Just as House lawmakers were putting together their annual “trains” — cramming multiple, tangentially related bills into hundreds of pages of amendments so they could pass them all at the 11th hour — a funny thing happened. They upped and quit.

On April 27, House Speaker Steve Crisafulli prematurely banged his gavel, ending the session, leaving the Senate holding the bag on this year’s biggest, most contentious issue: Medicaid expansion under the Affordable Care Act. Now a group of Senate Democrats has sued the GOP-dominated House, and as of this writing, the Florida Supreme Court says the lower chamber must explain its abrupt adjournment.

In a nutshell, the House doesn’t want Medicaid expansion but the Senate does. The upper chamber has a nifty non-Medicaid name for it, too. The Florida Health Insurance Exchange (or FHIX) is, in name, an attempt to help GOP senators get past the program’s unpalatable association with “Obamacare.”

OK, I just got this and it just went live, so I'm just now reading it as I'm typing this...call it "liveblogging" if you will...(Update 6:00pm: OK, pretty much done now)

4 p.m., ET, Wednesday

May 6, 2015

STUDY FINDS HEALTH COVERAGE GROWS UNDER AFFORDABLE CARE ACT

Insurance coverage has increased across all types of insurance since the major provisions of the federal Affordable Care Act took effect, with a total of 16.9 million people becoming newly enrolled through February 2015, according to a new RAND Corporation study.

Researchers estimate that from September 2013 to February 2015, 22.8 million Americans became newly insured and 5.9 million lost coverage, for a net of 16.9 million newly insured Americans.

Among those newly gaining coverage, 9.6 million people enrolled in employer-sponsored health plans, followed by Medicaid (6.5 million), the individual marketplaces (4.1 million), nonmarketplace individual plans (1.2 million) and other insurance sources (1.5 million).

...it could actually be several hundred dollars lower.

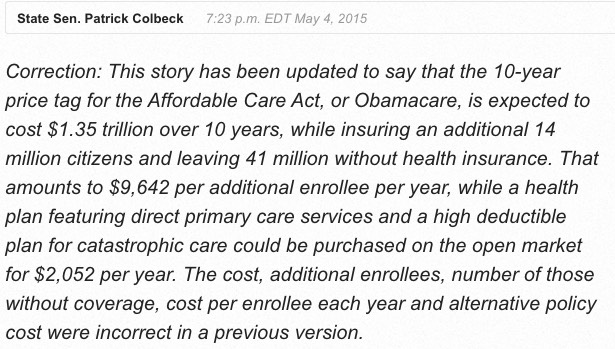

A week ago I posted a story in which I busted Michigan State Senator Patrick Colbeck for blatantly spewing nonsense numbers about the ACA in an Op-Ed in the Detroit News.

Yesterday, my follow-up story, about the Detroit News allowing Colbeck to go back in and correct some (but not all) of his insanely false factual garbage a solid 10 days later (while failing to give any indication about just how absurdly wrong he had been in the first place) went viral, generating more visitors than any other story I've posted in months.

After an all-day saga, the end result was that the Detroit News finally posted a "correction" notice...except they did so in such a disingenous way (and so long after the original editorial was publshed) as to be nearly meaningless.

I actually missed this report a few days ago, partially because I thought the February report had already been released a few weeks back; it turns out I was thinking of January's.

For January I overshot the mark a bit, but for February my projections were pretty much bang-on target, with an net incrase of 12.65 million Medicaid/CHIP enrollees to date thanks to the ACA. But wait, you're saying: The report says the net gain is only 11.7 million!

Yes, that's true...except that the 11.7 million figure only includes ACA-enabled Medicaid/CHIP additions since expansion started on 1/1/14:

Hartford, Conn. (May 5, 2015) – Access Health CT (AHCT) today announced that they enrolled 1,429 Connecticut residents during the Special Open Enrollment Period which began April 1, 2015 and ended April 30, 2015. The special enrollment period was open to individuals who did not have health care coverage in 2014 and were subject to a penalty on their 2014 federal taxes.

It's important to bear in mind that this number specifically does not include "normal" off-season QHP enrollees via marriage, birth, job loss and so forth.

1,429 over 30 days = about 48 per day. My final estimate of 3,000/day nationally would scale down to just 28/day for Connecticut specifically based on their Open Enrollment Period percentage, so this is actually pretty good.

NOTE: A few days ago there were 2 ACA-related stories which caused me some concern: The initial 2016 rate request filings out of Oregon and a new report from Standard & Poors which seems to indicate troubled waters ahead for ACA-compliant policy premiums. Unfortunately, a lot of this stuff goes way over my head. Fortunately, actuary Rebecca Stob has offered to explain why there's more (or possibly less) than meets the eye in the S&P report:

Disclaimer: I am an actuary at Group Health Cooperative in Seattle WA - this represents my personal opinion and not that of Group Health.

Just over 1 year ago I posted a long, rambling entry which boiled down to: A bunch of thank-yous to those who helped get me through Year One; a reminder that I never intended this project to continue past the 2014 Open Enrollment period; and a committment to keeping the site, blog, graph and spreadsheets cranking along through Year Two as well.

Now that we're past the official 2015 Open Enrollment period (#OE2), the "In Line by Midnight" overtime period (#ACAOvertime and the Tax Filing Season Special Enrollment Period (#ACATaxTime), it's time for me to finally let folks know what my plans are for the site for Year Three.

One week ago I posted en entry titled "Color me shocked: Michigan GOP State Senator spewing nonsense", which documented an appallingly erroneous Op-Ed by Republican State Senator Patrick Colbeck riddled with basic mathematical errors about the Affordable Care Act.

Among the many factual errors included in Colbeck's essay were such gems as:

He claimed that the ACA is costing $1.35 trillion per year. It's actually priced at less than 1/10th that price ($120 billion per year).

He claimed that the ACA has insured an additional 19 million people, which is oddly generous as compared with my own estimate of 14 million or even the Obama administration's estimate of 16.1 million.

He claimed that the ACA is "still leaving 36 million people" without insurance, while failing to acknowledge that 4 million of those are stuck in the Medicaid Gap created by Republican-run states, while another 6.3 million are undocumented immigrants who aren't legally eligible for coverage under the law.

He claimed that the ACA is costing over $71,000 per enrollee per year, when the actual number is closer to $5,000 per person.

He claimed that a "high quality policy" can be purchased on the non-ACA market for $6,000/year, which may or may not be true depending on the person.

He claimed that "159 organizations" which stand "between a patient and a doctor" were created by the ACA, which is utter nonsense.

He claimed that the state of Washington launched a program which magically cut both costs and hospitalization rates in half, without citing any source or providing any information about what this mystery program might be.

So, in my piece I carefully debunked all of these lies (or misstatements, assuming he was just ignorant). My response garnered quite a few retweets and a generally positive response...so positive that several people suggested that I write up a simplified version and submit it to the Detroit News Op-Ed page myself as a rebuttal.

Analysts at Standard & Poor's Ratings Services say the effects of funding restrictions on the Patient Protection and Affordable Care Act (PPACA) risk corridors program may cause the program to hurt small and midsize health insurers.

Drafters of PPACA created the risk corridors program in an effort to make selling health insurance under PPACA rules less risky, by using cash from health insurers with good underwriting results for 2014, 2015 and 2016 to help insurers that get poor results for those years.