California: CoveredCA confirms my 2026 avg rate hike analysis, provides details on state subsidies

Thu, 08/28/2025 - 3:44pm

This actually came out a couple of weeks ago but ironically, I've been too swamped analyzing & posting 2026 rate filings for other states to get around to posting it here until now.

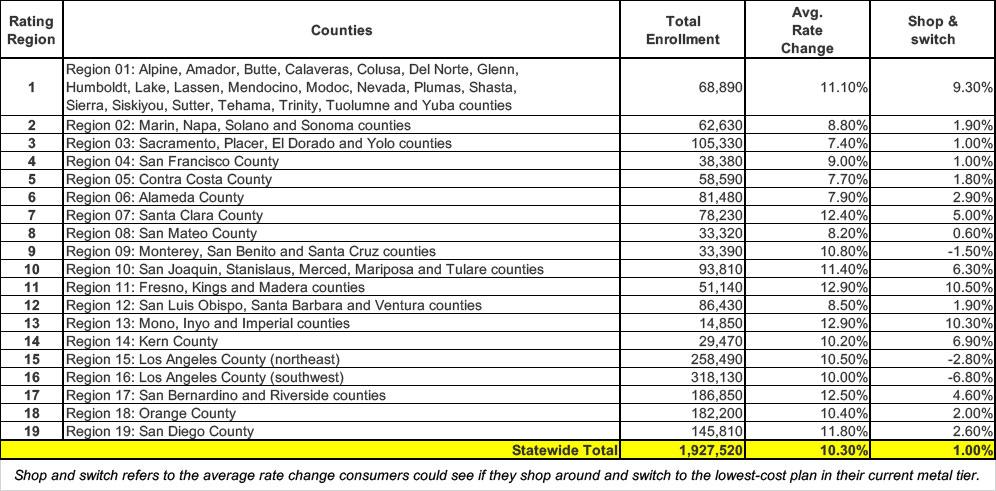

Covered California has officially confirmed the preliminary 2026 ACA individual market rate hikes, and the weighted average (10.3% statewide) is nearly identical to what I had it at a few days prior to their press release (10.2%).

August 14, 2025

Covered California Rates and Plans for 2026: Consumer Affordability on the Line with Uncertainty Surrounding Federal Premium Tax Credit Extension

La versión en español de este Comunicado puede ser descargada en este enlace.

SACRAMENTO, Calif. — Covered California announced its health plans and rates for the 2026 coverage year, highlighting a preliminary weighted average rate increase of 10.3 percent. However, this increase could be reduced if Congress takes timely action to extend the federal enhanced premium tax credits that have played a vital role in lowering costs and driving enrollment increases nationally and in California the past four years.

The proposed rate change can be attributed to many factors, including the increasing cost of health care and pharmacy expenditures, alongside broader industry challenges. Federal health care policies are driving premiums up even further, particularly the expiration at the end of 2025 of the federal enhanced premium tax credits that have helped lower premiums for millions of Americans since 2021. Combined with these rate increases, if Congress does not extend the enhanced premium tax credits, costs will rise significantly for consumers in 2026.

For California, the combined impact of the loss of enhanced premium tax credits and these premium increases would be devastating: All Covered California enrollees would see their costs increase. From the loss of the enhanced premium tax credits alone, 1.7 million enrollees in California could see an additional average net premium increase of 66 percent. This would be a catastrophic cost increase for a majority of the exchange’s enrollees, pricing many out of coverage. This story would be repeated across the nation for consumers getting health insurance through Patient Protection and Affordable Care Act marketplaces. The result would be unnecessarily higher monthly health care premiums for millions of Americans already facing rising costs and inflation.

“Skyrocketing health insurance premiums are the last thing Americans need right now,” said Covered California Executive Director Jessica Altman. “There is still time for Congress to act and protect the health care of millions of Americans who rely on marketplace coverage, and we’re hopeful that lawmakers on both sides of the aisle recognize the need to extend this essential lifeline for working families. Regardless of what happens, we’re here to help Californians access high-quality, affordable health insurance, and encourage everyone to contact us to find a plan that works for their needs and budget.”

California’s Individual Market Rate Change for 2026

Despite market uncertainties surrounding federal tax subsidies, Covered California maintains a strong marketplace, with a record-high number of enrollees, and engages in active negotiations with health insurance companies to ensure consumers are receiving the best value possible. California has also continued to support the access and affordability of health care, including state-funded assistance to Covered California enrollees that helps keep our marketplace healthy and stable. Because of these efforts, Covered California has a significantly lower average rate increase than the national average of 20 percent.

The actual national average is more like 23%, I'm afraid; I'll be posting about that separately soon.

Covered California’s 10.3 percent increase for 2026 reflects an average of proposed rates across all health insurers that offer individual plans. As it does year over year, actual rates can differ greatly by plan and region. They are subject to final review and public comment by California’s Department of Managed Health Care (see Table 1: Covered California Individual Market Rate Changes by Rating Region and Table 2: California Individual Market Rate Changes by Carrier). Final rates will take effect on Jan. 1, 2026, coinciding with the potential sunset of the enhanced premium tax credits.

While final rates are often significantly different from preliminary ones in some states, it's my understanding that California regulators usually work pretty closely with the state exchange and the carriers throughout the process, so my guess is that the 10.3% overall rate hike isn't likely to change by much in the end.

