Final 2026 Open Enrollment Report: Metal Levels (Part 5B)

Mon, 04/06/2026 - 3:25pm

On Friday I posted the first half of my analysis of the various metal level enrollment shifts made by ACA exchange enrollees this year, which have special importance for 2026 given three major changes which went into effect starting January 1st:

- The expiration of the enhanced ACA tax credits, which made net premiums far more expensive for just about all enrollees;

- The termination of ACA subsidy eligibility entirely for most documented non-U.S. citizens who were previously eligible for them; and

- The state-based subsidy programs (either new, retooled or beefed up) and/or Premium Alignment pricing policies put into place by some states in an attempt to mitigate the damage caused by the first two bullets above.

The main takeaways from the prior post were that:

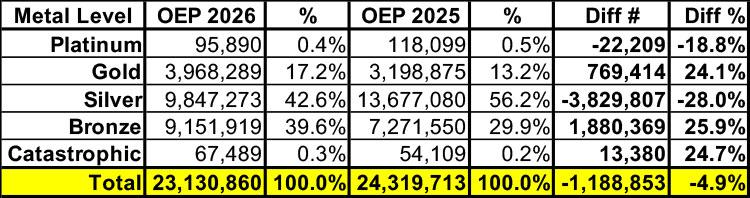

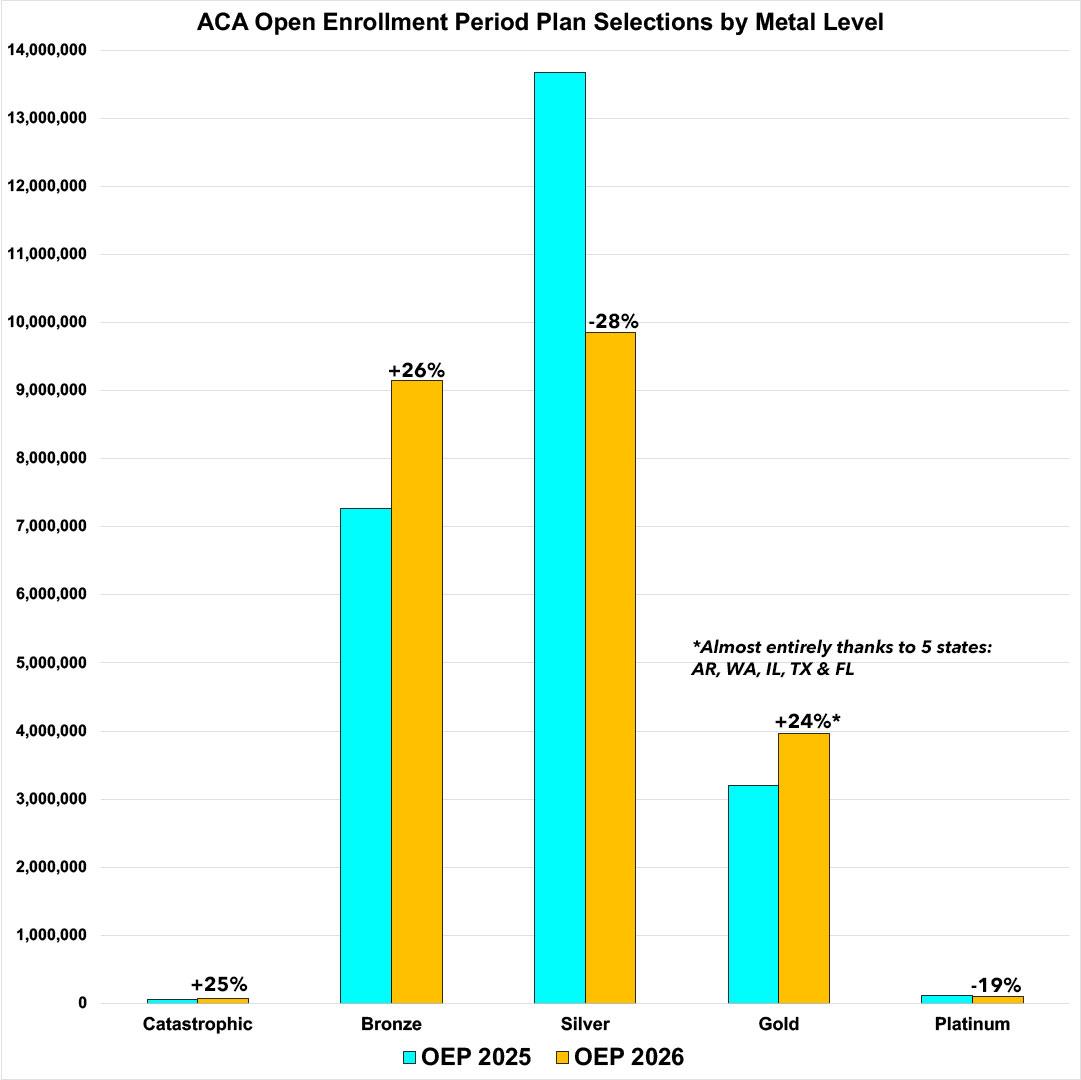

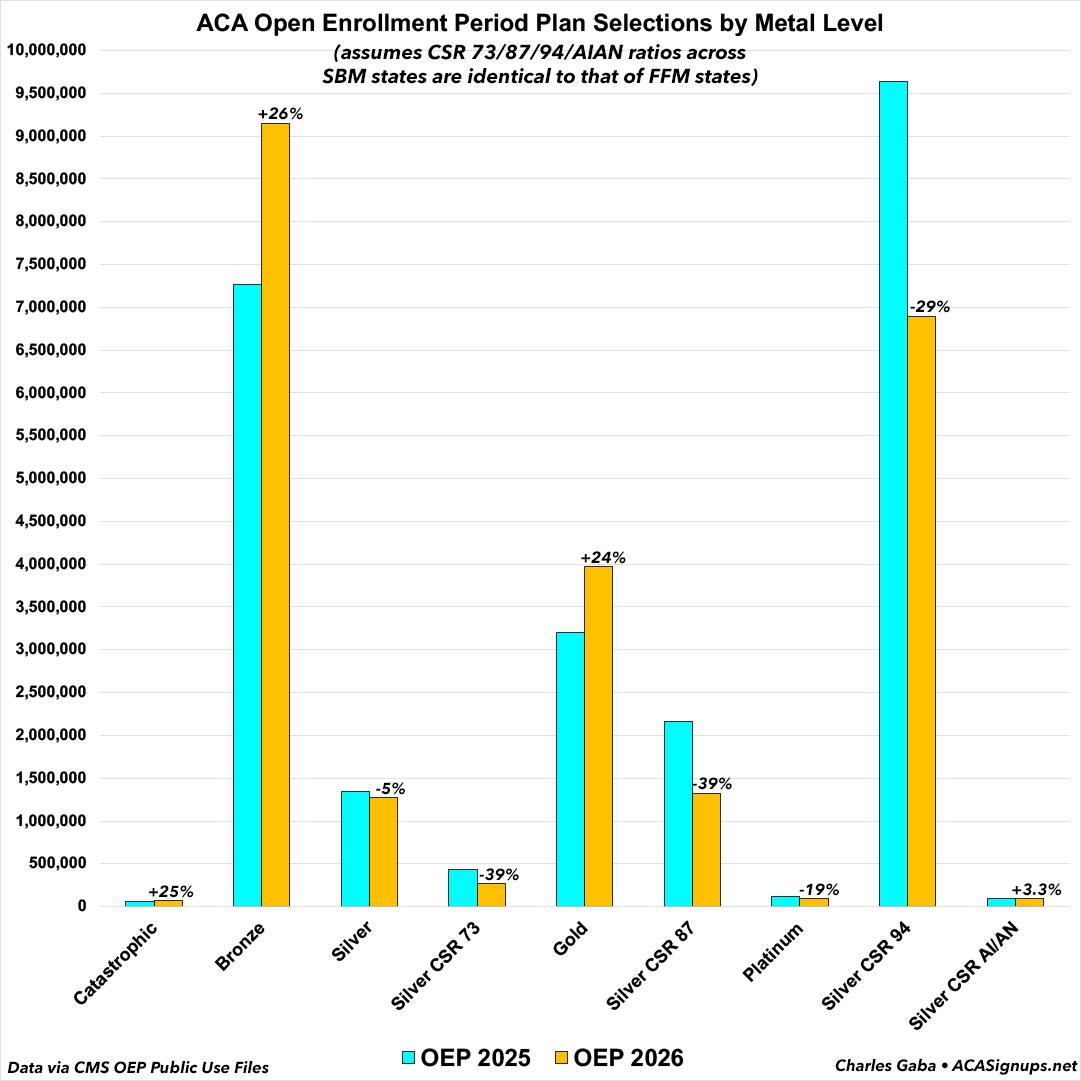

- Enrollment in Catastrophic plans did increase by 25% year over year, which sounds significant until you realize that the Trump Regime somehow thought that opening up eligibility to millions more individual market enrollees was somehow going to cause Catastrophic enrollment to skyrocket by an insane 5500%.

