How much did Marco Rubio screw the insurance market? $8.3 billion and counting.

Thu, 11/24/2016 - 1:43am

As anyone who's been following the ongoing ACA Risk Corridor Massacre saga knows, the program was designed to help insurance carriers participating in the ACA exchanges smooth over the rough patches during the first 3 years by transferring a chunk of the profits from carriers which did excessively well over to carriers which did excessively poorly. Here's an overview of how the program was supposed to work, and what went wrong; the short version is this:

- IF the amount of excessive profit going into the kitty was greater than the amount of excessive losses, the federal government would have paid out what was owed and keep the difference, in which case it was conceivable that the feds would actually profit off of the program.

- IF, instead, the profit was less than the loss, the government would have to pay out the difference.

Unfortunately, as it happens, the second scenario is how things played out in 2014...as well as in 2015, and, most likely, 2016 as well.

How bad was it? Well, in 2014, the amount paid into the system by winner carriers was $362 million, while the amount owed to the loser carriers added up to $2.87 billion...leaving $2.51 billion in IOUs.

Under the original Risk Corridor agreement, the federal government was supposed to pay out that $2.5B regardless, either making up the difference in the next two years or simply having to eat the loss if things didn't work out.

Unfortunately, Marco Rubio and the Congressional Republicans decided to change the Risk Corridor rules in the middle of the game (literally in the middle of the 2015 Open Enrollment Period), during the infamous CRomnibus bill debate. They slipped in an amendment to the "must-pass" continuing resolution bill (the one needed to keep the government running at all) which prevented the government from making good on any Risk Corridor shortfall payments. This meant that HHS was unable to pay that $2.5 billion balance owed to the carriers. As a result, they only ended up receiving 12.6¢ of what was owed to them.

The HHS Dept. tried to mitigate the damage by pointing out that there were still 2 more years in the program; any Risk Corridor revenue generated in 2015 would go to cover the remaining balance owed from 2014 first.

Unfortunately, that's not working out too well either:

Date: November 18, 2016

Subject: Risk Corridors Payment and Charge Amounts for the 2015 Benefit Year

Background:

Section 1342 of the Affordable Care Act directs the Secretary of the Department of Health and Human Services (HHS) to establish a temporary risk corridors program that provides issuers of qualified health plans (QHPs) in the individual and small group markets additional protection against uncertainty in claims costs during the first three years of the Marketplace.

HHS established a three-year payment framework for the risk corridors program and outlined the details of this payment framework in our April 11, 2014 guidance on Risk Corridors and Budget Neutrality. 1 As set forth in that guidance, if risk corridors collections for a particular year are insufficient to make full risk corridors payments for that year, risk corridors payments for the year will be reduced pro rata to the extent of any shortfall. Because risk corridors payments for the 2014 benefit year exceeded risk corridors collections for that benefit year, risk corridors collections for the 2015 benefit year will be used first towards remaining balances on 2014 benefit year risk corridors payments.

On September 9, 2016, HHS published guidance on Risk Corridors Payments for 2015, stating that we anticipated that all 2015 benefit year collections would be used toward remaining 2014 benefit year risk corridors payments, and that no funds would be available at this time for 2015 benefit year risk corridors payments. 2 Today, we are confirming that all 2015 benefit year risk corridors collections will be used to pay a portion of balances on 2014 benefit year risk corridors payments.

