Yesterday I estimated that total #ACATaxTime-specific enrollments were likely around 200,000. Today, thanks in part to CNBC's Dan Mangan, I can pin this down even further. The bold-faced states are the ones where the number is provided by Mangan's report:

But there’s another potential twist to the tale: Just as he is now seeking to get on Obamacare, he could very well find himself unable to sign up for coverage, if the Supreme Court rules for the challengers in King v. Burwell next month.

...an HHS official tells me that if he can get his income up a bit — it reportedly fluctuates — he could probably qualify for a category that would allow him to apply for Obamacare again before next year’s open enrollment period.

But if the Court strikes subsidies in three dozen states on the federal exchange — one of which includes South Carolina — it could put Obamacare even further out of reach for Lang.

Of course, if the Supreme Court decides to blow up the entire system with an adverse King v. Burwell decision, all bets are off, as none of the “requested” rate changes will have any meaning whatsoever in the 34 states without their own exchange.

...In short, if the King plaintiffs win, prepare for one heck of a mess next year.

Yesterday I noted that a seemingly minor announcement (HHS tweeting that the final #ACATaxTime tally for the federal exchange from 3/15 - 4/30 ended up being 147,000 people) had a greater significance than that, because tacking that onto the grand national total brought the official tally up to the 12 million milestone.

Personally, this didn't mean much to me because I estimate that the actual total (including unreported numbers from various exchanges) is more like 12.4 million or higher anyway...and on the flip side, the number of people actually paid up with effectuated enrollments is more like 10.1 million, and has been for a month or so now. Still, officially hitting the 12 million mark seemed worth noting, so I did so.

An hour or so ago, Luis Lang, who earlier today announced his support of Single Payer healthcareand his decision to leave the Republican Party (specifically over their obstruction of the Affordable Care Act) posted the following update on his GoFundMe account:

Lifelong Republican Turns On His Party, Embraces Obamacare

Luis Lang, who is currently crowdfunding for medical expenses that he can’t afford because he didn’t sign up for insurance under Obamacare, has become a viral sensation. However, the 49-year-old South Carolina resident says he doesn’t want to be the poster child for the Republican Party’s opposition to health care reform anymore.

Many people both here and over at Daily Kos have criticized me, either for donating a few bucks ot Mr. Lang in the first place or alternately, for coming down so hard on the guy in my blog posts. Some thought it was a waste of time (and money) to help the guy out, while others thought it was an equal waste of time/breath to chastize him, figuring that it'd fall on deaf ears. Still others thought that it's inappropriate to donate money with one hand while berating him with the other. Well, guess what?

After all the fuss and bother made over the #ACATaxTime Special Enrollment Period by myself and others, the final number of QHP selections was announced in the most understated way possible:

From March 15 to April 30, 147,000 consumers signed up for coverage through http://t.co/eTfU7hSMWR using the tax special enrollment period.

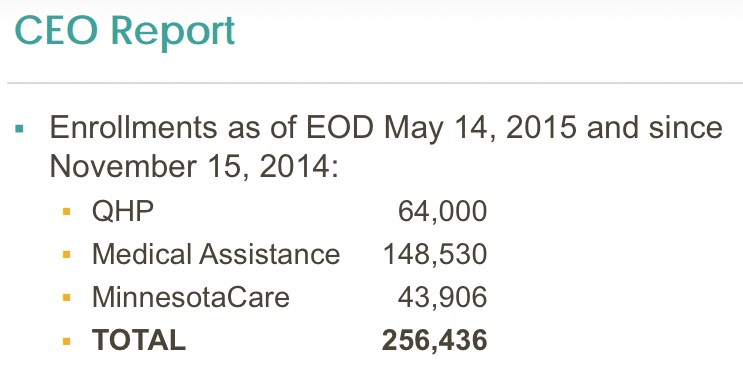

Hot off the presses, the Minnesota ACA exchange, MNsure, just held their monthly board meeting and released some new enrollment numbers:

That precise 64,000 QHP number is up 2,126 since April 13, while Medicaid and MinnesotaCare are (combined) up a whopping 34,538 people, which is pretty impressive.

As you may have noticed, I've been posting a bunch of 2016 Rate Change Request posts over the past week or so. Last week I wrote about Oregon, Washington State, Iowa and Connecticut. This week I've added Michigan and the District of Columbia, and just this morning I added Vermont and Maryland. Other state numbers will be popping up left and right over the next couple of weeks.

To try and avoid confusion, my latest exclusive piece over at healthinsurance.org is a primer of sorts on what to be on the lookout for when you start seeing scary-sounding newspaper headlines about "massive rate hikes!" for 2016.

Spoiler: They may be accurate, or they may be full of hot air. Check it out!

Maryland's rate request website is an exercise in frustration. At first glance, it looks very cut and dried: A full table of each health insurance company, broken out by either individual or small group market, whether the filing is for policies sold on or off the ACA exchange, and the "average % change requested", along with direct links to the actual filing documents (where, presumably, I can dig up the crucial enrollment numbers, which are vital to determining the weighted average rate requests).

Unfortunately, once you get into the actual documents...they're completely scattershot. Some companies list the number of enrollees who would be impacted by the requested rate changes; some don't. That makes it impossible to determine the market share, which in turn means there's no way of weighting the average.