HEALTHSOURCE RI RELEASES ENROLLMENT, DEMOGRAPHIC AND VOLUME DATA THROUGH FEBRUARY 7, 2015

Posted on February 11, 2015 | By HealthSource RI

PROVIDENCE – HealthSource RI (HSRI) has released enrollment data, certain demographic data and certain volume metrics through Saturday, February 7, 2015, for Open Enrollment.

RENEWAL UPDATE

As of February 7, 2015, 79% of Year One customers have renewed (selected a plan) for 2015

(77% of renewing customers paid the first month’s premium).

Total New Customers: 8,547 (7,372 paid)

Total Renewed Customers: 20,240 (19,617 paid) Total HealthSource RI enrollments for 2015 coverage: 28,787 (26,989 paid)

*Note: Individuals who have selected a plan but not paid by their selected coverage effective date become cancelled; reported enrollment values (plan selections, paid and unpaid) will fluctuate with potential net decrease due to plan selection cancellation, as of the passage of the January coverage payment deadline.

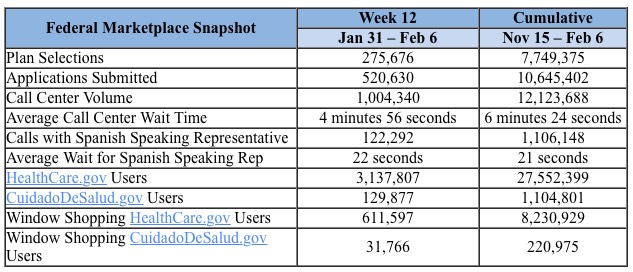

On Wednesday the 11th, HHS should issue a report including all HC.gov QHP selections as of Friday the 6th. I'm expecting the total to be roughly 7.75 million, or about 276K for the week.

This is possibly the dumbest story to make Major Headlines this week, but apparently GOP Speaker of the House John Boehner uttered the word "ass" in public.

Considering that VP Biden was caught on tape referring to the signing of the Affordable Care Act as a "Big F*cking Deal", I'm not quite sure I understand why Boehner saying "ass" is newsworthy, but what the hell: Here's my own connection to that "story": About 1:20 into this Al Jazeera America segment from March 26th, Boehner says "What the hell is this, a joke??" referring to the 2-week "extension period" tacked onto the end of last spring's Open Enrollment Period.

Oh, yeah...immediately after he rhetorically asks, "What the hell is this, a joke??", the segment turns to...me! (This has been, to date, my only televised appearance):

As of last Thursday, total QHP selections on the Massachusetts exchange were up to just shy of 119K. Between the weekend and the massive snowstorm that MA is digging out of, they went 5 days without a dashboard report, until today:

As always, I only have the QHP determinations to go by between their weekly reports. As of yesterday, those stood at 221,877, Subtract the 214,027 as of 2/05 and that's another 7,850 QHP determinations. Assuming 50% of those followed through with selecting a plan (a reasonable assumption at this point) and that's another 3,900 QHPs, or at least 122,600 QHPs to date.

Of course, that means that there's also another 99,000 people who started the process and have been approved for a private policy, but who may--or may not--have actually completed the process. Heading into the final 5 days, I presume that more and more of this enrollee pool will be scratched off the list; if, say, 80% of these folks follow through, Massachusetts would hit at least 200,000 QHPs by Sunday night.

Last year, I started out tracking just 2 numbers: Exchange-based QHPs and Medicaid via official ACA expansion provisions. As time went on, I gradually added other types of Obamacare-specific healthcare policy enrollments:

Off-exchange policies which were compliant with the new law;

People who were already eligible for traditional Medicaid prior to expansion (and in non-expansion states) but who were only "drawn out of the woodwork" to sign up thanks to outreach efforts, educational programs and streamlining of the enrollment process in many states

People who were transferred over from other existing low-income state-run healthcare programs (often with shaky funding) into Medicaid proper;

Enrollees in small business policies via the ACA's SHOP program (granted, this never ended up being more than a rounding error...less than 80K total)

Young adults aged 19 - 25 who were allowed to stay on their parent's plan thanks specifically to the ACA

As noted earlier, there's a lag between the exchange-based QHP data from HC.gov vs. the Oregon Insurance Division, so you can ignore that number. However, the off-exchange number should be accurate (and this is the official source for it anyway):

Members enrolled,

Nov. 15-Feb. 1

On Healthcare.gov 86,606 Outside of Healthcare.gov 95,859

Total 182,465

Last week the off-exchange total was 92,872, so that's about a 3,000 enrollee increase, for whatever that's worth.

According to the HC.gov weekly snapshot report, as of 2 days earlier (1/30), Oregon's exchange-based total was 94,126...slightly less than the off-exchange number. It'll be interesting to see if that ratio holds steady next week after the final deadline surge goes through.

Remember "Florida Health Choices", the brainchild of Republican Senator Marco Rubio which was supposed to be the Florida GOP's response to the Affordable Care Act health insurance exchanges?

The Florida Republican Party flushed $900,000 in startup funds into a website/"exchange" which signed up a whopping 30 paying customers in 6 months, at a cost of $30,000 apiece...or between 46x - 81x as much per enrollee as the "wasteful" HealthCare.Gov.

Beneficiaries with Healthy Michigan Plan Coverage: 546,807

(Includes beneficiaries enrolled in health plans and beneficiaries not required to enroll in a health plan.)

*Statistics as of February 9, 2015

*Updated every Monday at 3 p.m.

Connecticut's official 2015 QHP target is an even 100K. They were 99% of the way there as of last night, with no technical problems to speak of gumming up the works:

As of Jan. 30, 95,700 people had signed up for private insurance through Access Health, including about 66,700 repeat customers from 2014. (On Monday, officials said more than 99,000 people had signed up for private insurance plans through the exchange.) By comparison, last year, slightly more than 80,000 people bought insurance through the exchange (though a few thousand dropped out as the year went on).

My own target for CT is 114K. To reach that, they'll have to enroll just 2,100/day for the final week, or less than twice the rate they've averaged so far. This shouldn't be a problem; nationally, I'm expecting QHP enrollments to average around 286K/day all this week, which is around 2.33x more than the average to date, and Connecticut has one of the most solid operations of any state.