California: Effectuated ACA enrollment down 5.6% y/y; could drop by 12% or more by end of 2026

Fri, 04/17/2026 - 2:57pm

Covered California, the state's ACA exchange, has published effectuated enrollment data for January & February 2026, so it's time to dig in and see what this might say about national trends.

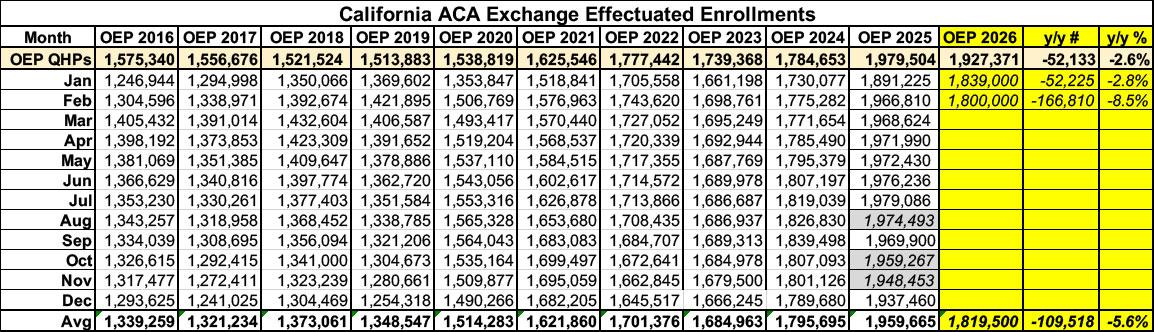

Officially, Qualified Health Plan (QHP) selections during Open Enrollment were only 2.6% lower than they were in 2025. However, as I expected and have warned about repeatedly, the year over year drop in effectuated enrollment was higher than that in January (down to 1,839,000, a 2.8% drop y/y), and the gap more than tripled in February:

- February 2026 enrollment is currently estimated at 1.80 million enrollees, a decrease of 135,000 (7 percent) from the 1.94 million enrolled in February 2025.*

(Note: CMS's official Public Use File actually puts February 2025 effectuated enrollment about 27,000 higher, or 1,966,810, for a February to February drop of 8.5%.)

- Before 2026, Covered California always increased net membership between October and February, averaging 60,000 enrollees from 2021 to 2025.

- In 2026, the marketplace shrank by over 150,000 enrollees between October and February, from a record-high 1.96 million in October 2025 down to 1.80 million in February 2026.

- Had Covered California maintained typical open enrollment experience for 2026, enrollment in February might be 210,000 higher than it is today.

For January & February combined, average effectuated enrollment in CA is down around 110,000 enrollees or 5.6% so far.