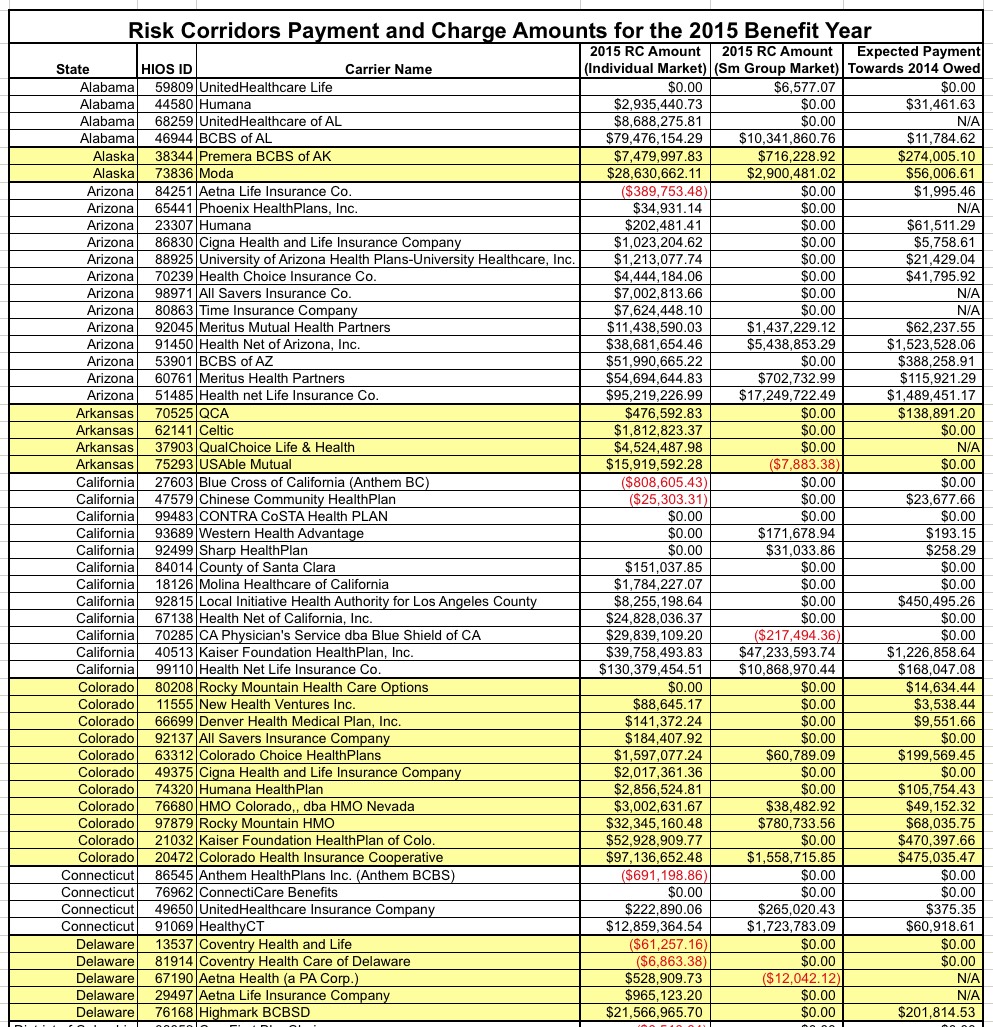

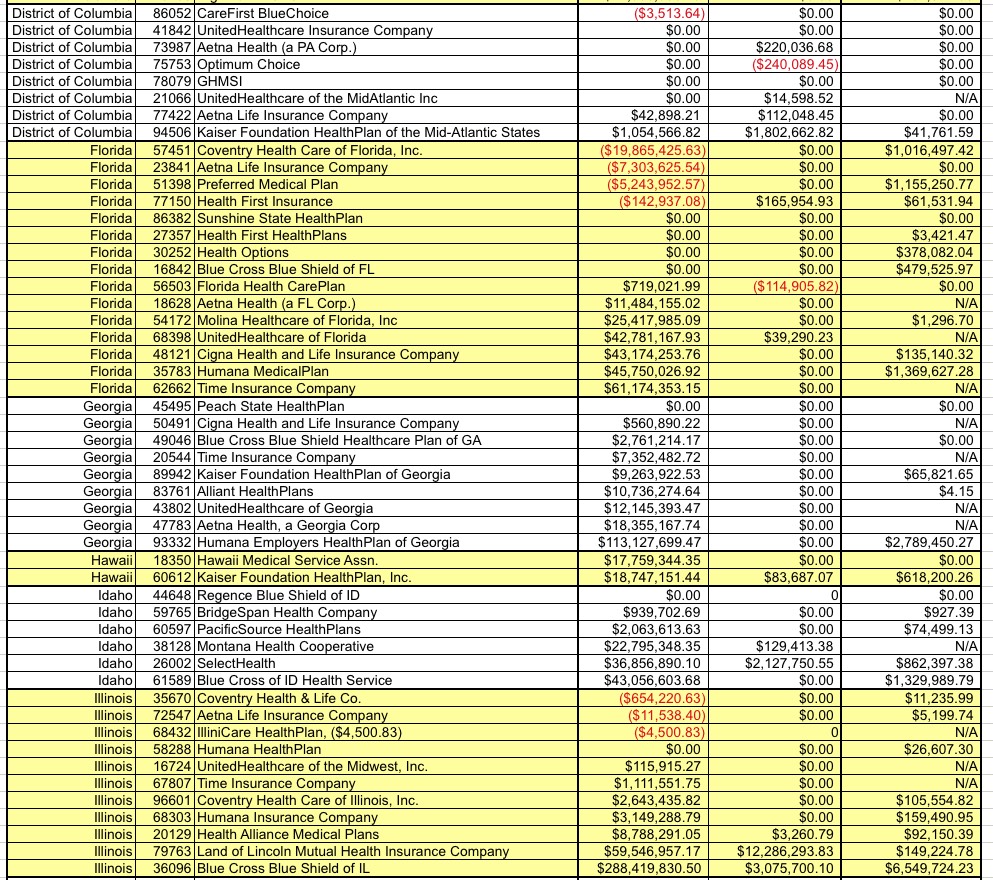

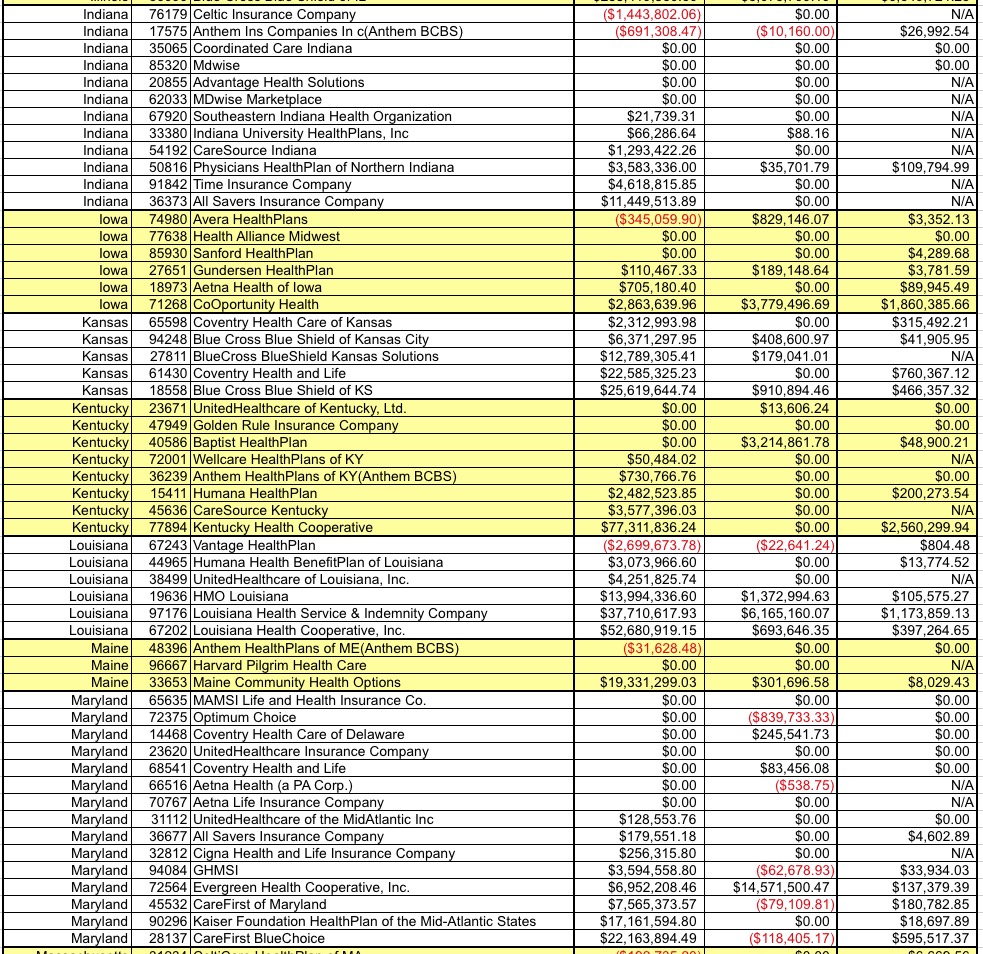

We are also announcing issuer-level risk corridors payments and charges for the 2015 benefit year. The tables below show risk corridors payments and charges calculated for the 2015 benefit year, by State and issuer, and the additional amount based on anticipated 2015 risk corridors collections that HHS expects to pay towards the calculated 2014 benefit year payments.3 Pursuant to 45 CFR 153.510(g), the 2015 benefit year risk corridors amounts listed in this report include the direct adjustment for issuers that reported certified estimates of the cost-sharing reduction portion of advance payments that were lower than the actual CSRs provided for the 2014 benefit year (as calculated under CSR reconciliation for the 2014 benefit year). On November 17, 2016, HHS notified issuers subject to the direct adjustment to 2015 benefit year risk corridors amounts of the calculated adjustment amount, consistent with guidance issued on September 15, 2016.4

Risk corridors payments are reduced pro rata based on risk corridors collections received. HHS intends to collect the full 2015 risk corridors charge amounts indicated in the tables below. HHS is collecting 2015 risk corridor charges in November 2016, and will begin remitting risk corridors payments to issuers in December 2016, as collections are received.

