Rate filings were due in New Mexico by June 10, 2018, for insurers that wish to offer individual market plans in 2019. Insurers that offer on-exchange coverage have been instructed by the New Mexico Office of the Superintendent of Insurance (NMOSI) to add the cost of cost-sharing reductions (CSR) only to on-exchange silver plans and the identical versions of those plans offered off-exchange (different silver plans offered only off-exchange will not have the cost of CSR added to their premiums).

AHIP Issues Statement Regarding TX v. United States of America

WASHINGTON, D.C. – America’s Health Insurance Plans (AHIP) issued the following statement regarding the latest developments in TX v. United States of America:

“Millions of Americans rely on the individual market for their coverage and care, and they deserve affordable choices that deliver the value they expect. Initial filings for 2019 plans have shown that, while rates are higher due to the zeroing out of the individual mandate penalty, the market is more steady for most consumers than in previous years, with insurance providers stepping in to serve more consumers in more states.

For those of you just coming to the case, this is from my earlier recap:

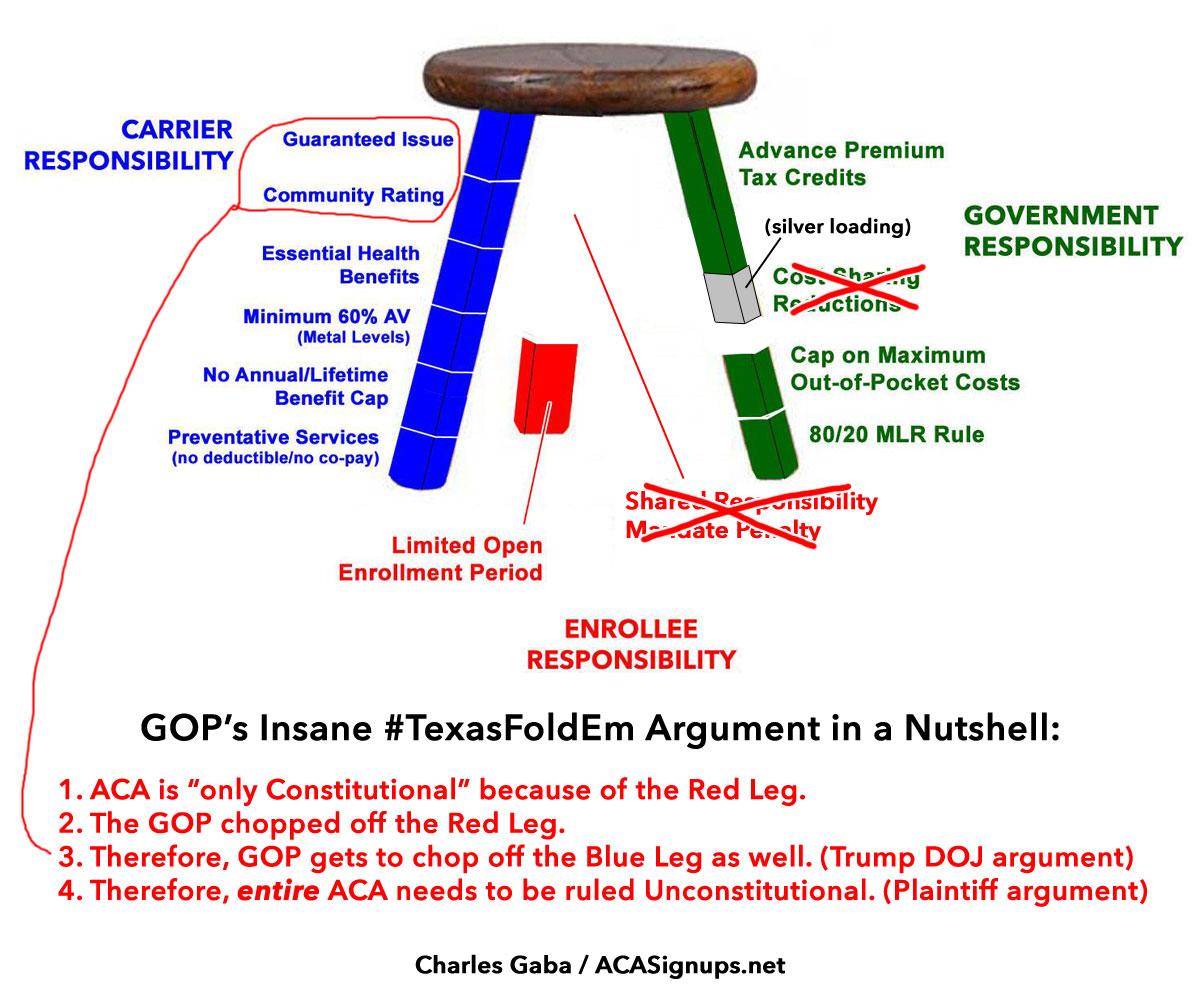

In their complaint, the states [including Texas and other red states] point out (rightly) that the Supreme Court upheld the ACA in NFIB v. Sebelius only because the individual mandate was a tax and (rightly) that Congress has now repealed the penalty for going without insurance. As the states see it, the freestanding requirement to get insurance, which is still on the books, is therefore unconstitutional. Because it’s unconstitutional, the courts must invalidate the entire ACA—lock, stock, and barrel.

Welp. The idiotic #TexasFoldEm lawsuit against the ACA...or more specifically, the Trump Administration's decision to lay down and even join the lawsuit against it--appears to be doing even more damage to the U.S. Justice Department than I had thought:

A highly respected career lawyer at the Justice Department has decided to resign just days after the Trump administration backed a controversial lawsuit that would wreck part of the Affordable Care Act.

About 90% of my focus here at ACASignups.net is on the two biggest sections of the ACA: The Individual Market (3-legged stool, exchanges, subsidies, etc.) and Medicaid expansion. I tend not to write much about Medicare, "traditional" Medicaid or the Employer-Sponsored Insurance (ESI) market, which mainly consists of the Large Group Market (companies with 50 employees or more) and the Small Group Market (companies with fewer than 50 employees). As it happens, the ESI market covers nearly half the U.S. population (roughly 155 million Americans, give or take).

Under the ACA, individual market policies have to include the following "Blue Leg" provisions to be considered ACA-compliant:

