New Jersey: *Preliminary* avg. 2020 #ACA premiums: +8.6%

Mon, 08/12/2019 - 11:27am

New Jersey is an important state to watch, as they (along with DC) are the first state to specifically reinstate the ACA individual mandate penalty at the exact same levels as the just-zeroed out federal version. Massachusetts has a mandate penalty in place this year as well, but a) theirs pre-dated the ACA and was simply dusted off again and b) theirs uses a different formula anyway.

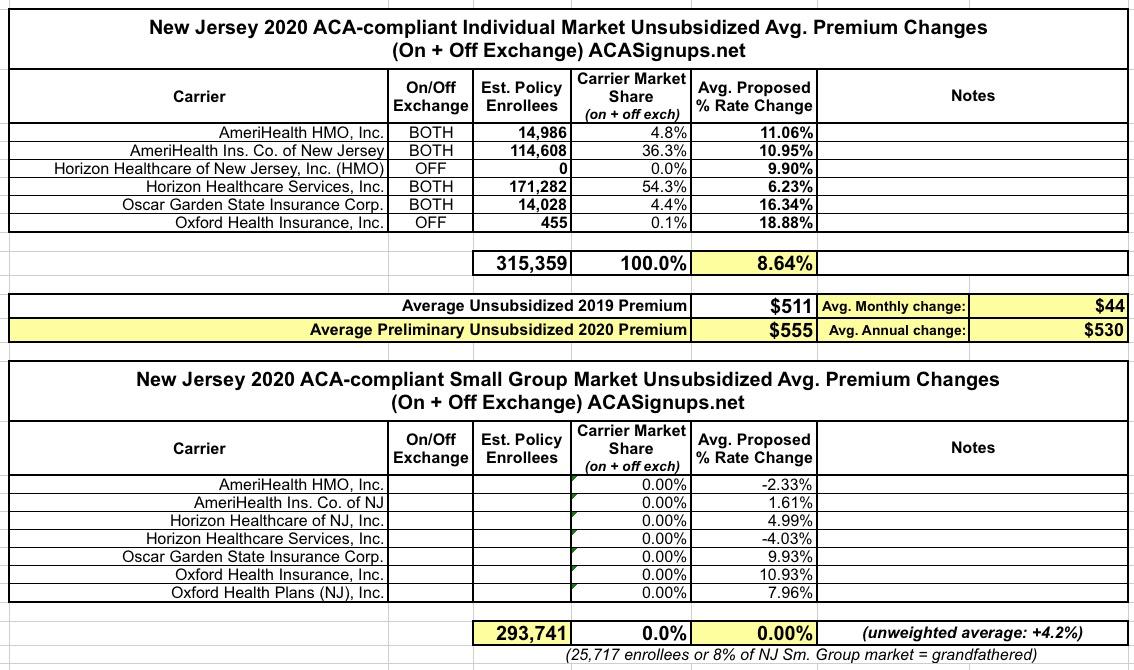

Last year, Individual Market insurance carriers in New Jersey announced that average unsubsidized 2019 premiums would be reduced by an average of 9.3% statewide due to two laws put into place by the state legislature and Governor Murphy: Reinstatement of the mandate penalty at federal levels (which lowered rates by 6.8 percentage points from +12.6% to just +5.8%) and the initiation of a solid reinsurance waiver program (which reduced rates by a further 15.1 points, for a final average change of -9.3%).

As I noted at the time, however, mandate penalties only work if a) they're strong enough to convince people to enroll in compliant coverage and b) if enough people know that the penalty exists:

There's only one problem with this: The impact of the mandate penalty is completely psychological in nature. It only works (to the extent that it does at all) if people know that they'll be penalized financially for not complying with the mandate.

Remember, the point of the mandate is not to add $700+ to the tax burden of a bunch of people; the point of it is to encourage them (detractors would say "goad") into enrolling in an ACA-compliant policy. The more (presumably relatively healthy) people do so, the healthier the ACA market risk pool is. This expectation is the very thing which caused New Jersey insurance carriers to lower their 2019 premiums by 5.8% in the first place.

HOWEVER...what if no one (or hardly anyone) in New Jersey knows about the penalty still being in place?

More specifically, what if no one who's part of the target population for enrolling in the ACA individual market (either on or off-exchange) knows that the penalty is still around, having simply shifted from the federal treasury to the state?