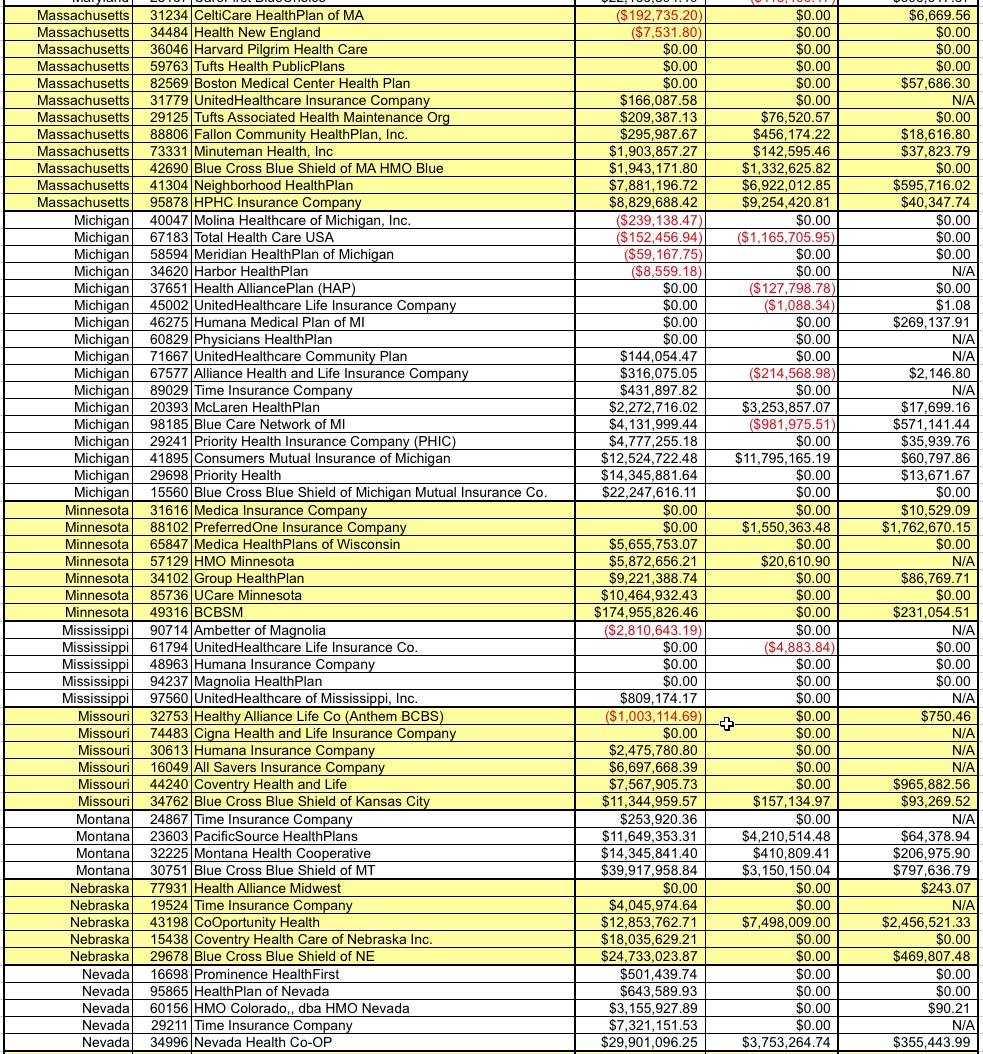

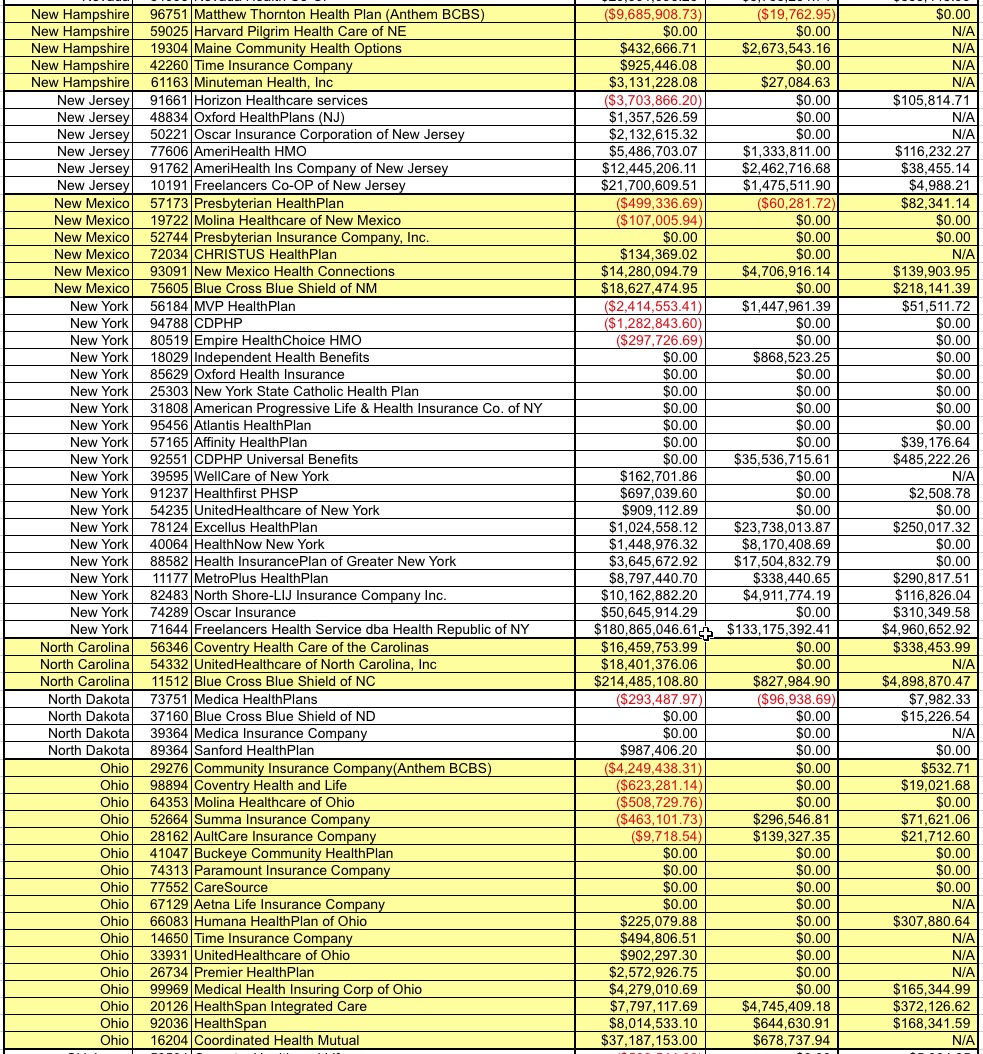

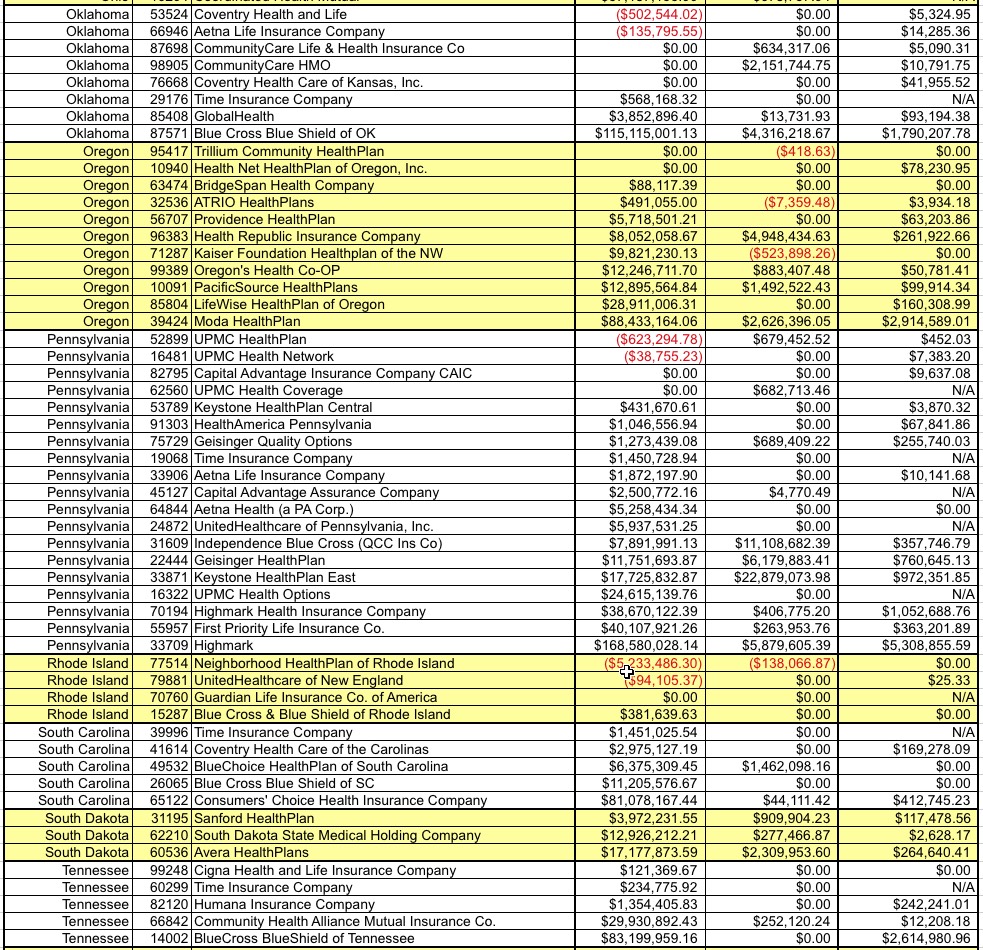

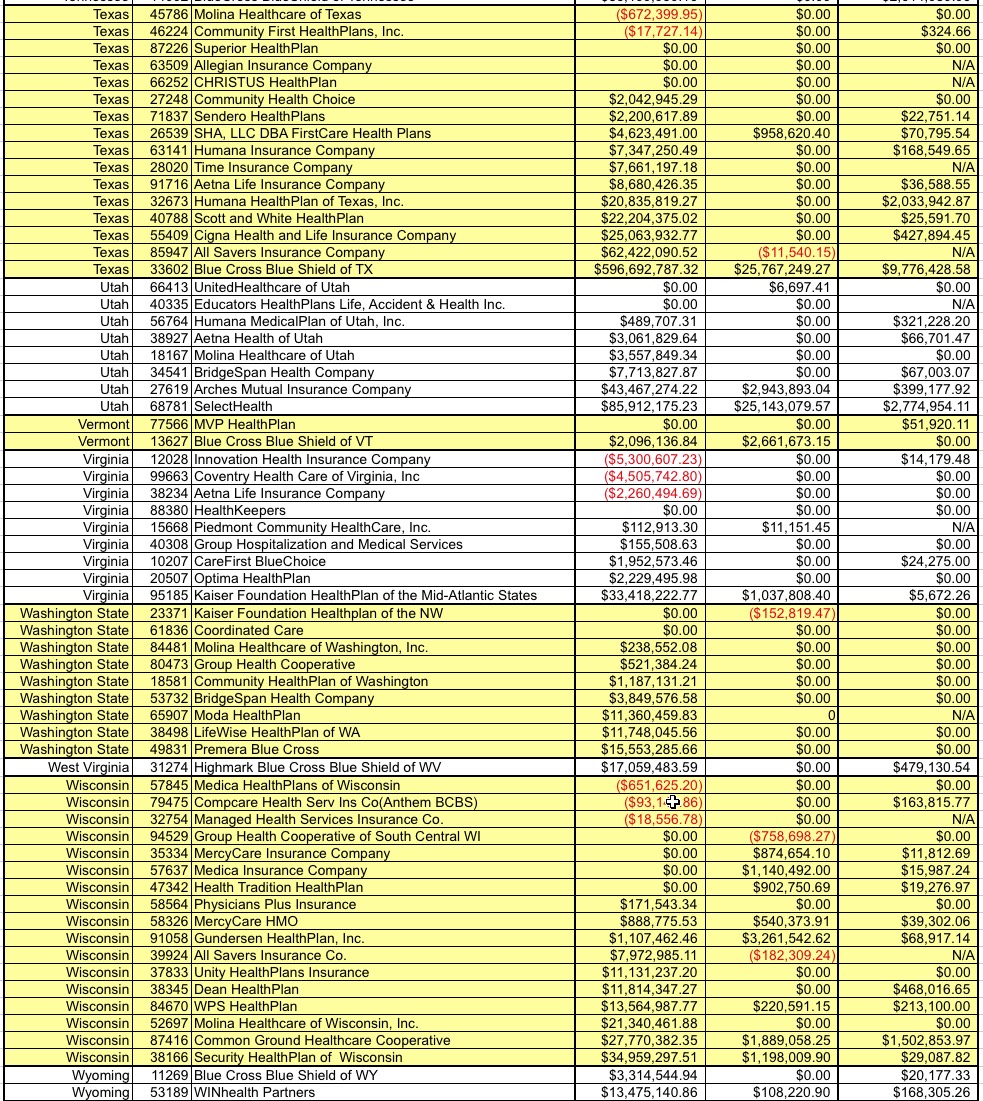

A table follows, listing every carrier across the country which owes money to or is owed money from the Risk Corridor program for 2015, as well as how much 2015 funding will be paid out to them to cover what's still owed for 2014. It's a long list, and some of the numbers are pretty big.

