Rhode Island: HealthSource RI releases 2026 OEP Report; enrollment down ~10%, net premiums doubled on avg.

Fri, 03/13/2026 - 12:56pm

HealthSource RI Open Enrollment 2026 closes with falling enrollment trend

Mar 9, 2026

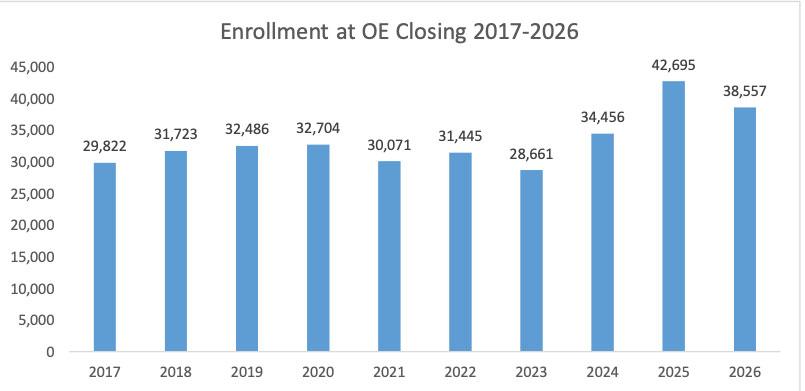

PROVIDENCE, RI – HealthSource RI (HSRI) concluded its annual Open Enrollment (OE) period January 31, with enrollment totals and the mix of plan selections bearing out expectations, as customers faced increased monthly costs upon the expiration of enhanced federal premium tax credits. Individual and Family enrollments totaled 38,557 during this Open Enrollment, a 10-percent decline from the record-high close of OE2025 (42,695). Overall enrollment decreased by 20% from year-end (48,060) to the end of OE, a highly unusual development, as the marketplace has recorded growth nearly every year in that same span.

I should note that HealthSource RI's 2025 OEP figure (42,695) is slightly higher than the official 2025 OEP plan selection total according to the Centers for Medicare & Medicaid Services (CMS), which was 42,117. Using CMS's numbers, Rhode Island is actually only down 8.5% year over year (which still isn't great, of course).

Of this year’s enrollment, 6,472 (16.8%) Rhode Island residents are newly enrolled in the affordable qualified health plans available through the state marketplace. The remaining 32,085 individuals, or 67% of last year’s customers, renewed their coverage during the same period, which started November 1.

From 2021 through 2025, historically high levels of financial assistance — available through the American Rescue Plan Act (ARPA, March 2021) and extended by the Inflation Reduction Act (August 2022) — made coverage through HSRI more affordable than ever. The enhanced premium tax credits expired on December 31 due to lack of federal action. Simultaneously, premiums rose more sharply than usual at least in part as insurers across the country, Rhode Island being no exception, anticipated shifts in the uninsured and underinsured rates in their markets.

Average premiums across the HSRI population increased by 101%, or $111 per person per month this year compared to last year. Lower-income households saw the largest percentage increase of their premiums this year. For example, a single adult household in the range of 150%-200% of Federal Poverty Level, which is about $24,000-$31,000 annually, saw their average premium go from $40 to $137. These challenges to affordability caused consumers to reconsider their options for health coverage.

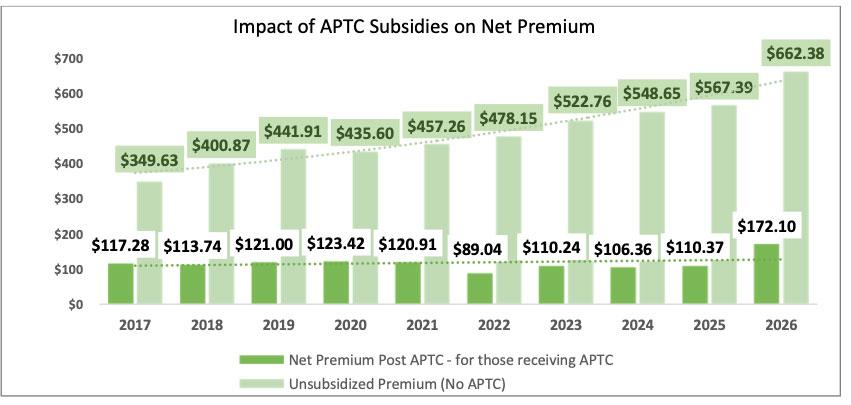

It's worth noting that average net premiums in Rhode Island still went up a whopping 56% even for those still receiving federal tax credits, as shown in this graph from the report itself:

