New Jersey individual & small group market carriers are asking for unweighted average rate increases of 7.3% and 4.5% respectively for 2025. However, the unweighted averages don't tell the whole story--the carriers are asking for rate hikes ranging from as low as 3.8% to as high as 16.2% on the individual market, and from as low as an 18.8% reduction to a 12.3% increase for small group plans.

As is the case with far too many states these days, most of the rate filing memorandums are heavily redacted in New Jersey, making it nearly impossible to get ahold of the actual enrollment numbers, which means I have no way of running a weighted average on either market.

I should note that the 433,000 estimate for New Jersey's total individual market is based on the assumption that 90% of it is via the ACA exchange, with only 10% being enrolled off-exchange.

Nevadans Get a Preview of 2025 Proposed Health Insurance Rate Changes for Upcoming Open Enrollment

Starting today, Nevada consumers who shop for their health insurance on the individual health insurance market can view and provide comments on proposed rate changes for Plan Year 2025.

The Nevada Division of Insurance (Division) has received and made public on its website the 2025 proposed rate changes from health insurers intending to sell plans on and off the Silver State Health Insurance Exchange (the "Exchange"). The Exchange is the state agency that assists eligible Nevada residents to purchase affordable health and dental plans.

Nebraska doesn't even bother listing indy/small group plan rate filings on their own insurance department website...the link goes directly to the federal Rate Review database. The problem with this is that very few filings here are unredacted, which means it's difficult to acquire the policy enrollees for many carriers needed to run a weighted average.

Nebraska has 4 carriers on the individual market for 2025: BCBS, Medica, NE Total Care and Oscar Health. The unweighted average rate increase being requested is around 4.0%.

For the 4 Small Group market carriers, I do have enrollment data for two of them, but without knowing the other two this isn't terribly useful. The unweighted average rate change being requested there is a 9.3% increase.

The good news is that this year at least, the SERFF database has both the average rate changes as well as the 2024 effectuated enrollment for all carriers on both the individual and small group markets. There's one curiousity, however: For the small group market, UnitedHealthcare shows up in the SERFF database but doesn't appear on the federal Rate Review website.

This doesn't really move the needle much either way, however, since UHC only reports having 250 enrollees anyway.

In any event, individual market carriers are requesting average 8.3% rate increases, while small group carriers are asking for similar 8.6% hikes.

Not a whole lot stands out to me other than SSM Health Insurance apparently dropping out of the states indy market and a new carrier, Bankers Reserve Life Insurance, newly joining it.

At the same time, the Missouri small group market appears to be losing two carriers (or three depending on your POV): Aetna Health, Aetna Life and Cigna Health & Life are all missing from the 2025 filing summaries as well as the federal Rate Review database.

In any event, the MO individual market is looking at average premium reductions of 1.7% if approved as is, while small group plans are likely to increase by about 7.9% overall.

As always, these are subject to state regulatory review and approval.

Unfortunately, Mississippi is another state which provides zero useful rate filing data for my purposes (preliminary or final) prior to the Open Enrollment Period launching. The only data I have is from the federal Rate Review website, and even the filing forms there are heavily redacted, so all I can put together are unweighted averages for the 2025 calendar year.

It's worth noting that Vantage Health Plan appears to be dropping out of the individual market, while All Savers appears to be dropping out of the states small group market (at least, neither one shows up on the Rate Review site or in a SERFF search, anyway).

With that in mind, unsubsidized individual market enrollees are looking for unweighted average increases of around 1.8%, while small group carriers are hoping to increase rates by around 9.8% (again, unweighted).

They break out the filings not between Individual and small group markets or on- vs. off-exchange policies, but between rate increases over and under 10%. Normally that would be fine, but they also have multiple listings within each market for several carrier.

Not that any of that matters this year, as they don't appear to have posted any of the ACA-compliant individual market filings there anyway. I had to rely entirely on the federal Rate Review site, and the filings there still don't include enrollment data for most carriers, so the averages below are all unweighted only:

Individual Market: Around 3.0% lower (in fact, 4 of the 5 carriers on the market next year are dropping average premiums at least slightly)

Small Group Market: 9.6% higher

It's worth noting, however that Louisiana Healthcare Connections appears to be dropping out of the individual market entirely.

