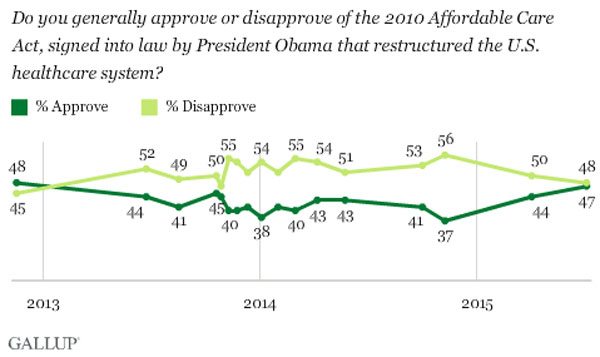

On top of this morning's excellent news from Gallup that the total number of uninsured U.S. adults dropped another 1.2 million people in the 2nd quarter of 2015 (0.5% of adults 18 & older = 0.5% out of appx. 245 million adults = around 1.2 million), the polling firm has released another data drop regarding approval/disapproval of the law, post-King v. Burwell:

On the surface, this isn't really that jaw-dropping; several other national polls have found similar trends, and the Kaiser Family Foundation's most recent survey actually has approval slightly outpacing disapproval. Still, it's always good to see confirmation from another respected source.

In addition, while the Kaiser survey included a fairly large "Don't know/Refused to answer" contingent, Gallup seems to be more forceful about getting leaners to commit: The latest survey only has 5% unlisted.

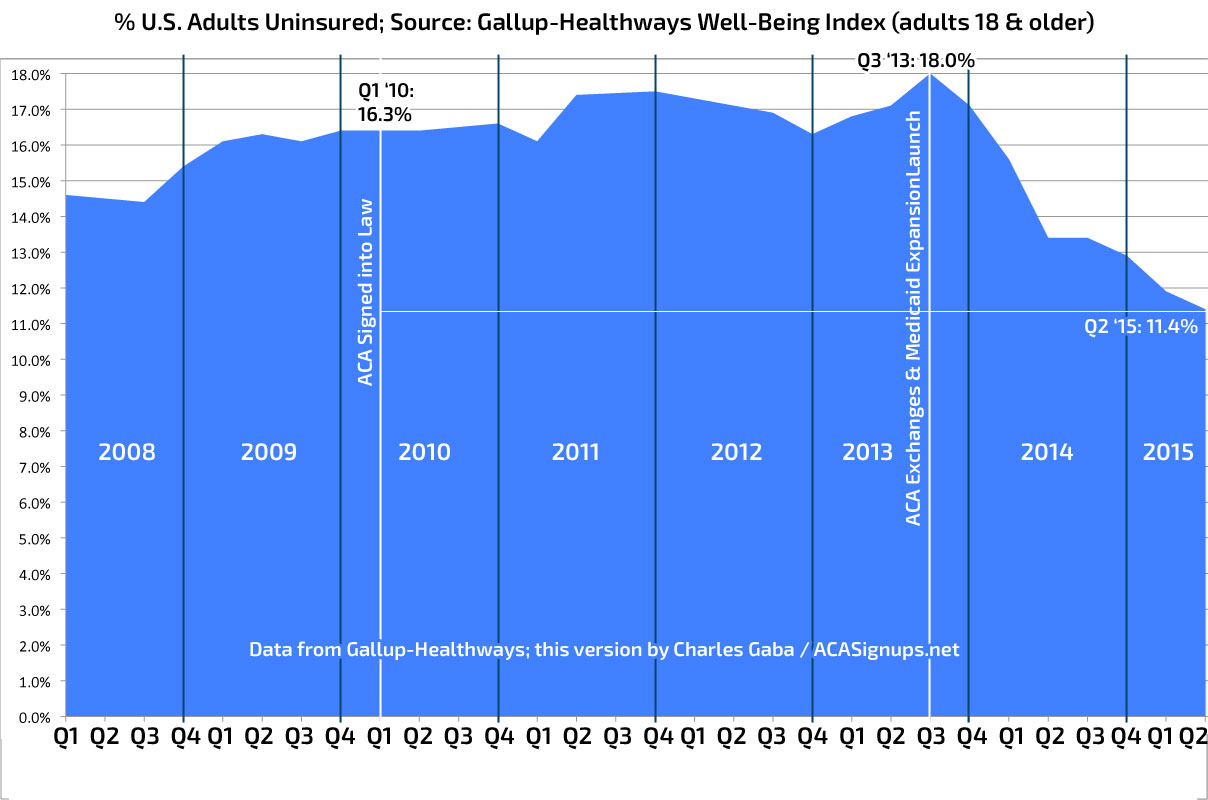

Furthermore, anyone who enrolled/enrolls between around February 23rd and March 15th (varies by state) will start coverage on April 1st...and then, on May 1st, the bulk of the #ACATaxTime Special Enrollment Period enrollees will be kicking into gear. Don't forget off-exchange enrollees, ongoing Medicaid expansion, etc...I wouldn't be at all surprised to see the national uninsured rate drop to below 12% by April.

The uninsured rate among U.S. adults declined to 11.9% for the first quarter of 2015 -- down one percentage point from the previous quarter and 5.2 points since the end of 2013, just before the Affordable Care Act went into effect. The uninsured rate is the lowest since Gallup and Healthways began tracking it in 2008.

