IF the amount of excessive profit going into the kitty was greater than the amount of excessive losses, the federal government would have paid out what was owed and keep the difference, in which case it was conceivable that the feds would actually profit off of the program.

IF, instead, the profit was less than the loss, the government would have to pay out the difference.

Unfortunately, as it happens, the second scenario is how things played out in 2014...as well as in 2015, and, most likely, 2016 as well.

When I last checked in on Colorado, they were reporting 2017 enrollments at a rate 30% faster than last year (16,305 in 13 days vs. 12,496 in the first 13 days last year).

Today they didn't issue an official update, but did give enough to piece together an estimate via an email to their enrollees:

Dear Connect for Health Colorado Stakeholders,

As we approach the Thanksgiving holiday, we’re busy as ever enrolling customers. In fact, enrollments are outpacing our numbers by more than 25 percent over this time last year, with our biggest day falling the day after the election. And, this is a trend we’re seeing nationally.

While the recent election has raised a lot of questions about the future of healthcare, what remains constant and true is the importance of protecting the health and financial future of our customers. Broken bones, disease and other chronic conditions aren’t political, but can happen at any time and in some cases, are preventable with access to care and health insurance. Our dedication to helping customers remains as strong as ever.

Two months before President-elect Donald Trump begins his attempt to repeal the Affordable Care Act, the Obama administration and its allies are making an aggressive final push to sign-up some of the program’s most reluctant customers -- young people.

Healthy and new to the workforce, the “young invincibles” -- people aged 25 to 34 -- represent the highest uninsured rate of Americans, according to a survey released in November by the Centers for Disease Control and Prevention. While coverage of people in that range has grown under Obamacare, the group has for the last five years had the highest rates of uninsurance compared to other age bands.

It's a good story, but there's one section in particular with a line which will make anyone with the slightest idea about how insurance works wince:

On the one hand, starting in January, the Republican Party will have complete control over both the U.S. House and Senate, Donald Trump will be sworn in as President, and the entire lot have promised repeatedly to kill the Affordable Care Act, aka "Obamacare".

On the other hand, the GOP hasn't managed to figure out what the hell they plan on actually replacing the ACA with (if anything), even though they've had over 6 years to come up with something and have voted to repeal it dozens of times. They insist that the ACA is a complete disaster; for years they refused to admit that it helped anyone; more recently they've grudgingly admitted that it helps some people, although they still claim that it hurts more than it helps.

In light of this, the Center for American Progress Action Fund has whipped up a simple website, ACAWorks.org, in which they ask people who have been helped by the ACA to let them know what Obamacare has meant to them.

So, the day after the election, I noted that on top of the rest of the awful, there's another fun tidbit: Due to the nature and timing of the ongoing House vs. Burwell lawsuit, it's conceivable that President-elect Donald Trump (See? I'm starting to get used to typing that!) could effectively wipe out most of the ACA immediately upon taking office by simply giving up on fighting the lawsuit and stopping Cost Sharing Reduction subsidies as early as February 1st.

This, in turn, would not only cause havoc across the individual insurance industry, it would also trigger an "escape clause" among the carriers, potentially (subject to whatever the state laws allow) letting them immediately cancel their policies. As in, the currently-in-effect policies which people had just had go into effect a month earlier. And this would have nothing to do with any action taken on the part of the Republican-held Congress.

How many people could potentially see their policies yanked out from under them?