- Enrollment in Bronze plans also jumped by 26% year over year, which is significant given that this means that nearly 1.9 million more ACA enrollees have joined the Crazy High Deductible brigade (my own family included), which is a direct result of...

- Enrollment in Silver plans simultaneously dropping by 28% year over year as people sought to escape (or at least mitigate) the massive rate hikes caused by the lost tax credits. However...

- Enrollment in Gold plans counterintuitively increased by 24%, which may seem like a head-scratcher until you dig deeper. And finally...

- Enrollment in Platinum plans, which (like Catastrophic plans) have never been more than a rounding error, continued to dwindle, falling below the 100K threshold.

In the second half of my look at metal levels, I'm mainly focusing on why Gold enrollment increased 24% year over year nationally even though a) total enrollment dropped by 5% and b) you'd normally expect the dramatic net premium hikes to push enrollees towards lower-tier plans (which have lower gross premiums but also dramatically higher deductibles & other out-of-pocket expenses) instead of higher-tier ones.

For the most part, this is exactly what happened: Nearly 1.9 million Silver enrollees "bought down" to Bronze (or Catastrophic) plans instead. However, a surprisingly high number (around 770,000) upgraded their plans to Gold instead (the remaining ~1.2 million simply gave up and dropped their coverage entirely, which I already documented in part 1.

(It's important to note that I'm being a bit loose with some of my language here--I actually don't know how many of the additional Gold enrollees upgraded from Silver; some may have upgraded from Bronze (especially in the states which newly-implemented Premium Alignment policies), while others likely are new enrollees.)

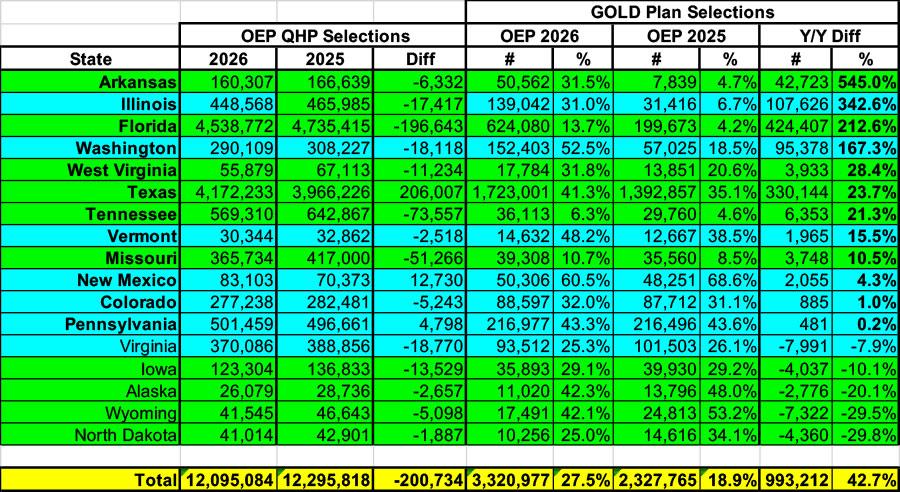

So, what's the deal with those ~770K who upgraded? Well, that's where Silver Loading & Premium Alignment once again come to the rescue. But first, let's take a look at the data. Here's 2026 Open Enrollment Period GOLD plan selections by state, sorted by how much they increased or decreased year over year on a percentage basis:

As a reminder, here's the shortest, simplest explanation of both Silver Loading and Premium Alignment...and remarkably, my source for the definition below is actually a right-wing healthcare hack who openly despises both the Affordable Care Act in general and the enhanced Premium Tax Credits in particular...but in a classic case of "even a blind squirrel finds a nut" now and then syndrome, here you go:

Premium alignment refers to the pricing of health plans on their benefit levels and not on their respective enrollees’ risk characteristics. The Affordable Care Act’s four categories of health plans (bronze, silver, gold, platinum) share the same Essential Health Benefits and were intended to differentiate their premiums largely by each category’s actuarial value. However, the silver-loading performed in the wake of CSR defunding has created a misalignment between the benefit levels and premiums in the Affordable Care Act market.