McConnell on Trump’s decision to support the Texas lawsuit that would invalidate Obamacare:

"Everybody I know in the Senate, everybody, is in favor of maintaining coverage for preexisting conditions. There's no difference in opinion about that whatsoever."

Even if you ignore the multiple times over the years that he's promised (and voted) to "defund Obamacare" and "repeal it out root & branch"...

...there's still the matter of last year, when Senate Republicans introduced the "Better Care Reconciliation Act plan" (BCRAp), which looked something like this:

By far, the most popular provisions of the Affordable Care Act is that it mandates Guaranteed Issue (GI) and Community Rating (CR) rules to all major medical healthcare insurance policies in most of the United States (all 50 states, plus DC...most ACA provisions don't apply in Puerto Rico, Guam and other U.S. Territories). These provisions state, quite simply, that insurance carriers can no longer discriminate against enrollees based on their physical or mental health status or history, their gender and so on, and can therefore no longer use medical underwriting to either cherry-pick who their enrollees are or how much they're charged in premiums for a given policy.

It's time once again to talk about stools. Not step stools, but the Three-Legged Stool.

I posted this video explainer about the Affordable Care Act's "Three-Legged Stool" works last winter. The first 9 minutes or so covers why it exists, how it's supposed to work, how well it's actually working, the most obvious problems with it and the basics of how to fix them. The second half goes into the details of the half-dozen different awful repeal/replace bills that Congressional Republicans tried to push through throughout 2017.

Below is a condensed transcript version of the first half of the slideshow.

First of all, who is in the Individual Market? Well, what you're looking at right now is something a friend of mine dubbed The Psychedelic Donut. It's actually a depiction of the healthcare coverage, by type, of the entire U.S. Population...all 320 million or so of us.

One of the big stories over the past few months has been the Trump Administration's attempts to strip away regulations on non-ACA compliant "Short-Term, Limited Duration" plans (by making them neither short-term nor of limited duration) and "Association Health Plans" (by recategorizing them from state-regulated, Small Group plans to mostly unregulated Large Group plans).

The Iowa Senate voted Wednesday to let the Iowa Farm Bureau Federation and Wellmark Blue Cross & Blue Shield sell health insurance plans that don't comply with the federal Affordable Care Act.

The new coverage could offer relatively low premiums for young and healthy consumers, but people with pre-existing health problems could once again be charged more or denied coverage.