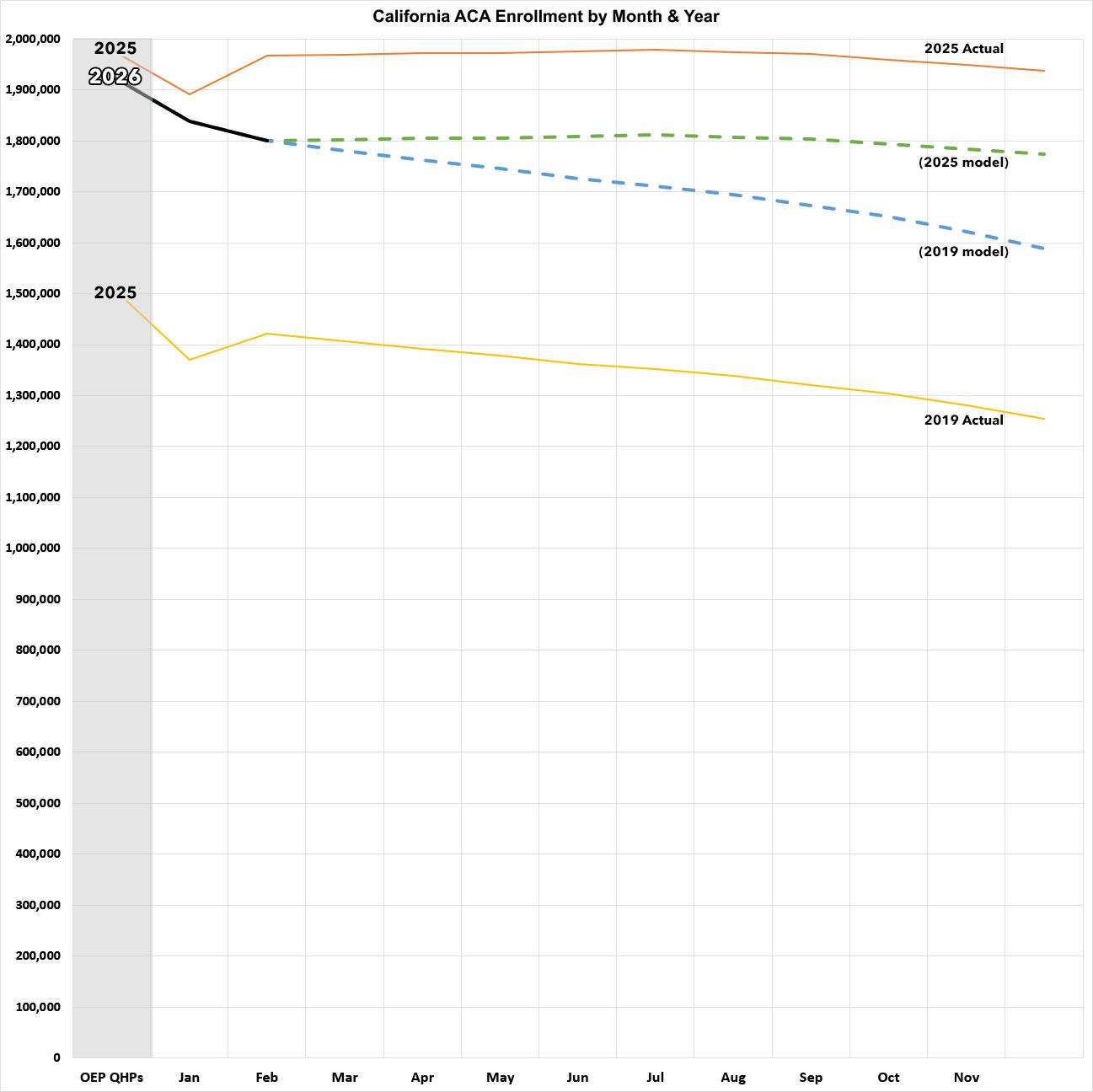

What might this look like for the rest of the year? Well, here's a visual version of the graph above, with the dotted lines respresenting what the rest of 2026 will look like if the effectuation pattern for the balance of the year follows either last year (2025) or the last pre-COVID year (2019):

- If the rest of the year follows the 2025 pattern, effectuations will taper off slightly more to around 1.77 million by December and will average around 1.8 million for the year...down 8% compared to 2025. However, it's likely to be considerably worse than that.

- If the rest of the year follows the 2019 pattern, effectuations will be down to around 1.59 million by December, and the average for the year will be around 1.72 million...down 12.4% y/y.

As I've mentioned before, it's important to keep in mind that under the ACA, insurance carriers are required to provide a 90-day grace period for enrollees to pay past-due premiums. This means that enrollees whose 2026 policies went into effect on January 1st had until the last day of March to make their first premium payment...which, in turn, means that there will likely be a significant drop in effectuated enrollment which won't actually show up until data for April is published...which likely won't happen until sometime in July for most states...although California and some other state-based exchanges will publish it sooner than that.

In addtion, it's also important to keep in mind that California is one of the dozen or so states which have implemented either state-based subsidies or other specific policy measures to help mitigate the damage caused by the enhanced federal tax credits expiring back in December.

In California's case, they're fully backfilling the lost federal tax credits to all enrollees who earn up to 150% of the Federal Poverty Level (FPL). In California's case, that's around 294,000 people, or roughly 15% of total enrollees this year.

Both of these points are addressed in the Covered CA Executive Director report:

- During the renewal process for plan year 2026, Covered California enrollees faced an unprecedented increase in costs due to the expiration of the enhanced Premium Tax Credit that had lowered costs for all enrollees since plan year 2021.

- • Previous Open Enrollment and Renewal reporting focused on the count of individuals who were still enrolled or pending enrollment for a health plan at the close of the Open Enrollment Period (January 31st).

- • However, with 90-day grace periods to make premium payments, consumers may not be cancelled for non-payment until early April.

