My Simplified #SilverLoading Explainer

Mon, 04/05/2021 - 1:56pm

I've written in-depth explainers before of how Silver Loading came into existence and how it works as part of longer blog posts, but I also wanted to have a simpler, standalone version, so here it is.

First, a quick backstory:

- The ACA includes two types of financial subsidies for individual market enrollees through the ACA exchanges (HealthCare.Gov, CoveredCA.com, etc). One program is called Advance Premium Tax Credits (APTC), which reduces monthly premiums for low- and moderate-income. APTCs are the subsidies which have been substantially beefed up by the American Rescue Plan (the additional subsidies will be available starting in April in most states, soon thereafter in most other states).

- The other type of subsidies are called Cost Sharing Reductions (CSR), which reduce deductibles, co-pays and other out-of-pocket expenses for low-income enrollees.

- The way the CSR program works is a bit unusual. Unlike premiums, which are a set, known dollar amount for every enrollee each month, the CSR program involves deductibles & co-pays, which can vary greatly from month to month. Therefore, instead of subsidizing the enrollees directly, the insurance carriers are contractually required to cover the given portion of the enrollee's deductibles, co-pays etc. up front, and then submit their CSR expenses to the federal government on a monthly basis to be reimbursed.

- After Donald Trump cut off CSR reimbursement payments in late 2017 as part of a failed attempt to sabotage the ACA, insurance carriers, state-based ACA exchanges and state insurance commissioners broke out a contingency plan which was first laid out in an issue brief by the HHS Dept's. Assistant Secretary for Planning & Evaluation (ASPE) in 2015 to make up for their CSR losses and further discussed by analysts at the Urban Institute in 2019: Silver Loading.

- The carriers basically calculated how much they expected to have to shell out in CSR payments the following year...and then added that amount to their premiums for the following year instead.

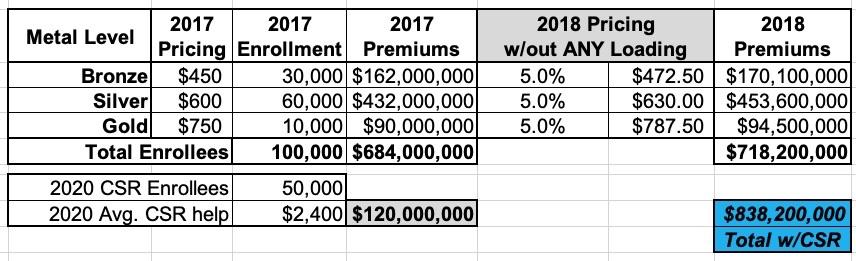

For example: Let's say in 2017 a carrier projected that overall claim expenses in 2018 would increase around 5%. To keep things simple, let's say they offered just 3 plans: One Bronze, one Silver (which happends to also be the "benchmark Silver" used to determine subsidies) and one Gold, priced at an average of $450, $600 and $750/month.

This carrier had 100,000 enrollees in 2017 and had to pay out $120 million in CSR assistance. They assumed that total enrollment and their CSR costs would be around the same (and the same ratios) in 2018 Since they knew they wouldn't get reimbursed from the federal government for their CSR costs in 2018, simply raising their premiums by 5% would mean a $120 million loss. Ouch:

So, what did they start doing instead? They loaded their projected CSR losses onto the premiums instead.

Basically, they took the total amount ($120 million), divided that by 12 months ($10 million/month) and then divided that across their projected enrollment to figure out how much to tack onto each enrollee's monthly premium to make up the difference.

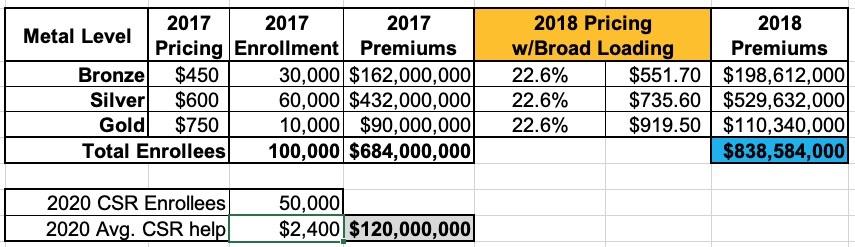

Now, if they simply divided that $10 million/month across all of their enrollees, regardless of the plan, they'd have to raise their premiums for every plan by around 22.6% to make up that difference, like so. This is called Broad Loading:

In 2018, a few states did it this way, but most states did something very clever instead: They Silver Loaded.

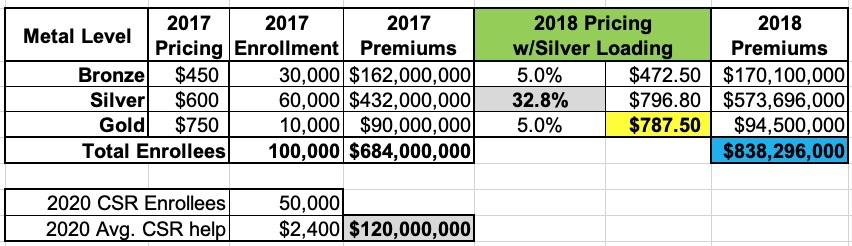

Silver loading involves concentrating the CSR costs so that they're only added to the Silver plans on the ACA market (as opposed to Bronze, Gold or Platinum). This means that instead of every plan going up by 22.6%, the Silver plans went up 32.8% while the other metal tiers only went up 5%:

The benefit of Silver Loading is that the premium subsidy program (APTC) is based on the cost of the benchmark Silver plan...but the subsidies can be applied to any plan.

Notice how the Gold plan is now priced LOWER than the Silver plan? Well, let's say an enrollee qualified for $400/month in APTC in 2017 (because the maximum they have to pay for the benchmark Silver is $200/month). In 2018, their APTC would increase from $400/mo to $597/month...but they can use that $597/mo for any plan. The Silver still costs them $200/mo, but suddenly the Gold plan, which would have cost $350/mo in 2017, only costs $190/mo! (Alternately, the Bronze plan, which would have cost them $50/mo in 2017, will cost nothing in 2018 since the APTC amount is actually more than the full-priced Bronze premium).

By 2019, nearly every carrier in every state was Silver Loading, and as of 2021 there's only two states still using Broad Loading (West Virginia and Mississippi, I believe). In 2022, West Virginia will finally start Silver Loading as well.

Silver Loading has resulted in millions of subsidized ACA exchange enrollees receiving more financial help than they would have otherwise, since a Bronze or Gold plan would now cost either about the same, less, or even nothing in premiums depending on where the enrollee lives.

This meant that the carriers got to be made whole on their CSR losses while millions of enrollees received more financial help and thus had lower net premiums for their policies....which meant that for the most part, the insurance carriers have since agreed to stick around for 2018, 2019 and beyond after all. This is exactly the opposite of what Donald Trump was hoping would happen. He basically botched his own attempt at sabotaging the ACA.

Advertisement