NOTE: I've decided to make "Short Cuts" the standard name for ACA-related stories which are interesting but which I just don't have time to do full write-ups on. I've also given up on trying to cram the headlines of each story into the blog entry title.

ObamaCare outreach campaigns across the country are diving deeper into the hard-to-reach uninsured populations such as rural areas with hopes of driving up enrollment in its second year, several state directors said Wednesday.

“We have a much better sense because of data from the federal government on where are the uninsured,” Ryan Barker, vice president of health policy for the Missouri Foundation for Health, said in a conference call hosted by Families USA.

The Michigan Primary Care Association said it is trying to “fill the gaps” of health insurance coverage by relocating a majority of its staff to rural, less-populated areas.

I was feeling kind of sour after writing my previous post about Sen. Tom Harkin's unhelpful comments today, so thanks to contributor "Dee" for cheering me up with this bit of idiocy from the Daily Caller from a woman named Sarah Hurtubise:

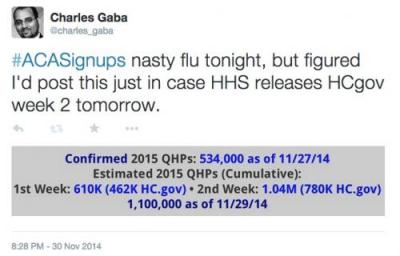

Obamacare Sign-Ups Stall In Week Two

The number of Americans signing up for Obamacare coverage on HealthCare.gov slowed significantly in the second week of the open enrollment season for the health-care law.

Just over 303,000 people chose plans on HealthCare.gov between Nov. 22 and Nov. 28, down from 462,125 who selected insurance coverage on the federal website during its first week, the Department of Health and Human Services announced Wednesday.

...The number of total applications submitted dropped by half in comparison to the first week. While over one million applications were submitted during the first week, that total fell to just 520,427 in the next seven days.

Today, he's followed up by IA Sen. Tom Harkin, who has the following incredibly insightful wisdom to spread to Democrats throughout the land:

“We had the votes in ’09. We had a huge majority in the House, we had 60 votes in the Senate," Harkin told The Hill, saying that the first Congress of President Barack Obama's administration should have passed “single-payer right from the get go or at least put a public option (which) would have simplified a lot.”

Huh. OK, I wasn't expecting MNsure's update until Friday this week (they put it out on Wednesday last week due to Thanksgiving), but fair enough:

Latest Enrollment Numbers

December 3, 2014

MNsure will release 2015 enrollment metrics weekly, and will present a more robust metrics summary to the MNsure Board of Directors at each regularly-scheduled board meeting. During weeks that MNsure is closed on Friday, the enrollment metrics update will be released earlier in the week.

Health Coverage Type Cumulative Enrollments

Medical Assistance 8,874

MinnesotaCare 2,954 Qualified Health Plan (QHP) 7,106

TOTAL 18,934

MNsure is running around 54% higher than their 2014 daily average so far, FWIW.

Massachusetts continues to steam ahead: Assuming at least 48.5% of QHP determinations have already selected policies, they should be at roughly 26,000 QHPs through last night, plus another 45,687 added to Medicaid.

If so, MA has reached 82% of their 2014 total in 18 days, and is on their way to a bare minimum of 134K even without the double-surges around 12/23 and 2/15.

Again, I'm expecting as many as 300K Bay Staters before the dust settles in February.

Over the summer, five different respected national healthcare studies agreed that the overall uninsured rate had plummeted by at least 25% from last fall through the end of June, 2014. The methodology varied a bit from one to another; some included all adults, others only included those under 65. Some included children under 18, others didn't. Some used the September 2013 as the starting point, others started with December 2013. Even with all of these variables, though, the consensus was a 25% reduction, from roughly 42.3 million down to around 31.3 million, give or take.

Today, one of the five, the Urban Institute, released an updated study which includes the third quarter of 2014, and as expected, the trend has continued:

On the one hand, moving from 2,000 in the first 3 days to a minimum of 6,000 (likely more like 10K, since the 6K refers only to "accounts" not "people") in the first 17 days is a perfectly reasonable point for Washington to be at right now.

Today, the Exchange identified an error affecting 6,000 customer accounts enrolled in Qualified Health Plans. Early analysis indicates that our system integrator, Deloitte, ran an automated enrollment cancellation process in error. The affected accounts, which are a portion of the total number of customers who are enrolled in coverage starting on Jan. 1, 2015, experienced an erroneous cancellation of both their enrollment and payment for 2015 coverage.

Oops.

Well, on the plus side, the rest of the PR makes it clear that a) they're on top of it, b) it's gonna get resolved ASAP and c) it looks like this screw-up was Deloitte's fault, not the actual exchange itself (they call them out by name, which is noteworthy).

Colorado's first official enrollment report is simple, to the point, and includes not only new Medicaid/CHIP data after all (I was concerned that they'd stopped doing so, but apparently not), but also includes a handy 2015 vs. 2014 comparison chart, the SHOP number and even the number of QHP enrollees receiving tax credits/cost sharing!

In fact, the only gripes I have here are the lack of a new vs. renewal breakout (which it looked like they were going to include at first). They also don't include Medicaid/CHIP for 2014, but I already know that number went up 310K so far this year.