There's a lot of great lines in the 1988 semi-autobiographical movie/play "Biloxi Blues" by Neil Simon. Most are funny, some are poignant. To me, one of the most powerful scenes is when Jerome/Simon's (played by Matthew Broderick) diary is found and read by his boot camp bunkmates. Among the private thoughts he has about them being revealed, one of his friends, Arnold Epstein, discovers that Jerome thinks that he (Epstein) is gay. Since the story is set in the World War II-era U.S. Army, this obviously has much bigger implications than it would today.

After the scene plays out, Jerome/Simon/Broderick's voiceover notes that:

"Something magical happens when people read something on paper...they have a tendency to believe it. They figure no one would have bothered to write it down if it wasn't true." (that's a paraphrase...I can't find the video clip or transcript for Biloxi Blues online).

Jerome concludes by noting that this incident taught him to be more careful about what he writes.

OK, kind of a stupid title, I know, but it's been a really long day...spent 3 hours clearing our driveway/porch/roof/etc. after a snowstorm (and my kid had a snow day as well, of course, making it difficult to get any work done even after I was done shoveling...)

Anyway, there were four ACA-related stories today which are all worthy of a full entry, but I'm too exhausted to do a full writeup on any of them:

How is Obamacare ruining your life today? Fox News host Tucker Carlson thinks that he knows how Obamacare is ruining your life if you live in Colorado, let’s see if he is correct! Colorado’s health care exchange, Connect for Health Colorado, glitched out last week and cancelled the health insurance of 3,600 Coloradans who went on the state’s exchange to shop for another plan. Tucker Carlson invited perfect Fox News victim Steven Roussel, an articulate white guy, to describe the absolute horror of this bureaucratic glitch, or, as Tucker Carlson put it, “Kafka comes to Colorado!” Indeed!

Two days ago, after seeing that the White House (and President Obama specifically) had come out with an official (if utterly obvious) statement stating that vaccinating children is absolutely recommended in response to the insanity of the past few years, I snarkily tweeted the following:

In response to this post on both Twitter and Facebook, 3 friends of mine (one a Republican, one an otherwise sensible Democrat and one with whom I've never discussed politics one way or the other) posted the following comments:

As I noted a week or so ago, there's a slight discrepancy between Healthcare.Gov's ON-exchange QHP tally for Oregon (currently 92,059 as of 1/23) and the state insurance division's record (85,912 through 1/25). This turns out to be due to a combination of lag time between HC.gov recording new enrollments & the state insurance dept. receiving them, plus the fact that one of the companies is only reporting paid enrollees, not total, which skews the numbers. As such, I'm using HC.gov's data for the on-exchange QHPs.

However, for off-exchange QHPs, the only source is the Oregon Dept. of Insurance, and this has gone up a couple thousand people over the past week or so:

The Insurance Division will collect enrollment information from carriers each week throughout 2015 open enrollment. Updated numbers will be posted each week on this web page.

Members enrolled,

Nov. 15-Jan. 25

On Healthcare.gov 85,912 Outside of Healthcare.gov 92,872

Total 178,784

Connect for Health Colorado has released their end-of-month enrollment update. Since the 1/15 deadline for February coverage, they've added another 3,728 QHP enrollees, or 233/day. At that rate they'd only add another 3,500 by 2/15, or less than 130K total (vs. their target of 194K or mine of 208K). Of course, that's an extremely unfair comparison, as 1/16 - 1/31 covers the slowest portion of the open enrollment period (immediately after a monthly deadline).

Even so, there's no realistic way that CO can hit their target at this point--they'd have to average 4,600/day just to hit theirs (and over 5,500 to hit mine). For comparison, last year Colorado averaged 627 enrollees per day throughout the entire open enrollment period (and that included the huge surges in December and March). This year they've averaged 1,607/day, and that includes all of the renewals from 2014. Even with a massive final surge, I just don't see any way of CO hitting more than 160,000 QHPs at this point, although I'll obviously be happy to be proven wrong.

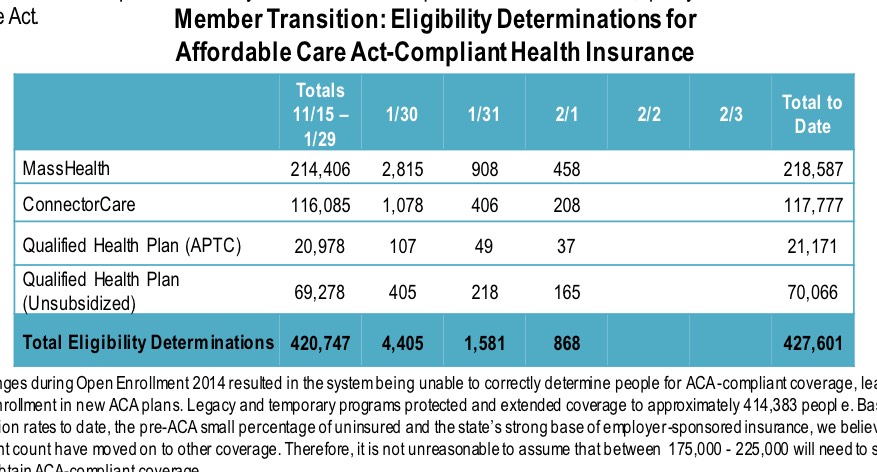

The "quiet period" continues this week, with just 2,673 QHP determinations over the past 3 days. Assuming 45% followed through and selected a plan, that means roughly 115,100 QHPs to date. Meanwhile, Medicaid enrollments have reached 218,587.

The 51 states (including the District of Columbia) that provided enrollment data for November 2014 reported nearly 69 million individuals were enrolled in Medicaid and CHIP. This enrollment count is point-in-time (on the last day of the month) and includes all enrollees in the Medicaid and CHIP programs who are receiving a comprehensive benefit package.

444,324 additional people were enrolled in November 2014 as compared to October 2014 in the 51 states that reported comparable October and September data.

(And yes, the "51 states" wording is CMS's, not mine)

I woke up this morning to learn that Paul Krugman has given me another shout-out this A.M. This is about the 8th or 9th time he's linked to me, but only the 2nd time that he's mentioned me by name (usually it's just a text link to the relevant entry). The first time was last March, when he compared me favorably to the Lord of the Data Nerds, Nate Silver; this time my name is mentioned in the same paragraphs as Ezra Klein and Andrew Sullivan. Needless to say, I'm flattered and honored beyond measure.

A decision made more than three years ago by a committee that no longer exists might deal a major blow to Obamacare in South Carolina this summer.

...Former members of the S.C. Health Exchange Planning Committee say they weren’t aware in 2011 that their opposition to a state-based insurance marketplace might jeopardize so many people’s ability to pay for coverage.

“At no point in the committee’s discussion was there ever raised a concern that by opting into the federal exchange we were losing anything — especially subsidies,” said Tim Ervolina, president of the United Way Foundation of South Carolina and a former planning committee member. “I recall a very intense discussion with (former) Sen. (Mike) Rose, who stated that, after reviewing the law, he felt confident that we had nothing to lose and everything to gain by opting into the federal exchange.”

The percentage of Vermonters without health insurance has dropped to 3.7 percent, second lowest in the nation, according to new data from a survey of 4,000 households. Massachusetts, which mandates health insurance coverage, has the lowest percentage of uninsured.

Since the last state-sponsored survey, in 2012, the number of uninsured Vermonters declined from 42,760 to 23,231, according to weighted results.

According to the Kaiser Family Foundation, Vermont's pool of potential private ACA exchange enrollees was around 44,000 people as of last April (ie, right after the 2014 enrollment period ended).