Yesterday I noted that if the Republican Party really wants to damage the Affordable Care Act, they could do so quite easily...byhelping the Affordable Care Act:

Put another way: 11.7 million people selected QHPs during 2015 open enrollment, of which roughly 10.3 million are currently enrolled nationally. If every state had expanded Medicaid as of the beginning of this year, only around 9.5 million people would have selected QHPs and only around 8.4 million would still be enrolled in them today.

That's right: As Sprung put it last March, by refusing Medicaid expansion, red state governors and legislatures drove almost 2 million private plan enrollees to federal exchange.

UPDATE 7/13/15: OK, looks like they've posted a "teaser" of the interview this morning; it's set to air this evening at 6pm; as you can see, in the text version, at least, they did a good job of including several of the key points I brought up, especially the "shop around" factor:

This led to a bit of confusion about just who does and doesn't fall into the "Medicaid Gap"...that is, people who don't qualify for Medicaid, but also don't make enough money to qualify for federal tax credits to enroll in private policies via the ACA.

As I noted yesterday:

...in states which expanded Medicaid, households earning less than 138% of the Federal Poverty Level (FPL) are eligible for Medicaid; anyone from 138% - 400% are eligible for federal tax credits to enroll in private Qualified Health Plans (QHPs) via the ACA exchanges.

Remember that massive Excel HC.gov enrollment spreadsheet file released last week? The one which broke out 2015 QHP selections by county, age group, metal level, income range and so on? Well, for those who don't have Excel, they've set up a web-based version of each.

OK, this is rather embarrassing (from the Office of the Inspector General):

CMS's internal controls did not effectively ensure the accuracy of nearly $2.8 billion in aggregate financial assistance payments made to insurance companies under the Affordable Care Act during the first 4 months that these payments were made.

Last week another healthcare reporter and I (I think I do count as a "reporter" by now, yes?) were discussing the fact that some of the 10.3 million people currently enrolled in private policies via the ACA exchanges would be eligible for Medicaid instead, if their states would simply expand Medicaid via the ACA.

How is this? Well, in states which expanded Medicaid, households earning less than 138% of the Federal Poverty Level (FPL) are eligible for Medicaid; anyone from 138% - 400% are eligible for federal tax credits to enroll in private Qualified Health Plans (QHPs) via the ACA exchanges.

However, in states which didn't expand Medicaid, households earning 100% - 400% are eligible for those private QHP tax credits (anyone below 100% are flat-out screwed if they don't already qualify for "normal" Medicaid in their state).

In nearly every state, the official "enrollment number" used in the HHS Dept's ASPE reports has been the number of QHP selections completed...whether or not the enrollee actually pays their first monthly premium. Naturally, this led to a lot of fuss and bother about "How many have PAID???" last year (and this year as well, though to a lesser extent). In the end, the answer in 2014 turned out to be roughly 88%, with an additional 4% or so gradually dropping their policies over the course of the year and another 5% dropping theirs once the 2015 season opened up. In 2015, so far it looks like the 1st-month-paid percent is a bit higher, more like 90%.

Most news outlets mushed the two figures (non-payments and attrition) together, but I keep them separate, and Washington State is one reason why. Unlike most states, the Washington ACA exchange only reports their exchange policies after the first monthly premium has been paid. As a result, while their official numbers seemed a bit weak back in February (160,732 vs. their stated goal of 230,000), the silver lining is that it was also a "cleaner" figure; I didn't have to lop off 10% of the total, since WA "pre-purged" it for me.

Spotlight here is on Alabama in my continuing close look at how many low income ACA private plan buyers accessed Cost Sharing Reduction (CSR) subsidies by buying silver plans. (Yesterday, HHS released detailed county-level data about buyers of private plans on healthcare.gov, the federal exchange, enabling a close look at state stats.)

CSR is available to buyers with household incomes below 251% of the Federal Poverty Level (FPL), and strongest for buyers under 201% FPL. It is available only with silver plans, the second-cheapest of four metal levels available on ACA exchanges -- a fact that's less than obvious to the average shopper, Buyers under 201% FPL are leaving a really strong benefit on the table if they don't buy silver plans (see the note at bottom for more detail). I consider the percentage of buyers under 201% FPL who select silver an important measure of how well the exchange is functioning in a given state. (Those in the 201-250% FPL range are likelier to have good cause to forego the relatively negligible CSR provided at that level.)

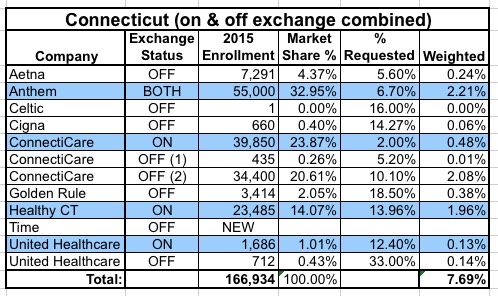

Nearly 2 months ago, I posted about Connecticut's insurance policy rate change requests from the 9 companies which plan on offering individual healthcare policies either on or off the ACA exchange, Access Health CT. The takeaway at the time was that, when weighted for the relative market share of each company, it looked like a statewide average requested rate increase of 7.7%, which isn't bad at all given the massive hikes being tossed around in some other states:

None of these have actually been approved yet, mind you...and in fact, just today it was announced that the CT Insurance Dept. will be holding public hearings to discuss the rate requests by three of the companies above: Anthem, ConnectiCare and Golden Rule.

Even before that happens, however, there's been some shifting: The first two companies, Anthem and ConnectiCare, have put in revisions to their earlier requests: