Updated: When enrolling in ACA exchange coverage, don't accidentally apply for Medicaid unless you mean to.

Mon, 11/25/2024 - 4:03pm

Yep, my wife & I screwed up royally. Yes, I know: I'm "The ACA Guy" and yes, it's incredibly embarrassing to tell this story, but I'm doing so in the hopes of helping others avoid making the same mistake.

It's been several years since we enrolled in an ACA policy ourselves via HealthCare.Gov, since we were enrolled in my wife's student plan up until recently (she returned to college to get her master's degree). The last few times we were able to enroll or renew our policies without any issues, so we assumed it wouldn't be an issue this time.

However, there seem to have been a few changes to some of the questions during the application process, and one of them threw us for a loop.

In the household income section of the application process, Healthcare.Gov asks both how much you expect to earn this month specifically (November 2024) as well as how much you expect to earn for all of 2025.

It was the first of these questions which is what caused the problem for us.

You see, both my wife and I are self-employed, which means we have highly variable incomes--we may earn $10,000 one month but not earn anything the next.

From the headline of this blog post you can probably see where I'm going with this.

We entered "$0" for our expected income for November (as it happens, that ended up not being the case anyway since a payment I didn't expect to show up until December ended up showed up earlier than expected). We then entered our normal projected annual income for 2025.

However, when we completed the application process, HealthCare.Gov informed us that we weren't eligible for any ACA financial subsidies...but were likely eligible for Medicaid or CHIP.

Ut-oh.

I immediately realized what our error must have been--it seems pretty clear that the system assumed that we were claiming that we earn nothing--so we went back & re-applied, this time entering a more reasonable monthly income for November (ie, roughly 1/12th of what our typical annual income is).

This time the application went through properly, displayed our estimated monthly APTC subsidies, and we were able to go ahead and enroll in a Blue Cross Blue Shield of Michigan Silver PPO policy without any further issues.

