OK, strictly speaking this isn't directly ACA-related, but come on...

Shumlin: "The time is not right"

Vermont has long had a two-pronged approach to building a single-payer health care system. First, they would figure out what they would want the system to look like. Then, they would figure out how to pay for it.

The state passed legislation outlining how the single-payer system would work in 2011. And ever since, the state has been trying to figure out how to pay for a system that covers everybody. Most estimates suggest that the single payer system would cost $2 billion each year. For a state that only collects $2.7 billion in revenue, that is a large sum of money.

What Shumlin appears to be saying today is that the "time is not right" to move forward on the financing of the single-payer system. And that means putting the whole effort aside, with no clear moment when the debate would be reopened.

Ouch.

Thanks to Morgan True for the link to this PowerPoint report which explains why VT is pulling the plug on their ambitious Single Payer attempt:

As of Thursday the 12th, MNsure had enrolled about 14.4K people for private 2015 policies. Thanks to the December Surge Weekend, this has jumped up by more than 9,300 more:

Latest Enrollment Numbers

December 17, 2014

Health Coverage Type Cumulative Enrollments

Medical Assistance 17,888

MinnesotaCare 7,681 Qualified Health Plan (QHP) 23,797

TOTAL 49,366

Hmmm...MNsure is currently enrolling people at 3x the rate they did all of last year. Assuming that this doesn't include automatic renewals, that's pretty good. They bumped their enrollment deadline for January coverage out until Friday afternoon (4:30pm, for some reason), which is even better.

UPDATE: According to this Modern Healthcare article, only about 42% of MN's enrollments to date are renewals. In one sense, this is good since it suggests that they still have a good 31K potential renewals to work with.

No formal press release yet, but CT is the 2nd state (after Kentucky) to announce how many 2014 enrollees were automatically renewed (as opposed to manually renewing):

66,000 of our customers were auto enrolled in our system and continue to have health coverage for 2015. #OEUpdate

The most recent update I have from Connecticut was 13,000 new enrollees, but that was only through last Friday, before the big weekend push. That means they added another 7K over the weekend; not bad!

As CoveredCA has noted before, they have no plans on posting renewed policy enrollments until January, but this at least gives data on the new additions:

COVERED CALIFORNIA AND DEPARTMENT OF HEALTH CARE SERVICES RELEASE EARLY RESULTS FOR FIRST MONTH OF OPEN ENROLLMENT THROUGH HEALTH INSURANCE EXCHANGE

Demand for Coverage Continues to Be Strong, with Applications Submitted for More Than 592,000 People Through Dec. 15

SACRAMENTO, Calif. — More than 592,000 people sought coverage and were determined eligible for private health insurance and eligible or likely eligible for Medi-Cal in the first month of open enrollment, Covered California and the California Department of Health Care Services announced Wednesday.

The consumers, who applied for coverage through Covered California since open enrollment began on Nov. 15, include 157,361 eligibility determinations and an additional 144,178 plan selections for private coverage, as well as 216,423 enrollments into Medi-Cal coverage and 74,965 who are likely eligible for Medi-Cal. So far in 2014, Medi-Cal has enrolled more than 2.2 million consumers.