I already wrote about all of this, of course; the more significant part of the press release to me is here:

California Is Taking Steps to Protect the Most Vulnerable From Increasing Costs

In 2025, Gov. Newsom and the California Legislature increased the amount of state funds available for the enhanced cost-sharing reduction program, appropriating $165 million to expand eligibility. As a result, Californians with incomes above 200 percent of the federal poverty level ($31,300 for an individual or $64,300 for a family of four) were eligible to enroll in an Enhanced Silver 73 plan with no deductibles and reduced out-of-pocket costs.

That's right: For the past year and a half, nearly half of California's ACA enrollees have paid no deductibles thanks to the state CSR program. I don't know the exact number, but currently it applies to enrollees who earn up to 250% FPL, which includes over 1.1 million of the ~2.4 million residents enrolled in ACA individual market plans.

With the federal subsidies being dramatically reduced, however, CA is retooling this program:

This year, California is continuing to take proactive steps to shield its lowest-income enrollees from the steepest rate increases and reduce costs for consumers should the enhanced tax credits expire. For 2026, the state has allocated $190 million to provide state subsidies for individuals earning up to 150 percent of the federal poverty level, ensuring monthly premiums remain comparable to 2025 levels for those with an annual income of $23,475 for an individual or $48,225 for a family of four. It would provide some additional assistance to those earning up to 165 percent of the federal poverty level.

If I'm reading this correctly, and assuming the 2023 table still applies, it means:

- enrollees earning up to 150% FPL will still be eligible for $0-premium plans...but will face a modest $75 deductible

- enrollees earning 150 - 165% FPL will receive at least some extra premium assistance...but will go back to an $800 deductible

- enrollees earning 165% - 200% FPL will go back to an $800 deductible, plus the other premium hikes

- enrollees earning 200 - 250% FPL will go back to a $5,400 deductible, plus the other premium hikes

Around 333,000 enrollees are below 150% FPL this year, so this is great news for around 14% of the CA ACA population (I'm including the ~450K off-exchange enrollees in the total). The ~650,000 or so who are unsubsidized will "only" face the 10.3% premium increases (not great, but not devastating).

As for the remaining ~1.4 million subsidized enrollees who earn more than 150% FPL, however...they're pretty much screwed.

For those wondering:

While this funding will provide a meaningful lifeline for the lowest-income Covered California enrollees, it far from fills the $2.1 billion hole the federal government would be leaving. If Congress takes timely action to extend the federal enhanced premium tax credits, Covered California will be able to maintain the current state enhanced benefit program, which provides plans with lower out-of-pocket costs to most Covered California enrollees.

Put another way, California is canceling out around 9% of the lost federal subsidies (but they're mostly doing so by reworking the money which has been going to further reduce deductibles).

“Even in this chaotic federal environment, California is leading the way to keep marketplace health insurance affordable, and we’re so incredibly proud of the progress we’ve made covering nearly 2 million Californians in 2025,” Altman said.

“Our success is a testament to the quality health insurance that is available through Covered California, the federal enhanced premium tax credits that help reduce the cost of monthly premiums, and the value that people see in having health insurance for themselves and their families. We have lots of work still ahead of us, and that begins with Congress taking action to extend the tax credits that have helped millions of Americans.”

Covered California Remains an Affordable Option for Californians

Despite the challenges posed by federal uncertainty, Covered California’s strong enrollment, combined with one of the healthiest consumer pools in the nation, continues to attract health insurance companies. This has resulted in increased competition and choices that benefit Californians. In 2026, 11 health insurance companies will offer plans across the state, ensuring that all Californians have access to two or more choices. Additionally, 92 percent will be able to choose from three carriers or more and 75 percent will have four or more carriers to choose from.

Changes for 2026 include Aetna’s exit from the marketplace. Its nearly 21,000 enrollees in Regions 3, 5, 6, and 11 will be allowed to choose a new plan or move to the carrier with the lowest-cost plan in the same metal tier.

OK, this is the one thing which I was significantly off on in my own analysis: I estimated Aetna's CA enrollment to be more like 163,000; it's actually only around 21,000 people. This doesn't impact the weighted rate hike average, however, since Aetna's enrollees aren't included in the calculation anyway. This is actually a good thing, as it means ~140,000 fewer people will have to scramble to find another carrier than I thought...

Covered California’s commitment to affordability and access remains unwavering. Its proactive approach to negotiating rates, combined with state subsidies, showcases California’s leadership in advancing the goals of the Affordable Care Act and protecting its residents during this critical time.

Note the "Shop & switch" column, which shows some options for cutting down premiums somewhat by shopping around for a better value. This won't help much but a dollar is a dollar...

Table 2: California Individual Market Rate Changes by Carrier

- Anthem Blue Cross: 14.5%

- Blue Shield of California: 9.1%

- Balance by CCHP: 9.6%

- Health Net: 15.0%

- Inland Empire Health Plan: 17.9%

- Kaiser Permanente: 7.1%

- LA Care Health Plan: 11.0%

- Molina Healthcare: 14.7%

- Sharp Health Plan: 8.6%

- Valley Health Plan: 21.0%

- Western Health Advantage: 13.9%

- Overall: 10.3%

Advertisement