Although silver loading significantly increased silver plan premiums to offset the expense of cost-sharing reductions, their premiums generally remained below gold plan levels even though average actuarial values for silver plans generally exceeded the gold plan’s actuarial value of 80 percent.

Several states have directed their local insurers to base premiums on the plan actuarial values, which increases silver plan premiums and decreases gold plan premiums in many circumstances. As a result, premium alignment further increases PTCs and leads to a situation where many gold plans can be purchased without any consumer premium payment due to gold plan premiums being at or below the value of the Premium Tax Subsidy derived from the increased premium of the benchmark silver plan.

Put even more simply: Premium Alignment at its most robust means that a lot of people in that state become eligible for $0-premium (or at least dirt-cheap) Gold plans when they'd otherwise have to pay a significant amount for a Silver plan which has a higher deductible. Even at its weakest, Premium Alignment still makes Gold plans a considerably better value than they otherwise would have been (it also makes Bronze plans cost nothing or dirt cheap, but Gold is where the impact & benefits are far more noticeable).

In my last big posts about Premium Alignment, I explained the basics of how it works and then concluded that there were around a dozen states which had Premium Alignment pricing in place this year (3 of which--Arkansas, Illinois and Washington State--are newly implementing this pricing policy starting in 2026 specifically in response to the federal tax credits expiring). The 14 states I came up with included AK, AR, CO, IL, MD, MO, NM, PA, TX, VT, VA, WA, WV & WY, with some states pushing the adjustment factor harder than others.

My methodology for this was to pick a major city in each state, plug in a single 50-yr old earning $50,000/year (around 320% of the Federal Poverty Level, which is an ideal income for Premium Alignment to be useful), and then divide the average gross premium of every Gold plan available by the average gross premium of the Silver plans on the exchange.

I considered any state where the average Gold premium was less than the average Silver to be a Premium Alignment state.

So, how'd I do? Well, for the most part I got it right: Enrollment in Gold plans increased (in some cases dramatically) in ten of the fourteen states on my list, and Gold plan enrollment dropped (by up to 50%) in 33 of the remaining states.

However, there were a couple of exceptions on both ends: Gold plan enrollment in the other four on my list (Alaska, Maryland, Virginia & Wyoming) dropped year over year, while Gold enrollment in DC, Tennessee and Florida actually increased (dramatically in the case of Florida).

So, where was my mistake?

Well, the biggest error I made seems to have been picking a single city in each state instead of looking at statewide data; due to the different plans offered by different carriers in different parts of every state, there are some cities where the "spread" between Gold & Silver plan pricing won't be nearly as high as others, and due to the "benchmark plan" (this is the plan which the ACA tax credit formula is based on) varying widely as well, the net premiums can also vary widely for the same enrollee.

Instead, my colleague Andrew Sprung suggested that I use a different methodology: Compare the statewide average price of the lowest-priced Gold plan against the average lowest-priced Silver plan...which, as it happens, is something with healthcare analysis think tank KFF helpfully does every year.

When I plug KFF's data in, here's what it looks like next to my cruder "50 yo / $50K" methodology as well as the actual year over year change in Gold plan enrollment:

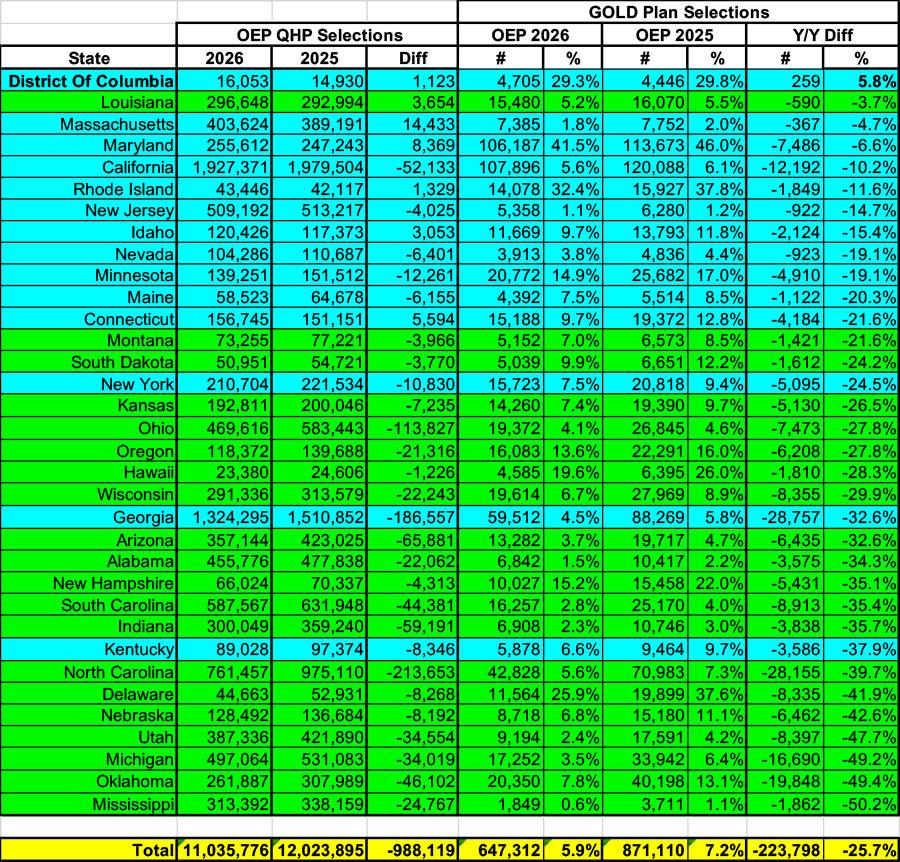

As you can see, using KFF's data seems to be a better way to go...they have 17 "likely Premium Alignment" states, of which 12 really did see increases in Gold enrollment this year, including the two biggest ones I missed: Tennessee and especially Florida.

I keep emphasizing Florida for two reasons: First, because it has by far the highest number of ACA enrollees of any state (~20% more than Texas last year; 9% higher this year even with Florida losing ~200K enrollees while Texas gained ~200K); second, because it also saw the 3rd highest percent increase in Gold enrollment (it more than tripled from ~200K in 2025 to over ~620K this year).

Here's what Gold plan enrollment looks like when you break it out into "Premium Alignment" vs "Non-Premium Alignment" states.

In the former, while there are a few exceptions, Gold plan enrollment shot up by a whopping 43% overall, ranging from a 30% drop in North Dakota (which also has the weakest Gold/Silver ratio) to an outstanding 545% increase in Arkansas (Premium Alignment was a massive hit in all 3 of the states to newly-implement it this year: Gold enrollment is 6.5x higher in Arkansas, 4.4x in Illinois and 2.7x higher in Washington State).

And then there's Florida, which, again, saw Gold enrollment more than triple even though they haven't officially implemented Premium Alignment pricing...and the word officially is the other reason it slipped by me: To my knowledge the Florida Office of Insurance Regulation never issued any sort of formal memo, policy paper or press release regarding implementing Premium Alignment, but I have it on good authority from one reliable source that yes, Florida regulators did indeed pushed their carriers to do so...and from another reliable source that at least one of the major players in the Florida ACA market, Oscar, did indeed proceed to do just that.

The net result of all of this is that across these 17 states, Gold enrollment increased by nearly a million people even as overall enrollment still dropped by 200,000. Note that nearly all of this can be attributed to just 5 states: Florida, Texas, Illinois, Washington and Arkansas...the first two of which have by far the highest ACA exchange enrollment in the country (FL & TX combined comprise 38% of all exchange enrollment), the other three of which are the ones to newly (officially) implement this pricing policy.

As for the remaining 34 states, the only one which saw a net increase in Gold enrollment is the District of Columbia...except that the numbers there are so small (from 4,446 to 4,705) that it's barely a rounding error. Otherwise, enrollment in Gold plans dropped by nearly 26% year over year, with over 223,000 fewer people selecting them...at the same time that nearly a million other enrollees dropped out of the market entirely.

I'm still left with a couple of questions about what happened with Maryland (Gold down 6.6%), Iowa (Gold down 10%), Alaska (Gold down 20%) & Wyoming (Gold down 30%), but I'm assuming there's some other local factor(s) in each which would explain them being outliers.

There's one more vitally important factor to consider here, however: Moving from Silver to Gold isn't always the same thing as upgrading. In fact, depending on their income, many people making this switch may be downgrading to a worse plan in the process...because of Cost Sharing Reduction (CSR) assistance.

