Massachusetts has one of the stablest statewide insurance markets, no doubt in large part due to their having instituted the precursor to the ACA, "RomneyCare", 4 years earlier. Massachusetts also merged their small business and individual market risk pools, which helps stabilize things. As a result, they have a high number of carriers participating in their ACA exchange and are among the few states with single-digit average rate hikes...assuming CSR payments are forthcoming and the individual mandate is properly enforced.

Assuming CSR payments aren't made, I used the Kaiser Family Foundation's 19% average estimate for Silver plan hikes due to the CSR factor. Since a whopping 92% of MA's exchange enrollees chose Silver plans (it looks like MA's unique "ConnectorCare" plans are considered Silver as well), that means an average CSR factor of around 17.5 points across the entire individual market.

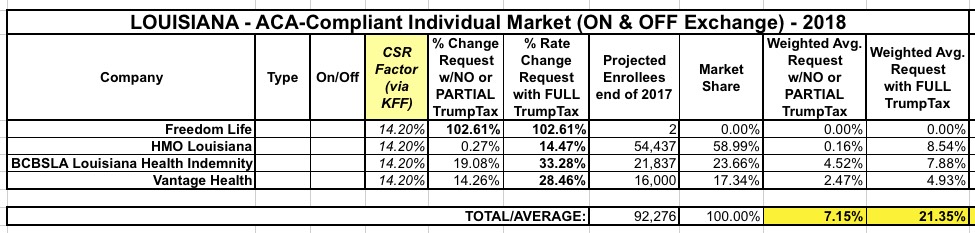

Louisiana has 3 individual market carriers for 2018 (technically there's 4, but "Freedom Life" is basically just a shell company with a placeholder filing). Officially, they're requesting average rate increases averaging around 21.4%...but all three carriers state point-blank in their filing letters that a huge chunk of their request is due specifically to the CSR reimbursement and mandate enforcement issues. The Kaiser Family Foundation estimates the CSR issue alone adds around 20 points to Silver plans, and 71% of Louisiana exchange enrollees chose Silver, so that translatest into roughly 14.2 points across the whole market. This results in just a 7.2% average rate hike if CSR payments are made vs. 21.4% if they aren't:

Hawaii only has two carriers on the individual market (and in fact doesn't even have much of an individual market due to a state law mandating that nearly every business provide coverage anyway). HMSA's filing letter is very specific about calling out both the CSR and mandate enforcement sabotage factors as being part of their request. Kaiser doesn't really mention either issue at all, and the only CSR reference in the filing seemed to assume it would be paid, so I have one in each category. Kaiser Family Foundation assumes a 21% Silver CSR rate hike, and 71% of Hawaii's exchange enrollees are on Silver plans, so that amounts to roughly a 15% overall CSR factor.

Here's what it looks like...15.2% w/partial sabotage, 30.2% with full sabotage:

48 hours ago I posted this analysis/explainer of the "Silver Switcharoo", the goofy, bass-ackwards workaround which insurance carriers and state regulators could (if necessary) use to resolve Donald Trump's impending threat to pull the plug on Cost Sharing Reduction subsidy reimbursement payments.

There's been a whole bunch of additional CSR-related developments since then:

Congressional Republicans moved on Tuesday to defuse President Trump’s threat to cut off critical payments to health insurance companies, maneuvering around the president toward bipartisan legislation to shore up insurance markets under the Affordable Care Act.

Insurance Commissioner Announces Single-Digit Aggregate 2018 Individual and Small Group Market Rate Requests, Confirming Move Toward Stability Unless Congress or the Trump Administration Act to Disrupt Individual Market

For 2017, North Carolina's unsubsidized, weighted average individual market rate hikes came in at around 24.2%. With carriers like Aetna, United Healthcare, Humana and Celtic all dropping out of the NC exchange market, there wasn't much math to do in order to find a weighted average: The only individual market carriers left were Blue Cross Blue Shield of NC, Cigna and "National Foundation Life Insurance", which is basically a non-entity shell company related to "Freedom Life", the less said about the better. Since Cigna only had around 1,200 indy market enrollees at the time (less than 0.5% of the total market share), that pretty much left BCBSNC as the only game in town, so their 24.3% hike was the whole shebang for the state.

About 5 weeks ago I noted that organizations representing pretty much the entire healthcare industry sent urgent letters to Donald Trump, HHS Secretary Tom Price, Treasury Secretary Steven Mnuchin, OMB Director Mick Mulveney and current CMS Administrator Seema Verma...basically, every major healthcare-related administration figure...practically begging them to fund the goddamned Cost Sharing Reduction reimbursements.

They made it crystal clear how vitally important doing this was, and Trump grudgingly went ahead and made the April payment, then later indicated that he was "probably" going to keep reimbursing carriers for the CSR funds legally owed to them on an ongoing basis, at least until the House vs. Price (formerly House vs. Burwell) lawsuit appeal process was completed.