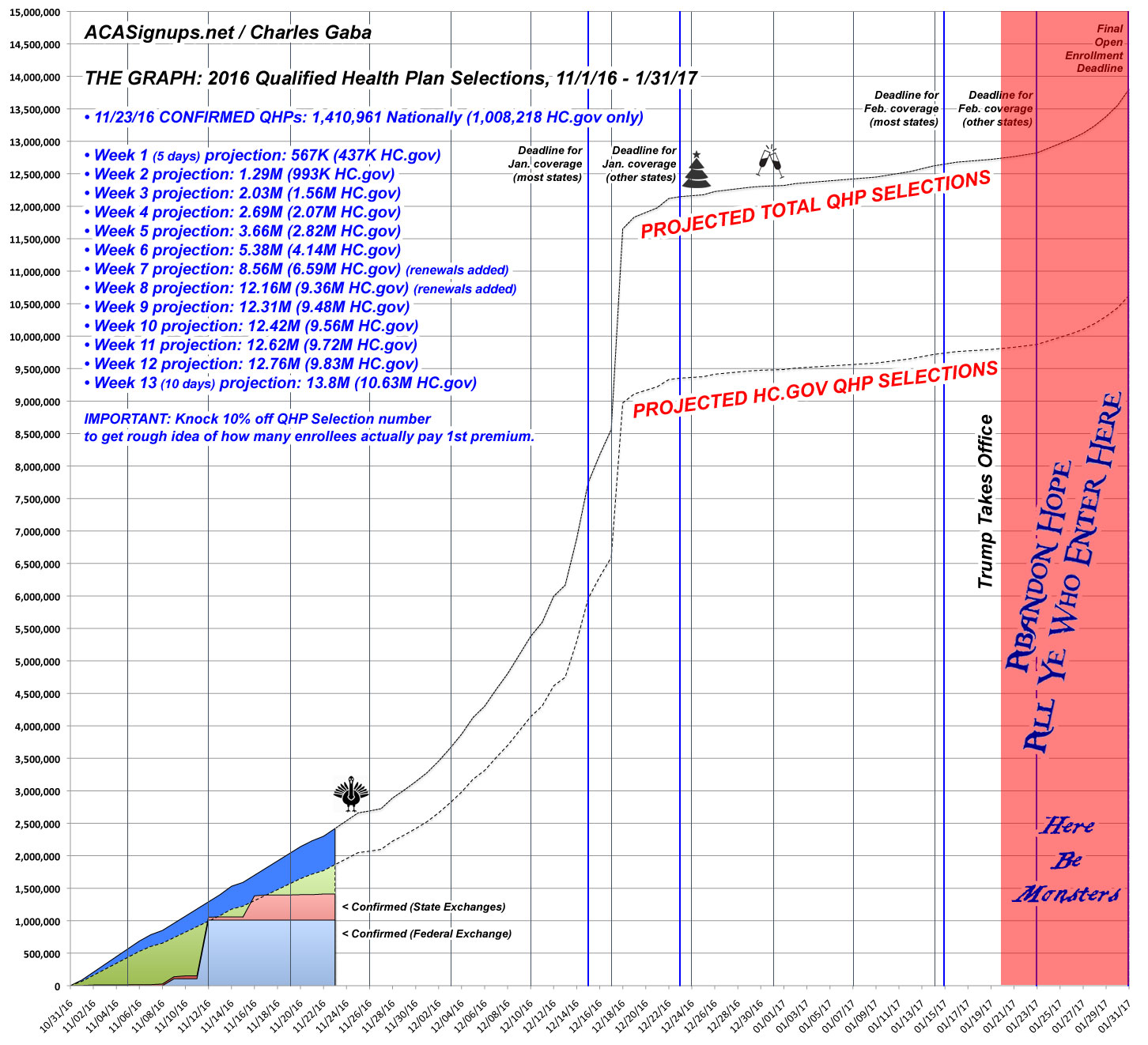

Just another update: I'm fairly certain that QHP selections via HealthCare.Gov (covering 39 states) has broken 1.7 million people, with an additional 500,000 having enrolled via the 12 state-based exchanges for a total of around 2.2 million as of tonight.

The confirmed tally stands at just over 1.4 million thanks to a small update out of Minnesota.

I expect things to slow down significantly over the holiday weekend (Thursday - Sunday) before ramping back up again next week.

UPDATE: As of Wednesday night (11/23/16), I estimate the grand total is now up to around 2.4 million nationally, 1.8 million via HC.gov.

Minnesota continues to enroll people at a breakneck pace (fortunately, broken necks are covered by Obamacare). Things have slowed down somewhat from the first few days, but they're still signing people up at a rate 3.5x faster than they did last year's 404/day due mainly to their unique "enrollment cap" situation:

28,000 Minnesotans Enrolled in Individual Plans Through MNsure Since the Start of Open Enrollment November 21, 2016

ST. PAUL, Minn.—Below is an update to MNsure's 2017 open enrollment period. Within the first three weeks of open enrollment, more than 28,000 Minnesotans have enrolled in health coverage.

Since the start of open enrollment, there have been:

A few days ago I noted that up to 50,000 South Dakota residents who previously held out at least had some hope that the state might expand Medicaid under the ACA next year have already had that hope yanked out from under them like a rug:

A proposal to expand a federal health insurance program for needy people could be off the table following the results of Tuesday's election.

The victory of Republican Donald Trump, who has called for a repeal of Obamacare, along with the increasingly conservative Republican make-up of the South Dakota state Legislature could thwart Gov. Dennis Daugaard's efforts to expand Medicaid in the state.

In Depressed Rural Kentucky, Worries Mount Over Medicaid Cutbacks

For Freida Lockaby, an unemployed 56-year-old woman who lives with her dog in an aging mobile home in Manchester, Ky., one of America's poorest places, the Affordable Care Act was life altering.

The law allowed Kentucky to expand Medicaid in 2014 and made Lockaby – along with 440,000 other low-income state residents – newly eligible for free health care under the state-federal insurance program. Enrollment gave Lockaby her first insurance in 11 years.

"It's been a godsend to me," said the former Ohio school custodian who moved to Kentucky a decade ago.

...But Lockaby is worried her good fortune could soon end. Her future access to health care now hinges on a controversial proposal to revamp the program that her state's Republican governor has submitted to the Obama administration.

With the repeal of the ACA supposedly looming next year, it's worth remembering that the ACA was based in large part on a state-level program in Massachusetts, implemented by, of course...Mitt Romney. Obviously there are a lot of differences beyond simply ramping "RomneyCare" up to the national level, but at least in terms of the "3-legged stool" of the ACA exchanges (guaranteed issue, individual mandate, subsidies to help lower income enrollees), it's essentially the same.

If the law really is repealed at the federal level, some blue states where it's working pretty well would likely switch back to their own state-level versions. In addition to Massachusetts presumably just reverting back to RomneyCare again, states like California, Washington State and Connecticut seem like likely contenders.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}