*(technically Vermont was the third to do so, but theirs doesn't kick into effect until 2020, and they haven't even crystalized exactly what form it would take anyway.)

**(yeah, I know very well that DC isn't actually a state, but it's pretty awkward to put "state and/or territory" in the headline.)

I realize that 110% of the news/media/political attention is on the bombshell announcement that Supreme Court Justice Anthony Kennedy is retiring at the end of July, but there are other things going on as well, so I'll do my best to soldier on...

More big health care action at the state level: yesterday the DC Council passed what would be the nation's third state-level individual mandate, after Mass. and NJ.https://t.co/BmtnDAQvVp

AHIP Issues Statement Regarding TX v. United States of America

WASHINGTON, D.C. – America’s Health Insurance Plans (AHIP) issued the following statement regarding the latest developments in TX v. United States of America:

“Millions of Americans rely on the individual market for their coverage and care, and they deserve affordable choices that deliver the value they expect. Initial filings for 2019 plans have shown that, while rates are higher due to the zeroing out of the individual mandate penalty, the market is more steady for most consumers than in previous years, with insurance providers stepping in to serve more consumers in more states.

Last night I made a big fuss about New Jersey Governor Phil Murphy signing a restoration of the ACA's individual mandate penalty into law.

It turns out that the Governor of Vermont also signed the ACA mandate restoration bill I wrote about back in March into law a few days ago as well...but it's not as noteworthy, for several reasons. As Louise Norris reports over at healthinsurance.org:

Vermont governor signs legislation to implement an individual mandate starting in 2020; working group will sort out enforcement details

Establish a robust reinsurance program to significantly lower insurance premiums for individual market enrollees,

Protect people from out-of-network "balance billing", and

Cancel out Trump's expansion of "Association Health Plans"

In addition, New Jersey already outlawed "Short-Term Plans" (and "Surprise Billing") before the ACA was passed anyway.

Well, until today, there was some lingering doubt about the first two bills (which are connected...the reinsurance program would be partly funded by the revenue from the state-level mandate penalty), as Gov. Murphy was reportedly kind of iffy about signing them. As I understand it, he's been supportive of both ideas but is concerned about the potential budget hit in case the mandate penalty revenue doesn't raise enough to cover its share of the reinsurance program.

For a couple of months now, I've been attempting to track a slew of state-based "ACA 2.0" bills slowly winding their way through various state legislatures. However, this is really a bit of a misnomer, since some of these bills aren't so much about expanding the ACA as they are about protecting it from various types of undermining or sabotage from the Trump Administration and Congressional Republicans.

