About 800,000 people nationally lost their insurance coverage, on very short notice, and were forced to scramble to find alternate coverage

The new coverage they ended up with was generally more expensive, and in many cases has worse networks

The federal government has to pay out more in premium subsidies to cover the increased costs as benchmark plans were increased

Over a dozen insurance carriers went out of business, meaning hundreds of people lost their jobs

Less competition in those markets, therefore higher premiums, therefore even more cost to the federal government in subsidies to make up the difference

Since all of the carriers which went out of business were little guys, this also means the big kahunas suck up even more market share

The original $2.5 billion which Rubio was supposedly trying to "save" taxpayers ends up being paid out anyway; and

Assuming the government decides to just concede the point (which, by all rights, they should), it's conceivable that Marco Rubio's "genius" stunt from December 2014could also very well end up costing taxpayers $2.5 billion MORE than it would have to just let the government make the payments they were supposed to in the first place.

...all of this just so that Marco Rubio could earn a couple of political brownie points to help him win the GOP nomination for President...which he ended up failing at miserably.

Throughout the summers of 2015 and 2016, the news media was chock-full of apocalyptic headlines screaming about MASSIVE DOUBLE DIGIT OBAMACARE RATE HIKES!!!, suggesting that rate hikes of 20%, 30% even 50% would be not just widespread but the norm nationally.

The reality, as I repeatedly tried to get through people's heads, is that while some carriers in some states were trying to push through massive hikes on some plans, the overall picture was far less dramatic. Many were seeking increases of under 10%, while some (not many, I admit) were even reducing rates. When you averaged out the rate changes by state and then weighted them by the number of people actually enrolled in those policies, it came in at around 7-8% in 2015 and around 12-13% in 2016.

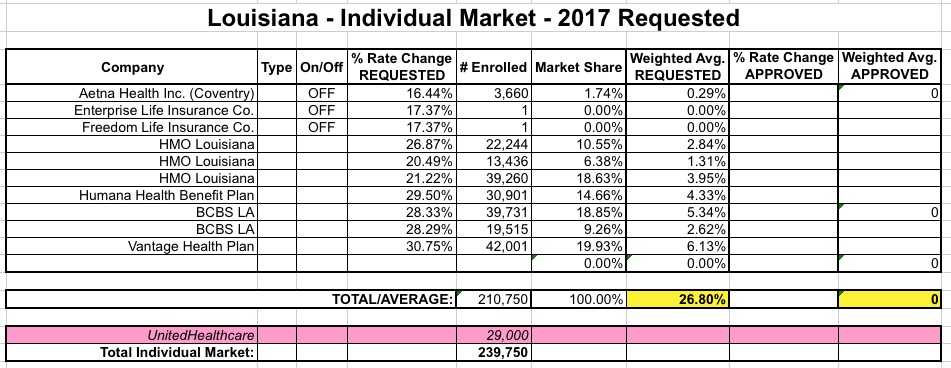

This year, about 214,000 people selected QHPs via HealthCare.Gov in Louisiana, though this has likely dropped to around 182K by now. The state's total individual market (on+off exchange, as well as grandfathered/transitional policies) was around 225,000 in 2014, and has likely increased roughly 25% since then to perhaps 280,000 total, of which around 10% is likely comprised of grandfathered/transitional enrollees. That should leave roughly 250,000 ACA-compliant enrollees statewide.

With this in mind, here's how things stack up in Louisiana for the ACA-compliant individual risk pool rate hike requests:

A few weeks ago I noted that thanks to the election of Democratic Governor John Bel Edwards (with an assist by David Vitter's diaper fetish), up to 375,000 lower-income Louisiana residents became eligible for the ACA's Medicaid expansion provision starting a month earlier than expected (June 1st instead of July 1st).

Enrollment officially started early this morning (not sure if it was right at midnight or if they had to wait until the state offices opened or whatever), and as of around 11:40am...

Gov. Edwards announces that there are already 175,000 Louisianans enrolled in the expanded Medicaid program. #lagov#lalege

— Gov John Bel Edwards (@LouisianaGov) June 1, 2016

Hmmm...last year Nebraska had 5 carriers offering individual policies, 2 of which were actually divisions of the same company (UnitedHealthcare). Since United is pulling out of Nebraska, this leaves only three companies...one of which is the mysterious "Freedom Life Insurance Co." which keeps popping up in numerous states as not having a single actual enrollee, and almost always asking for the exact same rate hike: 17.37%. What's up with that?

Anyway, Coventry (actually Aetna) appears to also be gone next year as well...or perhaps they simply haven't submitted their rate filings yet? I suspect the latter because Nebraska's total individual market was over 110,000 people as of 2014, and is likely up to over 130K this year (nearly 88,000 enrolled via the ACA exchange alone this year)...yet adding up the numbers from the official filings only totals around 30,000 people.

Back in mid-April, I posted the UnitedHealthcare State Dropout Odometer, which tracked exactly which of the 34 states which UnitedHealthcare is currently offering individual market policies in this year they'd drop out of for 2017. Instead of simply stating "we're sticking around in these states and dropping out of the rest", United decided to dole the pain out gradually, with states announcing their departure one by one over several weeks. For quite awhile, I knew that they were sticking around Nevada, New York and Virginia, with another half-dozen states in limbo status.

Today, according to the Chicago Tribune and the Minnesota Star Tribune, it looks like those three are it: They'll still be available in those 3 states, but are pulling out of the other 31 (including California, where they only have around 1,200 current enrollees via the exchange anyway). OK, that sucks, but we kind of knew about this already; it's old news for the most part.

North Carolina's individual market, which only had 5 carriers participating to begin with this year, suffered a double blow recently when both UnitedHealthcare (155,000 enrollees) and Humana (3,272 enrollees) announced that they were dropping out of the market entirely next year (Celtic is also leaving the state, but they have literally just 1 person enrolled state-wide anyway). Fortunately, nature abhors a vacuum, so Cigna Health & Life Insurance decided to join the exchange for 2017. Cigna is already selling off-exchange individual policies, but only has fewer than 1,300 people enrolled in them at the moment. There's also a carrier called "National Foundation Life Insurance" which is raising rates 17.4%...but doesn't have a single person enrolled at the moment anyway, so I'm not sure what to make of that.

It's time to take a breather from my ongoing 2017 Rate Hike Request project to check in on a couple of off-season enrollment numbers. First up is Minnesota. Here's how the QHP tally (cumulative, not currently effectuated) has gone since open enrollment ended in the Land of 10,000 Lakes (note: Michigan actually has 11,000, so there!):

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}