Kansas is another state where the annual rate filings are redacted for many of the carriers; as a result, I can only run a semi-weighted average, and even that is dependent on my estimate of the total individual market size being accurate (my general rule of thumb as long as the enhanced subsidies of the IRA are in place is that about 90% of most states individual market enrollment is on-exchange unless I have data proving otherwise).

With that in mind, the carriers on the Kansas individual market are asking for rate hikes ranging from 2.1% - 24.4%, with an estimated semi-weighted average of 8.9%.

For the small group market, I can't even run a semi-weighted average since I have no idea what the KS small group market size is overall, but the unweighted average rate hikes being requested is 14.9%.

It's also worth noting that unless I'm missing something, US Health & Life Insurance seems to be pulling out of the Kansas individual market, while both Aetna and Cigna seem to be missing from the small group market.

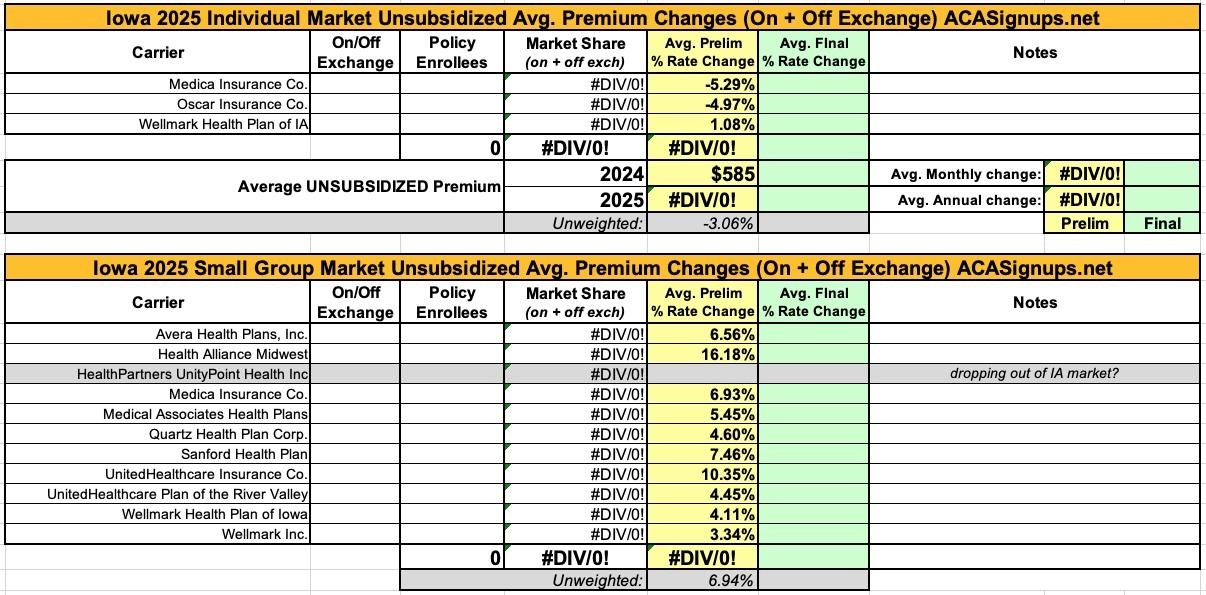

Here's the preliminary 2025 ACA individual and small group market rate filings. Unfortunately, the effectuated enrollment isn't available this year for the carriers in either market, so I can only offer unweighted averages...which include a 3.1% reduction on the indy market and a 6.9% increase for small group enrollees.

the only other noteworthy item is that it looks like HealthPartners UnityPoint is dropping out of Iowa's small group market next year...but with 9 other carriers participating there's still plenty of options for that population.

Georgia's health department doesn't publish their annual rate filings publicly, but they don't hide them either; I was able to acquire pretty much everything via a simple FOIA request. Huge kudos to the GA OCI folks!

Georgia's individual market has grown dramatically over the past two years; it went from 660,000 in 2023 to 813,000 people in 2024 to a stunning 1.3 MILLION this year. The weighted average rate increase for unsubsidized enrollees will go up 9.9% if state regulators approve all of the carrier requests as is.