Massachusetts had their state-level penalty in place for a good six years before the ACA did, so their population is quite familiar with it. Furthermore, they made sure to go all out on their awareness campaign last fall, making certain that everyone in the state knew about it. I don't know how much New Jersey did on this front, but the limited info I have from my contacts there suggest that it wasn't much.

Part of that might be due to the New Jersey media market overlapping with New York's. Not only does this make TV advertising extremely expensive in the Garden State, but it also means that NJ residents were likely receiving very mixed messages, since New York hasn't reinstated their mandate. That means many NJ residents likely heard that there wasn't a mandate penalty any longer from various New York outlets. Another big problem is that, just like the federal mandate, the penalty itself isn't actually imposed until over a year later. Anyone who chose, in late 2018, to skip coverage for 2019 won't be hit with a state tax penalty until spring of 2020.

This means that there are likely to be a bunch of very surprised, very pissed-off New Jersians early next year when they file their state tax forms.

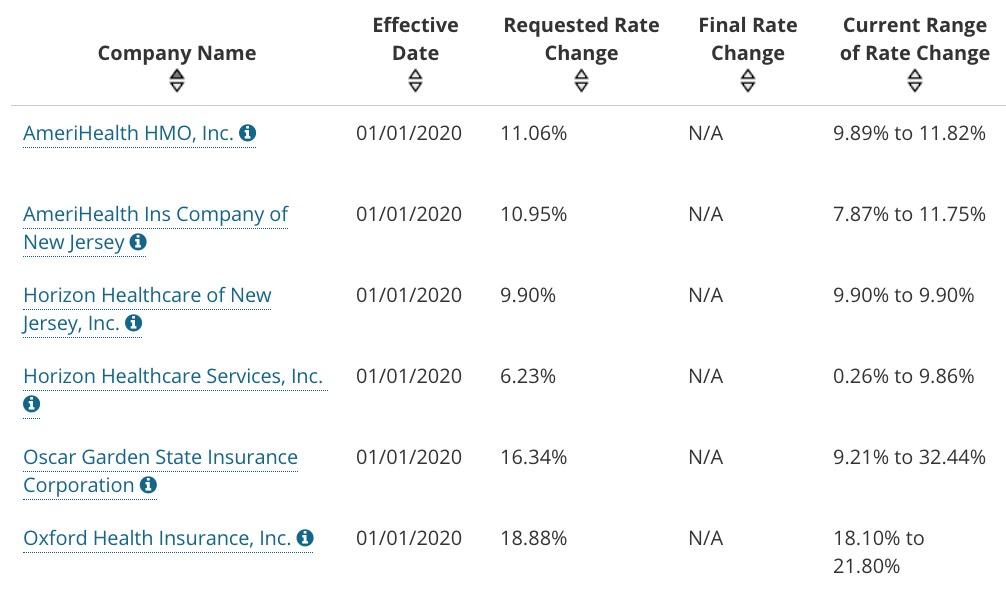

In any event, for 2020, unsubsidized ACA-compliant individual market premiums are going back up again, by a weighted average of around 8.6%. This is the 6th highest (requested) increase in the country for 2020, after New Mexico (13%), Vermont (13%), Louisiana (11.7%), Indiana (9.0%) and the District of Columbia (9.0%).