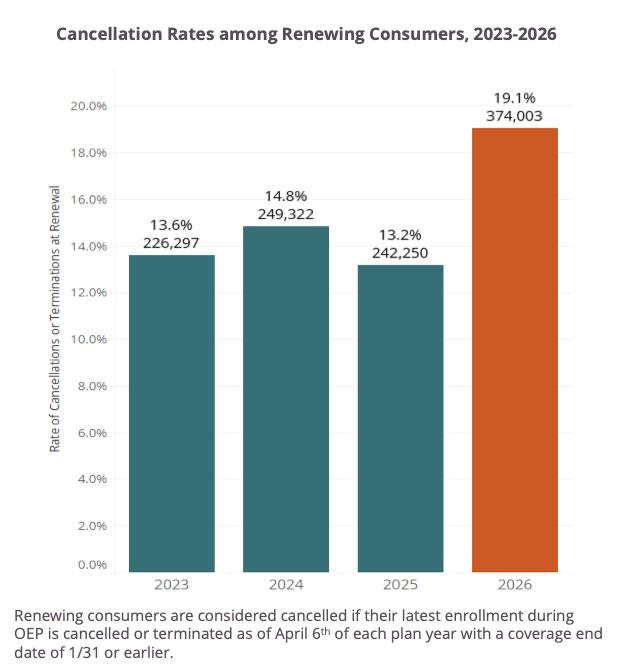

- By the end of payment grace periods, nearly 374,000 renewing consumers had cancelled or terminated their renewal plan.

- This represents 19% of renewing consumers, compared to 13% to 14% of renewing consumers cancelling their coverage in prior years.

- In the renewal cycle for 2026, this increase equates to over 130,000 additional enrollees cancelling or terminating their renewal.

It's important to note that even though 374,000 enrollees terminated their coverage thru April 6th, that doesn't mean that the net effectuated enrollment has dropped by that much--remember that California is one of several states which still kept Open Enrollment running through the end of January, which means most of those who selected a plan in January (or in February or March, via Special Enrollment Periods) won't be reflected in this figure.

Right now I'm guessing that the net drop thru April is likely something like ~360,000 or so, which would equate to roughly an 11% average drop for the first four months of the year, but I'll wait until the actual March & April data are published before being sure of that.

What this does mean is that California's effectuated enrollment is already down somewhere between 110,000 - 374,000 (between 5.6 - 12.4%), and is unlikely to increase between now and December.

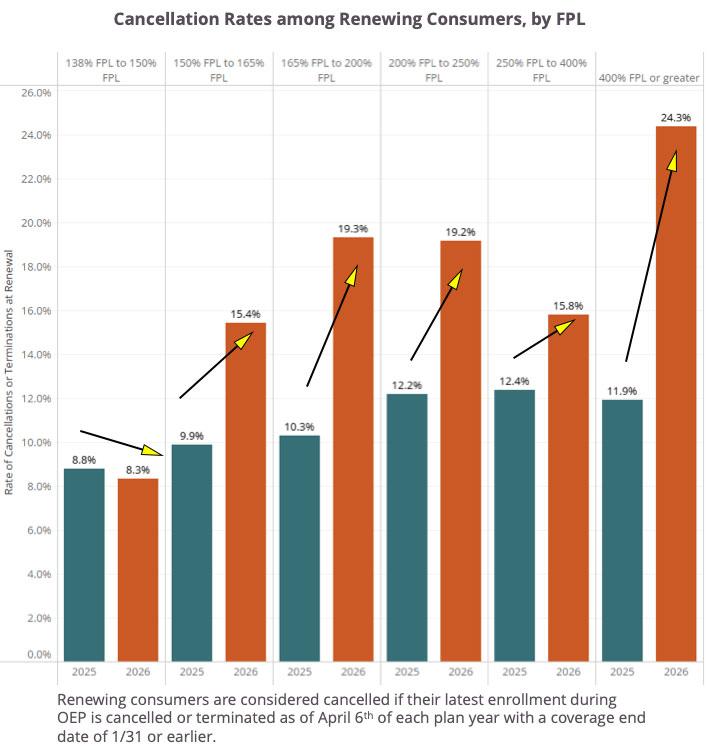

- For middle income consumers who lost all eligibility for tax credits in 2026, cancellation rates more than doubled, rising to 24.3% in 2026 from 11.9% in 2025.

- For the lowest-income consumers – who retained affordability similar to 2025 thanks to state premium subsidies – cancellation rates fell from 8.8% to 8.3%.

- Focusing on consumers with incomes between 150% FPL and 400% FPL, who retained eligibility for APTC but still experienced substantial premium increases, there are significant disparities in renewal cancellation rates.

- Consumers who identify as Black or African American saw cancellation rates nearly double (29.4% in 2026 vs 16% in 2025).

- For the consumers with state subsidies that preserved ePTC affordability (between 138% FPL and 150% FPL), no such differences in cancellation rates were observed by race/ethnicity.

My guess is that the effectuated enrollment drop will be even higher in states which don't have state subsidies, Premium Alignment pricing or other such policies in place.

Advertisement