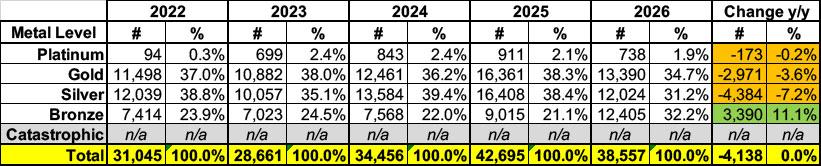

Aside from considering whether to continue or newly enroll for 2026, customers also grappled with which plans to choose, and plan selection shifted notably. Over recent years, customers had been using their enhanced financial supports to steadily migrate into silver and gold plans, which offer lower out-of-pocket costs and more predictability. That trend reversed sharply this year, with bronze plan selection rising steeply (from 21% to 32%) as silver and gold selection fell off (from 38% to 31% and 38% to 35% respectively). While customers are likely making this decision based on the affordability of the monthly premium, it comes with a trade-off – bronze plans have much higher deductibles and out-of-pocket costs, opening insured individuals up to higher bills as they use their plans. This raises concerns that as the year progresses, customers may find it unaffordable to keep their coverage as they begin to encounter those higher costs.

“It is disheartening but not surprising that, as President Trump’s policies have caused health insurance costs to skyrocket, more Rhode Islanders are struggling to pay for health coverage,” said Governor Dan McKee. “My FY27 recommended budget appropriates $9.5 million to subsidize coverage for the 20,000 hardest hit individuals purchasing insurance through HealthSource RI.”

So Gov. McKee is proposing to join several other states operating their own ACA exchanges in offering supplemental state-based subsidies to partially mitigate the lost federal tax credits. Last year around 21,000 Rhode Island enrollees earned between 100 - 200% of the Federal Poverty Level (FPL), which I'm assuming is whow McKee's 20K figure refers to.

$9.5 million / 20,000 enrollees would average $475 each or around $40/month apiece. For the example in the press release (a single adult earning 150 - 200% FPL), this would presumably knock their average premium down from $137 to $97, which would still be 2.4x as much as they paid last year but at least wouldn't be 3.4x as much as they're currently paying.

“The increase in premiums, combined with the decrease in federal supports, makes this an incredibly challenging year for folks depending on HealthSource RI for health coverage. We understand that and we are committed to working with our customers and potential customers through these difficult decisions,” said HSRI Director Lindsay Lang. “Having health coverage helps protect against one bad turn of luck becoming years of financial burden. We will work with every customer to find options that are best for their needs and budget, and continue to work with state leaders and our federal delegation to find long-term solutions.”

Since 2013, Rhode Island has decreased the uninsured rate by more than two thirds. The Rhode Island Health Information Survey, conducted biannually and last updated in 2024, pointed to an uninsured rate of just 2.2%, among the best in the country. For detailed information on both HSRI’s 2026 Open Enrollment Report and the 2024 Health Information Survey, visit HealthSourceRI.com/Surveys-and-Reports. The 2026 Health Information Survey has just begun and will be available late this year.

HSRI is still the only place where Rhode Islanders can receive Advance Premium Tax Credits to help pay for their health coverage, with customers qualifying for more than $14 million in Advance Premium Tax Credits in January 2026. Currently, 81% of HSRI customers receive financial assistance, down from 88% last year. The average premium before tax credits of all currently active plans is $662; that average drops to $172 per month after applying tax credits.

With annual Open Enrollment complete, individuals and families who have experienced certain life events may be eligible to shop for a new plan during a Special Enrollment Period (SEP), which is a 60-day window to enroll starting before or after that event. Qualifying SEP events include a loss of other coverage including Medicaid; moving into Rhode Island; marriage or divorce; or birth or adoption of a child. Individuals can visit HealthSourceRI.com/SEP to learn more about these qualifying events, register for an online info session, get live expert support through chat in English or Spanish, book an appointment, or enroll online. Enrollment support is also available by calling 1-855-840-HSRI (4774).

Here's some more data points from the report itself:

Customers who identify as Hispanic or Latino, a group whose proportions had been steadily growing over recent years, saw a 31% reduction in the number of new customers from last year.

Though stark, moderate retention and new enrollments helped to offset some of the loss HSRI had projected with the loss of enhanced tax credits – mid-2025 projections anticipated a loss of about 27% of enrollment. Notably, enrollment of those under 200% of the Federal Poverty Level (200% is about $31,000 per year for a single adult), a group most affected with highest percentage change to their monthly costs, did drop off by 27%

Enrollees are 56.8% female and 43.2% male.

Those aged 55-64 continue to make up a substantial portion of HSRI’s total enrollment, with 27.5% of enrollees, followed by those aged 45-54 (19.1%) and 35-44 (18.5%).

For 2026, HealthSource RI’s second-lowest-cost silver plan, also known as a “benchmark plan,” has an average premium of $506/month before tax credits, up from $425 in 2025, (based on a single 40-year-old), though still about 19% lower than the national average of $625 per month, and 10th lowest in the nation, down slightly from 9th last year.

In 2026, just 2,535 (6.6%) of customers are enrolled in a plan with a premium of less than $10/month after tax credits. Comparatively, in 2025, 12,909 (30.2%) of customers paid less than $10/month in premium costs.

Advertisement