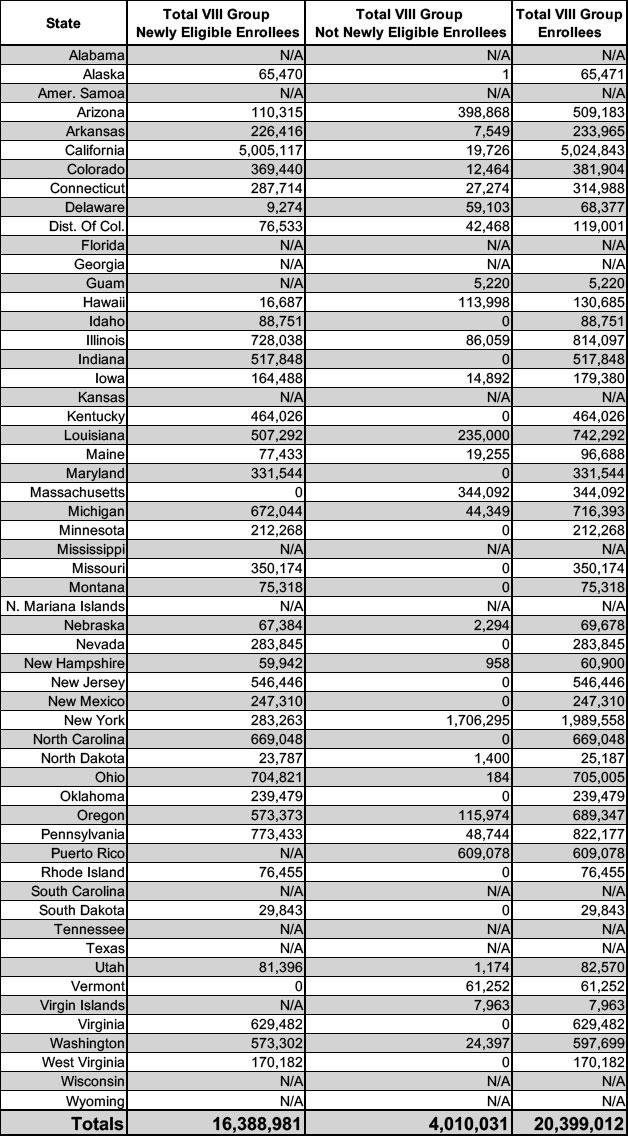

According to the new report, total enrollment from December 2024 through June 2025 dropped by 517,000 people, or roughly 2.5%, standing at 20.4 million nationally as of last June, so it doesn't look like the Trump Admin has started cooking these particular books, at least not yet.

Limited-time marketplace transition year Special Enrollment Period

This year, with the multitude of unique factors impacting access and affordability, Get Covered Illinois is using its authority as a state-based marketplace to offer a limited-time Special Enrollment Period for customers previously enrolled in a 2025 health plan through HealthCare.gov.

Who Qualifies for this Special Enrollment Period?

To qualify for this limited-time Special Enrollment Period, the enrollee must:

have been automatically renewed in a 2026 health plan through Get Covered Illinois, and

have not made an active plan selection or terminated/canceled their coverage during this past Open Enrollment Period, and

have not claimed their Get Covered Illinois account by February 1, 2026.

How long is this Special Enrollment Period available?

Back in December, I issued a strong warning that the official 2026 ACA Open Enrollment Period data would have to be taken with a huge grain of salt, since the actual effectuated enrollment data would likely take much longer to know:

...I'm bringing all of this back up again today because I strongly suspect that the situation is about to reverse itself, with the Trump Administration already preparing to brag about impressive-sounding ACA enrollment numbers for 2026 in spite of the enhanced tax credits expiring less than 60 hours from now...even though the actual negative impact of the expiring tax credits (along with several other administrative policy changes made by CMS this year) likely won't be known for several months after Open Enrollment officially ends in January.

Top Senate negotiators said an effort to renew expired healthcare subsidies had effectively collapsed, likely ending the hopes of 20 million Americans that the tax-credit expansion could be revived and lower their monthly insurance premiums.

Talks had centered on a proposal from Sens. Bernie Moreno (R., Ohio) and Susan Collins (R., Maine) to extend a version of the enlarged Affordable Care Act subsidies for at least two years, while cutting off higher-income people from participating and eventually giving enrollees the option of putting money into health savings accounts. It also would eliminate zero-dollar premium plans. But lawmakers from both parties now say the chances of a deal have all but evaporated.

“It’s effectively over,” Moreno said Wednesday. Sen. Bill Cassidy (R., La.)—the architect of an adjacent plan—agreed. While Collins declined to be as definitive, she did say that it was “certainly difficult.”

The Maryland Health Benefit Exchange has their own Open Enrollment dashboard which, while not providing nearly as much data as New Mexico's, at least breaks out the top-line data. With the 2026 Open Enrollment Period (OEP) now over in the Old Line State, here's what their final numbers look like (barring any last-minute clerical corrections):

Total Renewals: 236,338

New Enrollees: 47,815

Total Enrollments: 255,612

Disenrollments (already subtracted from renewals)

67.4% are subsidized; 32.6% are unsubsidized

They also break out total enrollment by county, which isn't terribly relevant to me.

Final 2025 OEP enrollment in Maryland was 247,243, so this represents a 3.4% QHP selection increase vs. last year, in spite of the enhanced federal tax credits expiring...

MNsure, Minnesota's state-based ACA exchange, has posted their January Board Directors Meeting presentation, which includes the final 2026 Open Enrollment Period tally along with a bunch of other data points of interest:

Plan Year 2025 (November 1, 2024 – December 31, 2025)

Total (Medical Assistance, MinnesotaCare, QHP) 357,227

The 2026 ACA Open Enrollment Period is now officially over in every state.

For most Americans, if you missed the deadline to enroll in ACA exchange healthcare coverage, your options are pretty limited at this point...but there are some exceptions, so let's take a look.

After calling them out for some sloppy summary numbers which understated the enrollment drop by over 144,000 people out of the gate, I delved into the meat of their false argument:

...the above is fairly minor compared to the most egregiously misleading claim in the WSJ piece, which appears in the next paragraph:

The Congressional Budget Office’s ObamaCare baseline in 2024 assumed 18.9 million people would enroll in plans this year if the enhanced subsidies vanished.