It appears that after the tragic Amtrak derailment a couple of weeks ago, a Philadelphia-based personal injury attorney named Chad Boonswang (allegedly) decided to send out hand-written "sympathy cards" to the families of not just one, but at least two different victims. The "sympathy cards" actually contain no words of sympathy, but instead are crass ads pushing his litigation services at a discounted rate. What a bargain!!

Adding insult to injury, at least one of the victims and their families happen to be Jewish, making the embossed cross on the outside of the card doubly tacky.

In other words, every one of the following states--along with the other 2 dozen not already running their own exchanges--should be running, not walking towards at least getting their ducks in a row in case SCOTUS lowers the boom...and instead, every damned one of them appears to have decided to twiddle their thumbs for the next 6 months or so.

Anyway, let's suppose that #1 and #2 are squared away. Against all odds, the Republican governors and legislators of these states get their heads out of their asses and actually approve all of the above.

That leaves #3: Time. Even if everything was streamlined and fast-tracked (and lord knows that's unlikely), it would still take substantial amounts of time to do all of this.

5. Does the rate change reflect how many people switched policies and/or companies?

Number 4 is easy: NO. None of the requested rate changes that you're seeing flying around right now (and will continue to for the next few weeks) have been approved yet. This could dramatically change some of the final rates.

As I’ve noted before, Republicans may try to pass a temporary patch for the subsidies, packaged with something like the repeal of the individual mandate, in hopes of drawing a presidential veto — so Republicans can then try to blame Obama for failing to fix the problem.

A few days ago, in my latest exclusive for healthinsurance.org, I listed 4 important questions to ask before freaking out about the Scary Rate Increase Headlines® which have started popping up in the news for some states. However, I forgot about a fifth one, which I hinted at yesterday in my analysis of the new Kaiser Family Foundation survey:

Bear in mind that "shopping around" doesn't necessarily mean that you switch policies, it just means that you at least looked around to see what was available.

The whole theory behind the "invisible hand of the free market = lower prices for all" mindset is that competition allows the consumer to shop around and compare pricing and other factors. However, the "competition = lower prices" theory only works if the customers actually do shop around. This year only 30% did, which is either unimpressive or impressive depending on your perspective.

Jeffrey Toobin is a very smart man. He's a staff writer at The New Yorker and has been CNN's legal analyst for many years.

That doesn't mean he's correct about everything, however...and in fact, he made a very obvious, very significant factual error in his King v. Burwell opinion piece this morning, "Obama's Game of Chicken with the Supreme Court".

The main thrust of the piece is that if the Supreme Court does rule in favor of the plaintiffs in King v. Burwell and does make the IRS stop issuing federal tax credits to millions of people enrolled in private healthcare policies via the federal exchange, most people will blame President Obama and the Democratic Party for the fallout rather than the Republicans in Congress and their conservative think tank allies who brought the lawsuit, financed the lawsuit, cheered on the lawsuit and, most importantly, are refusing to take 5 minutes out of their day to "fix" the supposed "problem" in the language of the law.

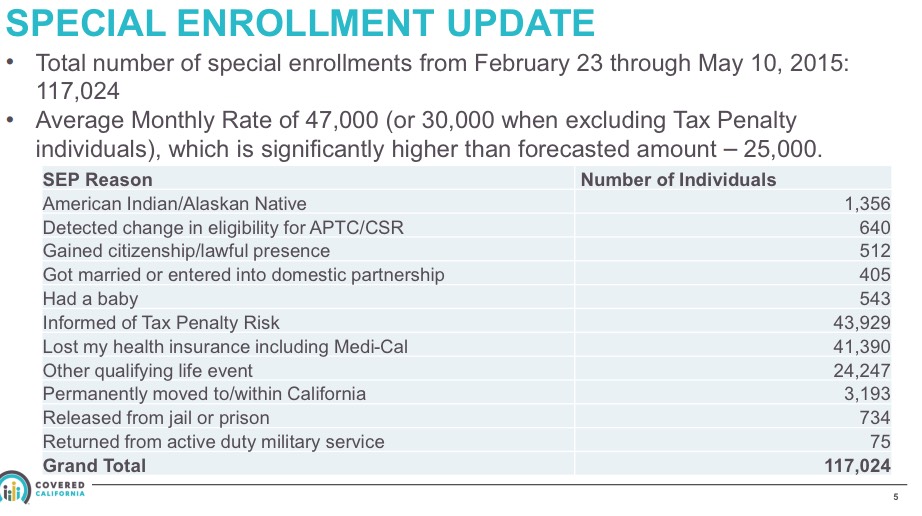

According to the new report, they've had a total of 117,024 QHP selections since then (through May 10th), including #ACATaxTime enrollments:

Add them together and you get 1,529,224 total QHP selections to date (well, as of 5/10, anyway).

One interesting side note: CA's final #ACATaxTime tally turned out to be nearly 10,000 higher than expected (they previously reported around 33K with just a couple of days to go in the special enrollment period; apparently a lot of people jumped in at the last second after all)

On the surface, aside from the extra 10K for #ACATaxTime, that doesn't sound too interesting...I already had CA down with 1,503,200 QHPs, so this is just 26,024 higher. Big deal, right?

Except for one thing: I've confirmed that the number below represents actual paid, effectuated enrollments as of March 2015:

Holy smokes. The Kaiser Family Foundation, without which running this site would be much harder, has released their 2nd annual (I assume it'll be done every year) Survey of Non-Group Health Insurance Enrollees.

There's a heck of a lot of findings to absorb here, almost all of which overlaps with the areas I cover here at ACASignups.net, so it'll take some time to go over it all. However, here's my initial thoughts:

The survey, conducted February 18 – April 5, 2015, after the close of the second open enrollment period, includes individuals who purchased ACA-compliant coverage inside or outside of a Marketplace, as well as those who are currently enrolled in “non-ACA compliant” plans.

These are really important points to keep in mind when looking at their findings. It does include off-exchange enrollments, whether ACA-compliant or not (and in fact those distinctions are the focus of some of KFF's findings).

Throughout the long, tortured life of the Affordable Care Act over the past 5+ years, one of the easiest attack points has been to go after the sheer bulk and complexity of the law itself. Whether you're referring to the actual wording of the law (supposedly a whopping 2,700 pages long) or, even worse, the 8-foot tall stack of 10,000 - 20,000 pages of regulations related to "Obamacare", Republican politicians, pundits and talk show hosts have used the immense size of the ACA itself to go after it.

I'm bringing this up now because my big project the past week or two has been to track down the various 2016 policy premium rate change requests for the companies operating both on and off the ACA exchanges in all 50 states (+DC, of course).

So far I've done a pretty good job with OR, WA, CT, MI, DC and VT...and I have partial data for MD & IA.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}