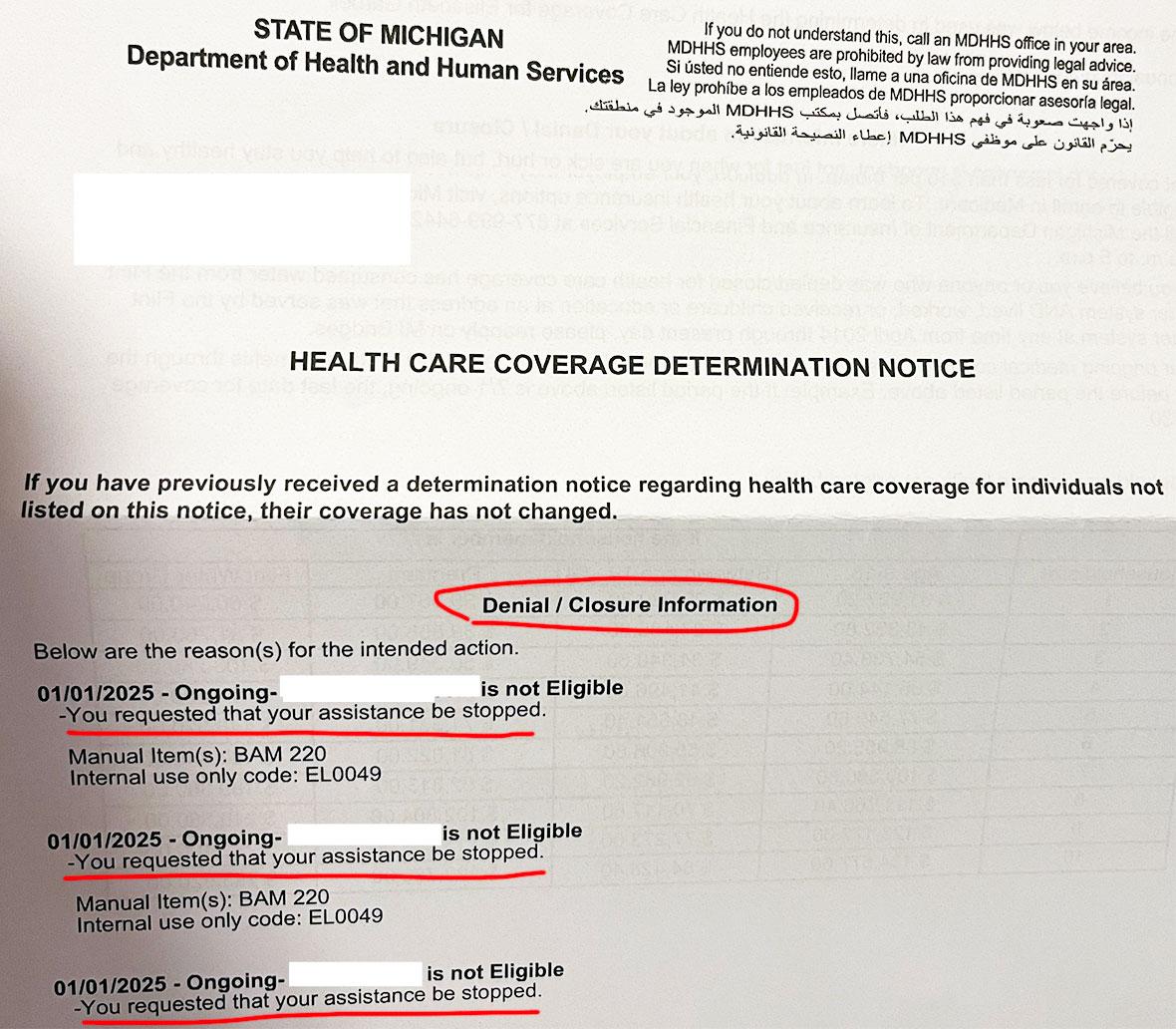

I assumed all was well...until about a week ago, when I started receiving mail from the Michigan Dept. of Health & Human Services telling me that they need us to provide various documentation, verification of our identities & income by December 2nd...and a few days later, I received a notice telling us that we have to choose a Medicaid plan by December 5th or a plan will be selected for us. But wait, there's more: MI DHHS has even already sent us "MI Health" cards.

That's right: The Michigan Dept. of Health & Human Services thinks that we applied for Medicaid even though that wasn't our intention at all, we don't want it and we're absolutely not eligible for it.

So, tomorrow I get to call up MI DHHS and hopefully get them to terminate the Medicaid account, hopefully without screwing up either our exchange coverage or APTC subsidies and without my wife or I being accused of trying to commit Medicaid fraud.

Oh yeah...and I get to do this just 2 days before Thanksgiving, which means I have to hope that the MI HHS office is open when I call and that the issue doesn't get delayed into December, turning into a voicemail/red tape hellscape situation.

Anyway, consider this a perfect example of what a royal pain in the ass administrative burden can be when it comes to healthcare coverage: If The Obamacare Guy could mess up his own Obamacare enrollment, imagine how easy it is for others who understand less about the system to do so?

I'll follow up when I have a further development to report...

UPDATE 11/26/24: OK, I heard back from MI DHHS this afternoon and they've supposedly gone ahead and cancelled our Medicaid account. I'm supposed to receive a confirmation letter in the mail sometime next week. It's supposed to be cancelled effective December 1st (before any of the deadlines I noted above)...but due to it being so close to the end of the month and being a holiday weekend, there's a possibility that my family will technically be "enrolled" in Medicaid through January 1st. I was told that as long as we don't actually attempt to utilize any Medicaid services there shouldn't be any issues--we shouldn't be charged any fees and it shouldn't screw up either our existing insurance coverage or our upcoming 2025 exchange policy/subsidies.

We'll see...

UPDATE 11/30/24: The good news is that I received the confirmation from MI DHHS that our Medicaid "enrollment' has been terminated. The bad news is that it looks like the termination won't become effective until January 1st, which means I may still have to deal with them for December (since they're supposedly going to "assign us a plan" if we don't choose one).

I'll post another follow-up if there's any further noteworthy developments good or bad.

Advertisement