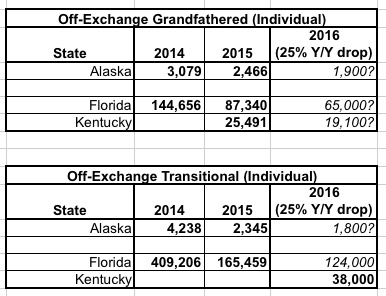

As you'll recall, until now I had data on "grandfathered" and "grandmothered" policy enrollment from 3 states: Alaska, Florida and Kentucky. However, even that limited data is kind of iffy, because most of it is from either 2014 or 2015, making it difficult to pin down the current numbers as of Spring 2016. Here's a summary of what I have so far:

Based on these numbers, I've extrapolated out to estimate perhaps 1.1 - 1.6 million grandmothered (transitional) enrollees and 800K - 1.4 million grandfathered enrollees nationally.

You'll notice that I left a blank line; that's because as always, Louise Norris has come through with some hard numbers out of The Big One: California:

@charles_gaba Got some more date from CA. It's as of 12/31/14, but they said the 12/31/15 report should be out very soon. CA has 2 reports..

As a patient, all you need to do is go to the doctor and show your insurance card. Bernie’s plan means no more copays, no more deductibles and no more fighting with insurance companies when they fail to pay for charges.

In my response, I noted that aside from anything else, getting rid of all co-pays and deductible altogether sounded a bit...off...to me. To the best of my knowledge, no other country in the world, even those which have single payer-like systems, cover 100% of everything without any out of pocket expense to the patient...and with good reason. While it doesn't specify anything about "no insurance premiums", that's kind of the core concept of any single payer system, and he specifically says that "all you need to do" is go to the doctor with your insurance card. The "premiums" are, of course, listed as a 6.2% employer premium and a special 2.2% income tax paid by households.

UnitedHealth Group Inc. plans to exit a third state Obamacare market as the insurer works to stem losses from its struggling Affordable Care Act business.

The insurer won’t sell policies through Michigan’s ACA exchange for next year, according to Andrea Miller, a spokeswoman for the state’s Department of Insurance and Financial Services. Georgia and Arkansas said last week that UnitedHealth will quit their exchanges for 2017.

...Fifteen insurers sold policies in the state for this year, U.S. data show.

Grandfathered Policies: These are non-ACA compliant policies which people were already enrolled in prior to March 2010, when the ACA was signed into law. Anyone enrolled in one of these can keep renewing them until the day they die if they wish (as long as they keep paying the premiums), or until the carrier chooses to (voluntarily) discontinue the policy.

Transitional (or "Grandmothered") Policies: These are non-ACA compliant policies which people enrolled in between March 2010 and October 2013. This category was created by President Obama and the HHS Dept. in November 2013 during the ugly "If You Like Your Plan You Can Keep It!" backlash. Basically, the ACA originally would have required that these policies be terminated as of 12/31/13. However, after a bunch of people received cancellation notices from their carrier, there was a massive backlash, leading Obama to announce an extension program.

The short version is that there were several extensions allowed, ultimately allowing insurance companies to keep these non-compliant "transitional" policies effective until as late as December 31st, 2017...depending on whether the state they operate in allowed the extensions, and if so, through what date. As a result, instead of all 5-6 million of these policies being cut off on 12/31/13, the cut-off date varies by state, by carrier and even by plan. Some states kept to the original 12/31/13 deadline; others bumped it out through the end of 2014, 2015, 2016 or took the full extension through 2017.

Don't ask me why, but I was thinking about the movie "A Few Good Men" this morning, and something has always bothered me about it.

As you'll recall, the reason Private First Class William Santiago was given the Code Red in the first place is because a) he broke the chain of command by begging everyone in the world to transfer him out of Guantanamo Bay, and b) he offered to squeal about the "fenceline incident" in return for the transfer.

OK, fair enough. But the scene which bothers me is this one, which is also the introduction to Col. Jessup:

Here's my problem: As Jessup clearly states, PFC Santiago was, by all accounts, just a shitty Marine. He simply couldn't keep up with the training. Regardless of whether it was because of a legitimate medical condition or due to him "not being properly motivated", he couldn't hack it, end of story. Furthermore, no one liked him anyway.

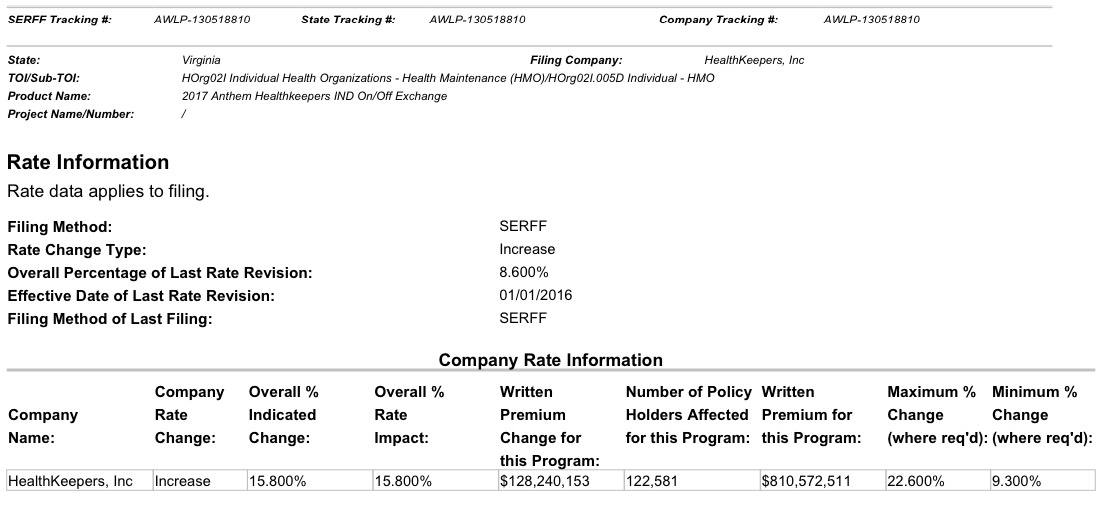

As you can see, while the requested rate increases stayed consistent throughout the various updates, the number of enrollees changed dramatically depending on which filing source I used. Case in point: Anthem/HealthKeepers Inc.

The first filing I found for Anthem HealthKeepers made it pretty clear that they're asking for a 15.8% average rate hike next year which is expected to potentially impact up to 122,581 policy holders:

Pretty cut & dry, right? Note that according to the filing that number covers current Anthem HealthKeepers enrollees both on and off the exchange, so it should cover all ACA-compliant policies.

In both cases, I've been criticized either here or via Twitter about the twin problems of high deductibles/co-pays and narrow networks. In response to the first story, people noted that the "actual" number who are uninsured is "a lot more" than 29 million because many people still can't afford the deductibles/co-pays or can't find a doctor/hospital in their network. In response to the second story, people claimed that I'm "hiding" the truth about how much policies cost for the same reasons.