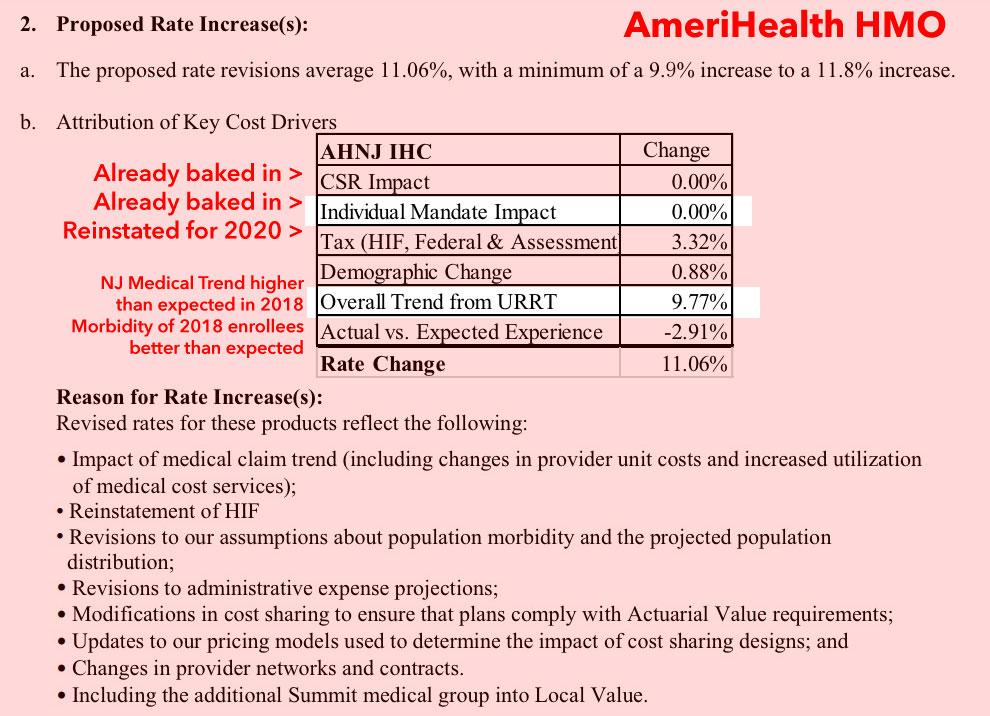

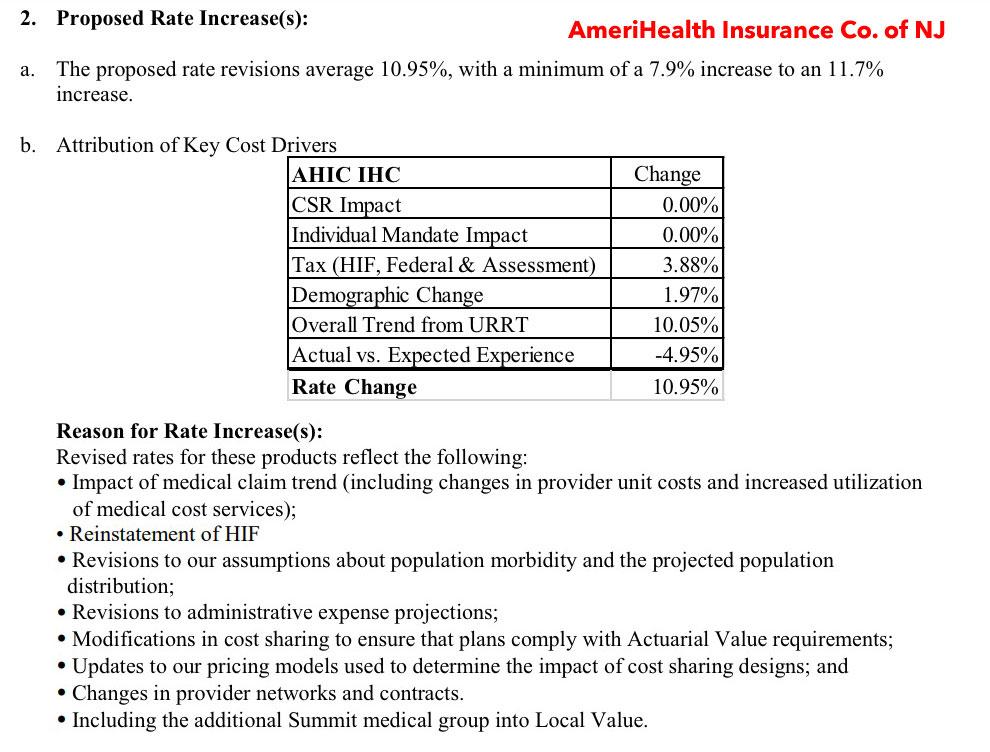

On the surface, this might make it sound like NJ's mandate reinstatement was ineffective (likely in part due to the reasons I noted above). However, the actual rate filings from two of the six carriers on the market (technically a single carrier with two divisions...AmeriHealth HMO and AmeriHealth Insurance Co.) suggest a different reason. I don't know about the other four carriers, but according to AmeriHealth:

- The reinstatement of the ACA carrier tax is cancelled out by an improved risk pool in 2018, but...

- Medical trend in New Jersey (basically, the average provider costs of medical care) shot up by 9.8%, which is considerably higher than the ~5% which various health wonks like David Anderson suggest should be the norm this year.

in short, it's too early to tell what impact, if any, NJ's reinstated penalty has had; it'll take a few years to know, especially with so many other factors at play.

Meanwhile, New Jersey's small group carriers are requesting an unweighted average increase of 4.2%.

Advertisement