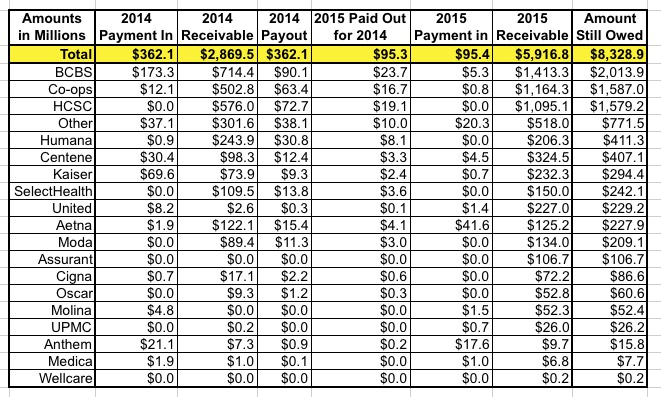

Unfortunately, it doesn't include a national total of any of the numbers involved, but someone took the time to add it all up for me; I'll verify these figures soon, but they seem reasonable to me:

Risk Corridors for 2015 are out!!

- $5.9 Billion owed back to insurers for 2015

- $95 Million payed back to insurers related to 2014

- $2.4 Billion still owed for 2014

- So far only 16.4% of 2014 payment will be made and 0% of 2015 payment.

- All numbers above are Individual + Small Group combined

They also provided the dollar amounts for select major carriers, along with the national tally, which I've compiled into a table below:

Of course it's theoretically possible that the 2016 numbers will end up saving the day...but given that several major carriers have bailed on the exchanges due to ongoing losses this year as well, that's pretty unlikely. So far a total of $458 million has come into the kitty while $8.79 billion in losses have been incurred. Unless the 2016 payments in end up being at least $8.3 billion more than whatever the 2016 receivables out are, the carriers are mostly gonna take a bath on the 3-year program...and even if they're paid in full, that's not gonna bring those liquidated Co-Ops back from the dead.

Of course, from a Republican POV, this is $8.3 billion which they've "saved" U.S. taxpayers...except that the real-world effect of "saving" that money...except that it did so by breaking a legal contract between the federal government and hundreds of private corporations, while helping wipe out over a dozen taxpayer-funded Co-Ops, the net effect of which, as I summarized back in February:

- up to 800,000 people nationally lost their insurance coverage, on very short notice, and were forced to scramble to find alternate coverage

- the new coverage these people ended up with is generally more expensive, and in many cases has worse networks

- the federal government has to therefore pay out more in premium subsidies to cover the increased costs as benchmark plans were increased

- over a dozen insurance carriers went out of business, meaning hundreds of people lost their jobs

- the loss of over a dozen carriers means less competition in those markets, therefore less competition, therefore higher premiums, therefore even more cost to the federal government in subsidies to make up the difference

- since all of the carriers which went out of business were little guys, this also means the big kahunas suck up even more market share

- the original $2.5 billion which Rubio was supposedly trying to "save" taxpayers ends up being paid out anyway; and

- it's possible that, in addition to all of this, assuming the government decides to just concede the point (which, by all rights, they should), it's conceivable that Marco Rubio's "genius" stunt from December 2014 could also very well end up costing taxpayers $2.5 billion MORE than it would have to just let the government make the payments they were supposed to in the first place.

- ...all so that Marco Rubio could earn a couple of political brownie points to help him win the GOP nomination for President...which he appears to be failing at anyway

I actually need to update this list a bit, however, as there have been several further developments:

- That 800,000 figure has actually risen to over 1 million, as several additional Co-Ops have gone belly-up since then, again, in large part due to the Risk Corridor Massacre;

- The 7th and 8th bullets (about the government having to pay out the funds anyway) doesn't appear to be playing out that way after all, since the lawsuits filed by various carriers to collect the funds owed to them seem to be getting shot down after all;

- Rubio, of course, did end up losing the GOP nomination anyway...but he did retain his seat as a U.S. Senator

- And, of course, with Donald Trump taking office as President and the GOP now holding control of all 3 branches of government, much of this is likely to be moot as the individual insurance market landscape, and the corresponding legalities surrounding it, may end up looking entirely different a year from now anyway.

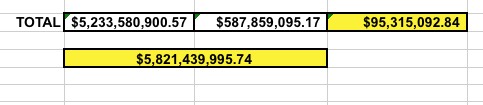

UPDATE: OK, I've compiled the entire list into a spreadsheet to tally up the total, and sure enough, my source had it right (be warned, this is a long list):

Advertisement