Several of the states operating their own ACA exchanges have already had their 2018 Window Shopping tools up and running for several weeks now, including Covered California, Your Health Idaho and the Maryland Health Connection, so this really shouldn't be that big of a deal, but given the insanity and uncertainty surrounding this years' Open Enrollment Period and especially the fact that HealthCare.Gov is responsible for 39 states (while being operated by the federal government under the thumb of an openly-hostile Trump Administration), it's pretty important news regardless.

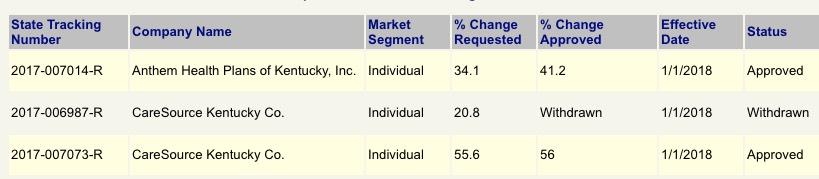

When I ran the requested rate hike numbers for Kentucky in early August, it looked like the only 2 carriers participating in the individual market next year (CareSource and Anthem BCBS) were asking for pretty hefty hikes of around 30.8% on average...and that assumed CSR reimbursement payments would be made next year. If they aren't, based on the Kaiser Family Foundation's estimates, I tacked on an additional 13.8% for a requested average of 44.3%. Ouch.

Washington, D.C. – The District of Columbia Department of Insurance, Securities and Banking (DISB) approved health insurance plan rates for the District of Columbia’s health insurance marketplace, DC Health Link, for plan year 2018.

Insurers filed their initial rates with the Department in May. Since then, DISB engaged in its rate review process resulting in two out of the four insurers revising their rates down from their initial filings, one as much as half of what was proposed. The Department also held a public hearing during the rate review process to allow residents to provide input in the rate review process.

Back in August, I posted a rough analysis of the requested rate increase situation for Wisconsin's individual market carriers. However, I cautioned at the time that I was missing the enrollment market share numbers for four of the carriers (Aspirus, Compcare, Wisconsin Physician Service and WPS), and therefore had to guess at how the rate hikes for those carriers would impact the statewide average. I estimated the numbers assuming CSR payments are made at 21.7%, and from that assumed the impact of CSR reimbursements not being made would be around 7.8 additional points being tacked onto the average.

A couple of weeks ago, the state insurance commissioner announced the approved rate increases. The good news is that I overestimated on the "CSRs paid" front. The bad news is that I underestimated on the "CSRs not paid" front: It's actually 20% and 36% respectively:

On November 10, 2016, at 4:30 in the morning, I was still in a bit of a dazed state trying to absorb the reality that a racist, misogynistic, xenophobic con-artist sexual predator moron was about to become the next President of the United States. We were 9 days into the 2017 Open Enrollment Period, and I realized that there was absolutely no way of knowing what sort of impact the election results might end up having on how many people would sign up for coverage.

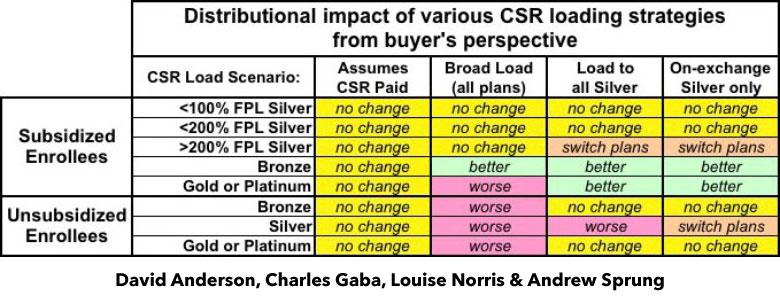

I've written a lot in recent weeks about the real world impact that Trump cutting off CSR reimbursement payments will have on 2018 premiums in various states depending on how they choose to load the additional cost. As I've noted repeatedly, there are basically four strategies they can take: They can assume the payments will continue; they can spread the load across all ACA-compliant policies; they can load all of the cost onto Silver plans only; or they can load all of the cost onto on-exchange Silver plans only, while also creating (if one doesn't exist) a special off-exchange-only Silver plan as a backstop for unsubsidized Silver enrollees (aka the "Silver Switcharoo").

Up until a week ago, the possibility of Donald Trump pulling the plug on Cost Sharing Reduction reimbursement payments was a looming threat every day. While it hadn't actually happened yet, most of the state insurance commissioners and/or insurance carriers themselves saw the potential writing on the wall and priced their 2018 premiums accordingly (or at the very least prepared two different sets of rate filings to cover either contingency).

A few spread the extra CSR load across all policies, both on and off the exchange. This seems like the "fairest" way of handling things on the surface, but is actually the worst way to do so, because it hurts all unsubsidized enrollees no matter what they choose for 2018 and can even make things slightly worse for some subsidized enrollees in Gold or Platinum plans.

Our timing couldn't have been more fortuitous: Less than 48 hours after we posted the piece, Donald Trump announced that, sure enough, he's finally following through on his threat to pull the plug on CSR payments, effective immediately.

The approved rate increases for NJ were just released, and the numbers appear to be pretty close to that, if a bit higher: 9.9% and 22.0% respectively.

Truth be told, I only have the hard numbers for the exchange-based carriers...and even those aren't technically official; they come from this NJ.com article:

TRENTON -- New Jersey residents who bought their own health coverage from Horizon Blue Cross Blue Shield through the Affordable Care Act could pay an average of 24 percent more next year, according to state-approved rates released on Tuesday.

Horizon is one of three insurance companies in New Jersey participating in the Obamacare marketplace in 2018. But it is the most dominant, insuring 72 percent of the 244,000 individual policy holders this year.

I first looked at Rhode Island's proposed rate hikes back in early July. At the time, the average increase for the two carriers participating in RI's individual market was 10.5% assuming CSR reimbursement payments are guaranteed for 2018. If they weren't guaranteed, however, I estimated at the time that an additional 19 percentage points would be added into the mix, based on an estimate by the Kaiser Family Foundation.

However, I realized a little later on that I was misinterpreting KFF's analysis; they were referring to how much they estimated silver plans would go up due to the lost CSR funds, not all metal levels. Furthermore, for Medicaid expansion states (which includes Rhode Island) they estimated the average was only 15%.. Based on these factors, the impact across the board on Rhode Island should have only been around 10.3%.