As a refresher: In addition to premium tax credit assistance, which is available to most enrollees who earn between 100 - 400% of the Federal Poverty Level (FPL) on a sliding scale, the ACA also offers Cost Sharing Reduction (CSR) assistance, which helps cut down on deductibles, co-pays & coinsurance expenses...the out of pocket costs you have to pay in addition to premiums.

CSR assistance is available at three (technically four) tiers:

- Households earning 100 - 150% FPL are eligible for CSR 94 plans

- Households earning 150 - 200% FPL are eligible for CSR 87 plans

- Households earning 200 - 250% FPL are eligible for CSR 73 plans

- Members of American Indian tribes & Alaska Natives are eligible for CSR AI/AN plans

The number for each tier refers to the actuarial value (AV) which the CSR assistance makes the enrollees eligible for. Officially, Silver plans have a ~70% AV: All things being equal, a Silver plan will cover around 70% of the average (in aggregate) medical claims of those enrolled in it, while having to pay the other ~30% out of pocket in the form of deductibles, co-pays & coinsurance fees.

With CSR assistance, the AV of a Silver plan increases to either 73% (CSR 73), 87% (CSR 87), 94% (CSR 94) or effectively 100% in the case of CSR AI/AN plans (these basically cover everything with zero out of pocket expenses to the enrollee). All of these except the first are effectively Platinum plans for all practical purposes.

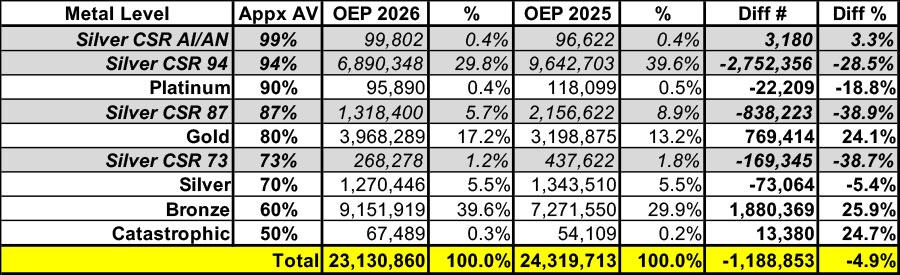

The thing is, as I noted last week, a lot of ACA enrollees have CSR plans, even if this has plummeted from 50% in 2025 to 37% of them this year....around 8.6 million people. And of those, at least across the 30 states hosted on the federal exchange, the vast majority receive the highest tiers (over 81% have either CSR 94 or CSR AI/AN coverage; another 15% have CSR 87 plans).

What this means is that over 5.5 million of the 9.8 million Silver plan enrollees in 2026--57% of them--are actually enrolled in plans which are better than Gold.

This also means that anyone who moved from a CSR 87, 94 or AI/AN plan in 2025 to a Gold plan in 2026 actually downgraded the Actuarial Value of their coverage in the process.

How many people does this apply to? Again, unfortunately, the CMS Public Use File only includes the breakout of CSR data for the 30 states on the federal exchange. The ratios are likely somewhat different for the remaining 21 states operating their own platforms; but assuming the ratios are identical, here's what that would look like for 2026 vs. 2025 (note: I'm assuming 99% AV for CSR AI/AN and ~50% AV for Catastrophic plans):

If you look at it from this perspective, suddenly Gold enrollment jumping by ~770,000 enrollees doesn't look like such a positive surprise after all...since it's likely that a significant chunk of those extra Gold enrollees came from CSR 87 or 94 Silver enrollees, not "vanilla" Silver enrollees.

If that's what happened, it means that far more of the plan shifting was "buying down" than it appears after all: There was a tiny bump in CSR AI/AN enrollment, but otherwise...

- 94% AV plans lost 2.75 million enrollees

- 90% AV plans lost 22,000 enrollees

- 87% AV plans lost 838,000 enrollees

That's a drop of over 3.6 million "Platinum Level" enrollees total...vs. a gain of ~770,000 Gold-level enrollees.

UPDATE: Thanks to a heads up from Sprung, it looks like the reality of the Actuarial Value situation is even worse than I thought. He's dug further into the metal level breakout by income bracket and concludes that...

...the shift to gold is not an upgrade in actuarial terms. MORE than all of it is at incomes below 200% FPL. Gold enrollment went down at incomes over 200% FPL. Year-over-year, increased gold selection *reduced* average AV -- though it probably kept some low-income enrollees from switching to bronze or dropping out altogether.

I'll be posting more about this as soon as I tackle the income bracket data itself...

Advertisement