It's been a long, long time since I've written about the "Sub26ers"...that is, the population of Americans age 18 - 25 who are enrolled in the same healthcare policy as their parents thanks to the ACA's provision mandating that insurance carriers allow them to do so. While I may be missing a more recent article, the last time I recall writing anything in depth about this was nearly a decade ago:

Long-time readers will remember that throughout the 2014 Open Enrollment period, there was much fuss and bother made by both the Obama administration, the HHS Dept., myself and some ACA detractors over the "sub26er" population: Young adults aged from 19-25 years old who are covered by their parents policies thanks to provisions in the Affordable Care Act requiring all new policies issued since 2010 to allow this.

At the time I was a bit obsessed with trying to suss out just how many Americans fell into this particular category. It was a tricky number to pin down for a number of reasons, but in the end it seemed to hover somewhere in the 2 - 3 million range, depending on your source.

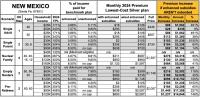

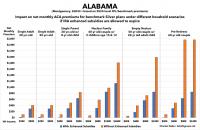

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

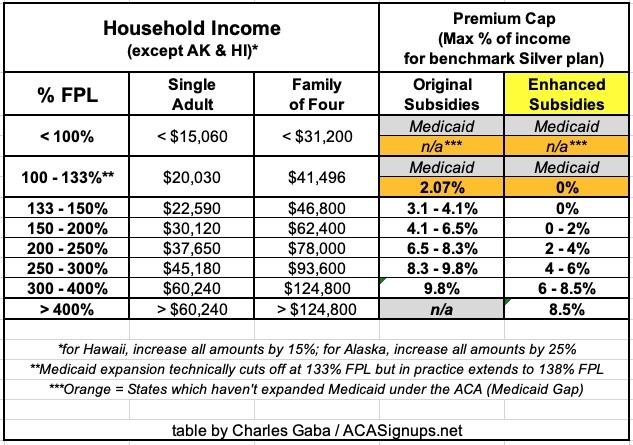

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

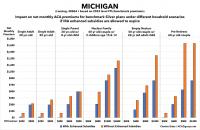

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

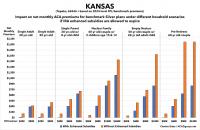

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

It's been another several months since the last time I wrote about the seemingly never-ending Braidwood v. Becerra lawsuit which threatens to not only end many of the ACA's zero-cost preventative services, but which could also throw all sorts of regulatory authority into turmoil depending on what precedents it sets.

On March 30, 2023, a federal district court judge issued a sweeping ruling, enjoining the government from enforcing Affordable Care Act (ACA) requirements that health plans cover and waive cost-sharing for high-value preventive services. This decision, which wipes out the guarantee of benefits that Americans have taken for granted for 13 years, now takes immediate effect.

In addition to beefing up the subsidies along the entire 100 - 400% Federal Poverty Level (FPL) income scale, the ARPA also eliminated the much-maligned "Subsidy Cliff" at 400% FPL, wherein a household earning even $1 more than that had all premium subsidies cut off immediately, requiring middle-class families to pay full price for individual market health insurance policies.

Here's what the original ACA premium subsidy formula looked like compared to the current, enhanced subsidy formula:

Covered California announced today that more than 158,000 Californians remained covered through the Medi-Cal to Covered California enrollment program over the past year.

Beginning in April 2023, following the end of the federal continuous coverage requirement put in place during the COVID-19 pandemic, Medi-Cal resumed its renewal process by redetermining eligibility for over 15 million of its members. In May 2023, Covered California and the Department of Health Care Services (DHCS), which administers California’s Medi-Cal program, launched the Medi-Cal to Covered California enrollment program.

Under the program, Covered California automatically enrolls individuals in one of its low-cost health plans when they lose Medi-Cal coverage and gain eligibility for financial help through Covered California. Through early June of 2024, the program has helped 158,100 Californians remain insured.