The Rebooted #OE2 Spreadsheet & my State-level Projections

Fri, 11/14/2014 - 11:09pm

I was cleaning up The Spreadsheet earlier this evening to prep it for the 2015 Open Enrollment Period. Most of the changes involve simply stripping out the OE1 numbers so I can start all over again, but there's some other changes which true data geeks will notice, including:

- I've decided to completely delete the "Sub-26er" column, not because they don't exist (there should still be 1-2 million out there), but because they've basically been absorbed into the other QHP numbers at this point (and were extremely tricky to accurately count in the first place).

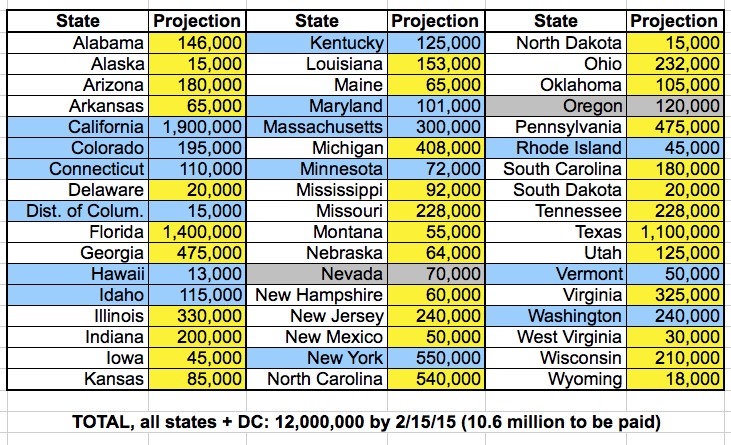

- The Idaho row is now blue since they've broken off from HC.gov onto their own full state-run exchange.

- Conversely, both Nevada and Oregon have been changed to gray because they're operating on HC.gov this year...but are still technically classified as state-run (Oregon's SHOP exchange is still apparently being run locally, however).

- Speaking of the SHOP (small business) exchanges, last year most of them were blacked out since only a handful were operational (with perhaps 80,000 individuals being covered by SHOP policies nationwide). This year, all 51 will supposedly be operational...with one exception (Vermont...see below).

- Also on the subject of the SHOP exchanges, note that in addition to Oregon, several other states are marked in blue as well even though their individual/family exchange is being run through HC.gov: Mississippi, New Mexico and Utah. Jazzing things up even more, Idaho is doing the opposite: Individuals/families enroll via Your Health Idaho, but SHOP enrollees are still taken to HC.gov.

- Note that DC and Vermont have their off-exchange cells blacked out, just as they did last year. This is because in this state & district, all individual insurance has to be purchased through the exchanges by law. DC did this in order to make sure that they had a large enough pool to operate their exchange. Vermont did so for the same reason, but also because they're gradually moving towards single payer, and this presumably was one of the phases in that plan. Unfortunately, VT's SHOP exchange was (and still is) so screwed up, the Governor had to issue a special executive order allowing small businesses to purchase policies off of the exchange after all. Confused yet?

- PAID QHPs: I've successfully proven, repeatedly, that in the end, around 88% of all exchange QHP enrollees (on average) do eventually pay at least their first month's premium. Therefore, this time around I'm just plugging in 88% until I receive reliable evidence to the contrary. Keep in mind that this a rolling average--anyone who enrolls between tomorrow and 12/15 will have until the end of December to pay for January 1st coverage, so don't freak out if a report comes in on 12/10/14 claiming that "only 67% have paid!" or whatever.

- I've also eliminated the "1YX" column, which I used to designate states which were allowing 1 year extensions of non-compliant policies. Not only is this moot for those states, but some others are allowing 2 or even 3 year extensions (and I'm not sure which); in the end this doesn't really matter that much anymore.

- The total state population column has been updated. Unfortunately, I don't have updated "QHP Eligible" numbers for the 2nd column from the left. That's OK, though, since a good half or more of this year's QHPs will be those already on the exchanges anyway.

- And FINALLY, take a look at the yellow columns (3rd/4th ones over). These are my own state-level projections, which add up to the 12.0 million that I'm projecting nationally.

For the most part, these are straight-line 50%-increase projections over last April's total for each state (or close to it), just as the 12.0 million is a straight 50% bump over the 8.02 million total. However, there's a few states which are noteworthy:

- California had 1.4 million enrollees as of April. A straight 50% bump would put them at 2.1 million. However, they also ended up with a lower than average payment rate this year (82%) and their own projection only puts them at 1.73 million for 2015, so I'm splitting the difference and assuming 1.9 million for CA.

- Florida, meanwhile, gave an "official" projection of only 1.07 million, but I have a gut feeling that they're gonna outperform substantially this time around, so I have them at 1.4 million, which would effectively make up for CA coming up short.

- Massachusetts: This is a very special case. As I've noted a couple of times, due to MA's first attempt at an ACA exchange failing so miserably, they had to push a whopping 300,000 Bay Staters into some sort of temporary health insurance limbo status. These are people who presumably can afford private policies, but their income status couldn't be proven. Since the state couldn't be sure who was supposed to receive tax credits and who wasn't, they basically punted until 2015. Supposedly MA's all-new exchange should work properly; if it does, Massachusetts could see a dramatic 13-fold increase in QHP enrollments by the end of February.

- Finally, there's Vermont, whose ACA exchange website is still completely offline even as I type this, just 1 hour before #OE2 starts (OK, presumably it wouldn't be open for business until tomorrow morning anyway, but still...)

So, there you have it. I realize that it's pretty much insane for me to try and drill down to that level of detail, but what the hell. My official state-level exchange QHP projections for the 2015 Open Enrollment Period are:

UPDATE: As I noted on December 11th, I've since bumped up my total projections a bit to 12.5 million. As such, the state-level projections are also obviously a bit higher now.

Instead of whipping up a new graphic, just visit The Spreadsheet to see the revised state-level projections and how close each state is doing so far (remember, the autorenewals for most states haven't been broken out yet, so just focus on the state-exchange lines along with Oregon and Nevada for now).

Advertisement