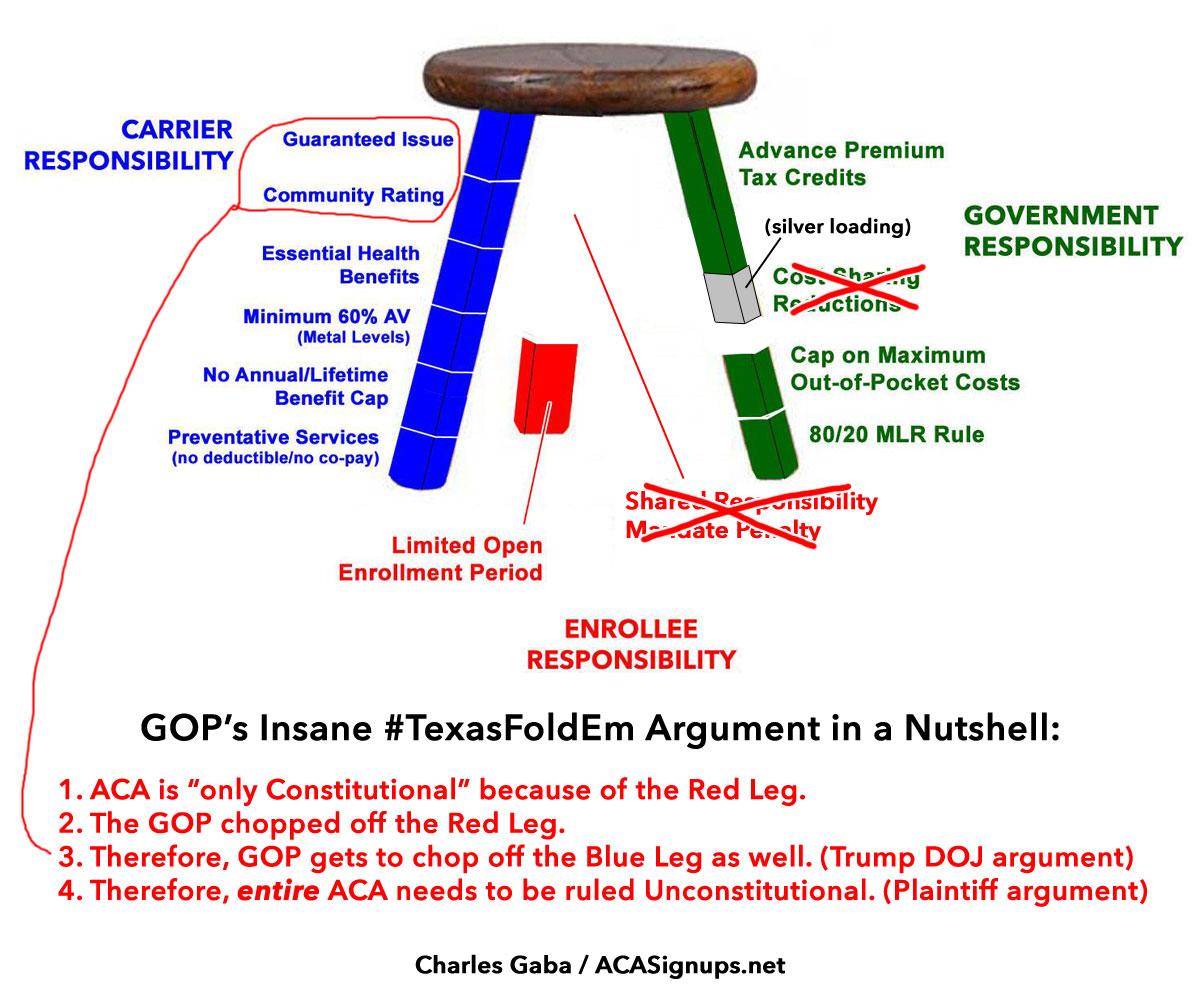

Once again: The "Blue Leg" of the Stool covers everything which ACA-compliant individual health insurance carriers are required to include: Guaranteed Issue, Community Rating, 10 Essential Health Benefits, a Minimum 60% Actuarial Value rating, no Annual or Lifetime Caps on coverage, and a long list of mandatory Preventative Services at no out-of-pocket cost when done in-network.

Price says that he's not a big fan of the GOP tax bill's 2019 individual mandate repeal-- says it will harm the pool in the exchange markets & drive up costs

Making my eyeballs roll even further back in my head, here's what Price said just nine months ago (shortly before he was given the boot from the HHS Dept.):

I've noted before that now that the Republicans in Congress have repealed the ACA's much-hated (but vitally necessary) individual mandate penalty (effective 2019), the odds of it being reinstated at the federal level are virtually zilch. Even if there's a massive blue wave in November and the Democrats are able to retake both the House and Senate, they're extremely unlikely to be willing to face the same type of firestorm/backlash that they did back in 2009-2010 over it.

SACRAMENTO, Calif. — Covered California Executive Director Peter V. Lee issued the following statement in connection with the Harvard Medical School Study, “Eliminating the Individual Mandate Penalty in California: Harmful but Non-Fatal Changes in Enrollment and Premiums,”published in Health Affairs. The Harvard study, conducted by a team lead by Dr. John Hsu, is the first national effort to measure the potential impacts of removing the individual mandate penalty based on surveying actual California consumers about their likely actions in the face of there being no penalty.

Last year, in my "If I Ran the Zoo" piece, I stuck my neck out and noted that the single biggest problem with the Individual Mandate isn't that it exists, but that it's not strong enough (conservative healthcare writer Michael Bertaut, who I disagree with on most issues but respect on this topic, also argues that the mandate has never been enforced strongly enough either). Here's what I said at the time:

The reality is that as much as everyone complains about the $695 or 2.5% income individual mandate penalty for NOT having qualifying healthcare coverage, the penalty should really be increased. There, I said it. The problem is that if the penalty is significantly less than the amount that the premiums would be, some people will still decide to eat the tax instead of signing up.