The 2016 rate requests are popping up all over the place now...here's Vermont:

Blue Cross Blue Shield of VT is requesting avg. 8.38% increase for 31,147 individual exchange enrollees and 35,903 small business (small group) enrollees.

HOWEVER, it's important to bear in mind that this average a) ranges from 4.7% to 14.3% depending on the type of policy, and they seem to have mixed both individual and small group enrollments together (first time I've seen that so far). Here's the distribution; I'm not sure I understand the 2,964-enrollee difference between the totals:

As you can see, about 1.6% of enrollees would see an increase of 5% or less, while 32% would see a 10-15% increase, with the remaining 66% between 5-10%.

The 2016 Rate Request Train continues to chug along; in addition to Oregon, Washington State, Connecticut and Michigan, I can now add the District of Columbia to the list.

The first thing to note about the DC market is that one of only two (the other is Vermont) in which all individual and small group enrollments are done through the ACA exchange; no off-exchange enrollees here. That makes things a bit simpler.

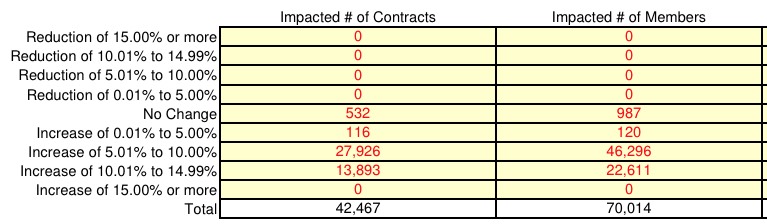

In addition, the DC Dept. of Insurance, Securities & Banking has also provided a handy table showing the year over year changes on both markets:

As you can see, DC has a pretty simple setup; 4 insurance companies operating in the Small Business (SHOP) exchange, only 2 of which are operating on the Individual exchange (and one of those, Kaiser, is only offering HMOs, not PPOs). An unweighted average of each gives the following:

I was poring over a bunch of ACA-related stories last night, many of which have to do with last week's announcement that the Hawaii ACA exchange is very close to having to shut down in 2016 just as both Oregon's and Nevada's already did in 2015.

Don't get me wrong, there's no putting a positive spin on this development (other than to say that it's not a done deal; HI Gov. Ige is still negotiating with the Federal government and a way to save the exchange may come through at the last minute). However, one curious thing jumped out at me in not one, but two different stories about the Hawaii exchange.

Hawaii’s move to the federal exchange would leave only 13 states with state-based marketplaces. Already, about a half-dozen states, including Oregon and Nevada, have had to scrap their exchanges and move to the federal system because of funding and technological issues.

Over at Politico this morning, Rachana Pradhan has an excellent article about the real-world impact of the ACA's Medicaid enrollment expansion program on, well, the expansion of Medicaid enrollment. The gist of it is that, as I've been noting for months now, additional enrollment in the Medicaid and/or CHIP programs have far exceeded "expectations" to date, with a net increase of over 12.6 million people since the ACA was passed into law (over 11.7 million of which has happened since the expansion provision officially went into effect a year and a half ago).

As far as I can tell, there are four reasons why enrollment in Medicaid/CHIP is higher than "expected":

Lawmakers and the governor reached a deal to pass a health care package that, as one senator put it, will “keep the lights on” for health care reform.

The package contains $3.2 million in new state health care spending, which is eligible for roughly another $3 million in federal match. The money will be used to level-fund exchange subsidies for out-of-pocket costs, target increases to Medicaid rates and invest in initiatives to strengthen the primary care system.

I know I said I was done writing about Luis Lang, the guy in South Carolina who's going blind and is uninsured due to a combination of his own decisions and the SC administration. However, my colleague Harold Pollack over at healthinsurance.org just posted a lengthy interview with the guy to get his take on things. Since I'm one of those who tore him to shreds, it behooves me to let him say his piece.

For a few hours yesterday, the top link on the Drudge Report led to a YouTube video in which an Ohio woman said she's going to vote for President Obama because he gave her a phone. The woman is inarticulate and she speaks loudly, and on top of those things she's black. Basically, she is exactly the kind of person many on the right envision—wrongly, it should be said—when they think of who is guzzling from the government teat these days. That she was bragging about Obama giving "every minority in Cleveland" luxuries like cell phones was just the icing on the cake.

Of course, it turns out that the "Obamaphone" brouhaha was, to put it mildly, a wee bit exaggerated (and the program was actually started by Ronald Reagan):

However, I also noted that the graph included by Gallup makes the drop look more dramatic than it really is, by not including the entire picture. I whipped up my own version which starts at 0% to give a more accurate representation; here they are again:

Nearly 12 million people signed up for health coverage plans on exchanges created under Obamacare, according to the website ACAsignups.net. [ed: hey, that's me!!]

But more than half of the adults who bought such plans had deductibles of $1,500 or more, Families USA, a Washington nonprofit organization focused on health care, found. Adeductible is the cumulative amount a person has to spend on health care before his or her insurance company starts to pay. Despite receiving tax credits to help offset the cost of coverage, these deductibles were prohibitively expensive.