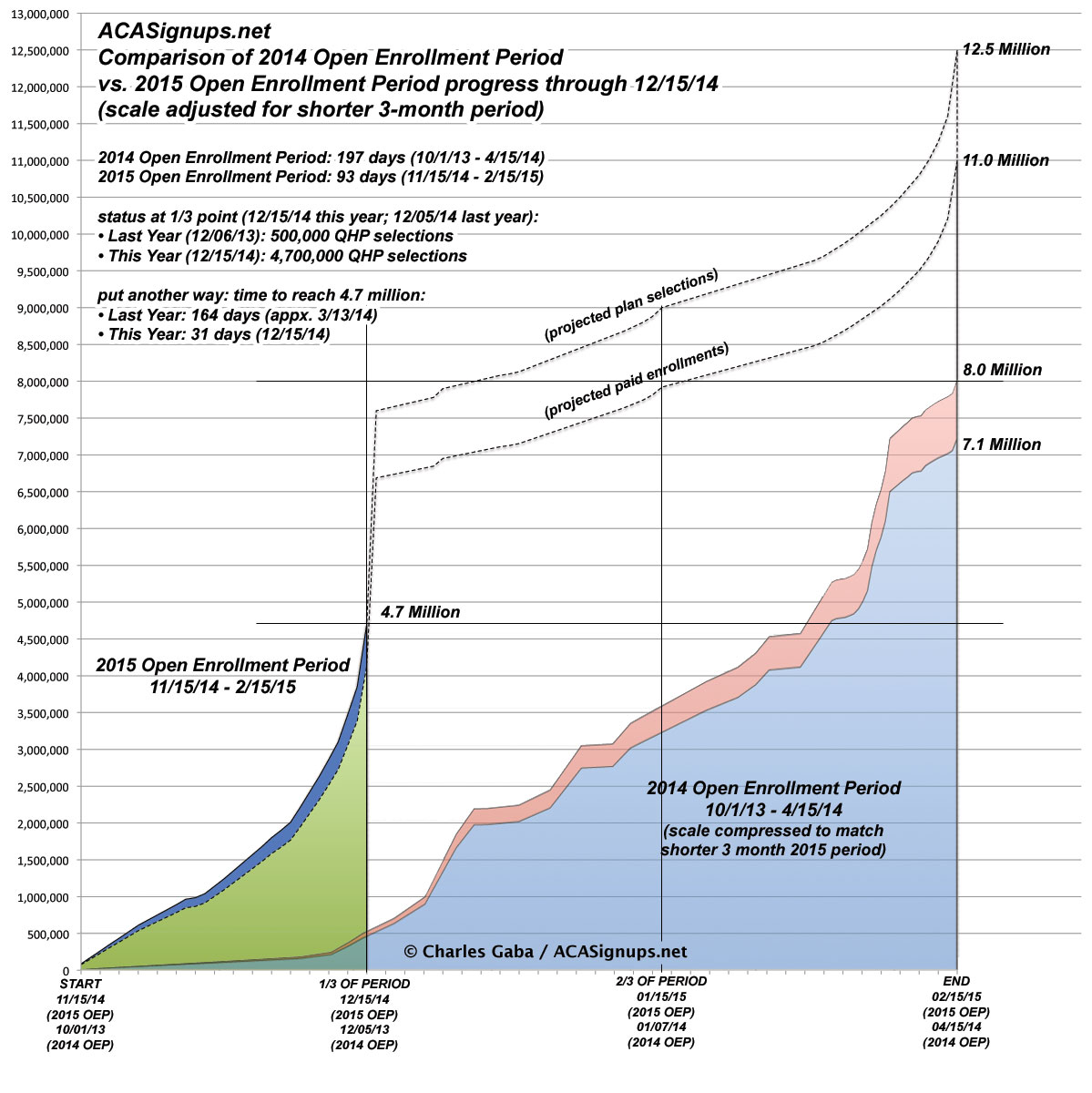

After all the craziness of the past day or two, I figured this would be a good time for a reality check. I've taken the 2014 Open Enrollment Period Graph, compressed it so that the time period and scale match the 2015 Period (ie, 3 months instead of 6.5) and have overlaid it on top of the 2015 Graph to see how they compare. The comparison is pretty striking.

(NOTE: I've modified this version to make the adjusted timeframes less confusing, and clicking below will now load the full-size version in a new window):

Wow! This was unexpected; while several other states have provided enrollment updates today, and some have broken out (or at least included) both new enrollments as well as manual renewals/re-enrollments, Kentucky is the first one to include automatic renewals as well!

Webb is one of 101,114 Kentuckians who have newly enrolled or re-enrolled in Obamacare health plans during the first 30 days of open enrollment through the state's health insurance exchange, kynect. State numbers released late Tuesday afternoon show that 16,139 residents met eligibility requirements for Medicaid, 9,215 newly enrolled in qualified health plans and 75,760 auto-renewed last year's private kynect health plans since re-enrollment began Nov. 15.

This is important for a couple of reasons: First, it's the first enrollment update of any sort we've heard from Idaho (which was, until tonight, the only exchange I didn't have any info on). Secondly, it's important because Idaho is the only state which moved off of Healthcare.Gov onto their own exchange. Finally, the number is absolutely fantastic, especially considering that it doesn't include Monday:

BOISE, Idaho – During the first month of open enrollment, Your Health Idaho processed 74,689 enrollments, which includes new applicants and those renewing coverage for 2015. The numbers released by Your Health Idaho at its Tuesday board meeting include enrollments processed from November 15 through December 14.

For comparison, last year Idaho enrolled 76,000 people for the entire enrollment period.

That's right: They managed to essentially equal 6 1/2 months worth of private policy enrollments in just 1 month...and that doesn't include the surge from yesterday (or for the following 5 days, since ID's deadline isn't until the 20th).

On the one hand, I'm a bit pouty today because I was off by about 6% on my HC.gov estimate through the 4th week. On the other hand, this is good news because it means that the actual enrollment total is 126K higher than I thought...and that's just via Healthcare.Gov! Of course, it's possible that the state exchanges will be a bit lower than I thought which might cancel this out, but assuming the 75/25 ratio is accurate, it should mean that instead of the 3.1 million national total I had estimated for 12/12, it should be closer to 3.3 million!

Anyway, here's the hard numbers from HC.gov through December 12th:

The CMS Dept. is holding a conference call with reporters right now. I'll be liveblogging the call and posting updates as quickly as I can for any useful info. It should focus much on the enrollment numbers, of course, but also how well the HC.gov servers held up under yesterday's strain, and I'd expect a lot of discussion of the "autorenewal" issue--how many, how it'll be handled and so forth.

Participants: Lori Lodes, Kevin Counihan & Andy Slavitt

3:04pm: Call hasn't started yet, but HHS just releaced their 4th week enrollment data for HC.gov (thru 12/12)...and it's actually 5.4% higher than I thought! (thanks to Bob Herman for the tip!)

My estimate: 2.32 million

Actual: 2,446,562

still 52% renewals / 48% new

Call starting:

first 8 hours: 20K applications

last 3 days: more than 3 million unique site visitors