingenuously claimed that individual market premiums had "increased by 105% since 2013 due to the ACA"; second, my 2018 Rate Hike Project.

As I noted when I debunked/corrected the ASPE report, not only did it turn out to be somewhat lower when all 50 states were included (84%, not 105%), but the ASPE report completely ignores both the financial assistance provided to roughly half the market and, just as importantly, blows off the apples to oranges mismatch between the numbers, because only a handful of states had guaranteed issue laws in 2013, and only one (NY) had a community rating law. Having said that, as long as you keep those caveats in mind, the (corrected) ASPE report does provide a good baseline for figuring out what the 2018 premiums are likely to be.

By merging the spreadsheets for these projects together, I've come up with a rough idea of what I expect to see in terms of unsubsidized, full-price premiums for individual ACA policies this November. I'm using a median instead of a weighted average this time around because I expect high variables in terms of the number of people who enroll in each state compared to 2017 (unfortunately, I still don't have 2018 data for several states, and I don't have the 2017 dollar average for DC to compare against).

I've ordered the states from lowest to highest based on the assumption that CSR reimbursements aren't made next year ("full sabotage effect"). The blue sections are my best estimates for each state assuming CSRs are paid; the yellow sections represent how much of the average premiums are due to "CSR padding" by the carriers.

As I explained a couple of weeks ago, even if CSR payments aren't made next year, there are five different paths a given insurance carrier can take for 2018:

1. Drop out of the on-exchange market so you're not at risk of having any CSR enrollees; stick around the off-exchange market.

2. Drop out of the entire individual market, both on and off exchange.

3. Preemptively cover your anticipated 2018 CSR losses by spreading them out across all plans on and off exchange.

4. Preemptively cover your anticipated 2018 CSR losses by loading them onto Silver plans only both on and off exchange.

5. Preemptively cover your anticipated 2018 CSR losses by loading them onto on-exchange Silver plans only.

Some carriers, tragically, have already thrown their hands up in the air and decided to wash their hands of the whole thing by choosing either #1 or 2 above. This includes Humana, Aetna, Wellmark and, most recently, Anthem, which is drastically scaling back their 2018 individual market participation levels.

County by County Analysis of Current Projected Insurer Participation in Health Insurance Exchanges

The Centers for Medicare & Medicaid Services (CMS) is releasing a county-level map of 2018 projected Health Insurance Exchanges participation based on the known issuer participation public announcements through June 9, 2017. This map shows that insurance options on the Exchanges continue to disappear. Plan options are down from last year and, in some areas, Americans will have no coverage options on the Exchanges, based on the current data.

House May Be Forced to Vote Again on GOP's Obamacare Repeal Bill

House Republicans barely managed to pass their Obamacare repeal bill earlier this month, and they now face the possibility of having to vote again on their controversial health measure.

A few days ago, CMS announced that they're retooling the ACA's SHOP program (at least on the federal exchange) so that instead of small businesses using HealthCare.Gov for eligibility verification, enrollment and payments, going forward it will only be used for verification, with the businesses then being kicked over to the actual insurance carrier website in order to actually enroll in the policies and make payments.

Although the Trump Administration and HHS Secretary Tom Price are hell bent on killing off the ACA altogether, this move didn't bother me for several reasons. For one thing, the SHOP program has always been kind of a dud anyway, with only around 230,000 people being enrolled in it nationally. For another, a business signing up their employees for coverage is a very different animal from an individual signing their family up for a policy. Finally, for several reasons, SHOP enrollment across the dozen or so state-based exchanges is actually higher than it is across the 3 dozen states covered by HC.gov, and the state-based exchanges aren't impacted by this policy anyway.

While poking around in the SERFF rate filing database for different states, I occasionally find filings which DON'T apply to ACA-compliant policies or enrollees but which are of interest to healthcare nerds such as myself. I've decided to bundle these into a single post as they pop up, so check this entry once in awhile.

IOWA: Big Kahuna carrier Wellmark submitted a filing for non-ACA compliant small group policies (either grandfathered or transitional) which have effective/renewal dates of July, August or September 2017. The requested rate increase is 7.0% on average, which is pretty typical for small group plans, and it appears that Wellmark had 51,003 people enrolled in such policies as of 12/31/16. Nothing odd there.

I'm not sure what the original source for this is, but the following initial filing deadlines were provided by Stephen Holland via Twitter. I've already posted analyses of the Virginia, Maryland and Connecticut filings. The California and Oregon filings are supposed to have been submitted already but don't appear to be publicly available yet. In addition, it's my understanding that in many states the rates can still be adjusted/resubmitted until as late as August 16th, so I'm not really sure how useful these dates are anyway, but it's at least a guideline.

12. LEGALLY TIE MEDICARE ADVANTAGE/MANAGED MEDICAID CONTRACTS TO EXCHANGE PARTICIPATION.

Andrew Sprung, Michael Hiltzik and I have all written about this before. I have no idea whether it's even legally feasible/practical or not, but if so, it makes a lot of sense to me: Remember, many of the same carriers whning about losing hundreds of millions of dollars on the individual market are simultaneously making billions of dollars in profit off of their other divisions...which include fat federal and state contracts to manage Medicare and/or Medicaid plans. If they want to play in the managed care sandbox, make exchange participation a requirement as well. I'm not saying they should have to treat it as a loss leader--they'd still be able to raise their premiums at an actuarially responsible rate as appropriate--but they should have to at least participate.

{kind=link}