Last week I noted that Ted Cruz's proposed amendment to the GOP Senate's BCRAP bill is a big pile of crap all by itself, since it would effectively turn the ACA-compliant market into a massively underfunded High Risk Pool, while likely turning the non-compliant individual market into a wasteland of subprime junk insurance (or at best, plans which are reasonable right up until you get truly sick, in which case you're screwed).

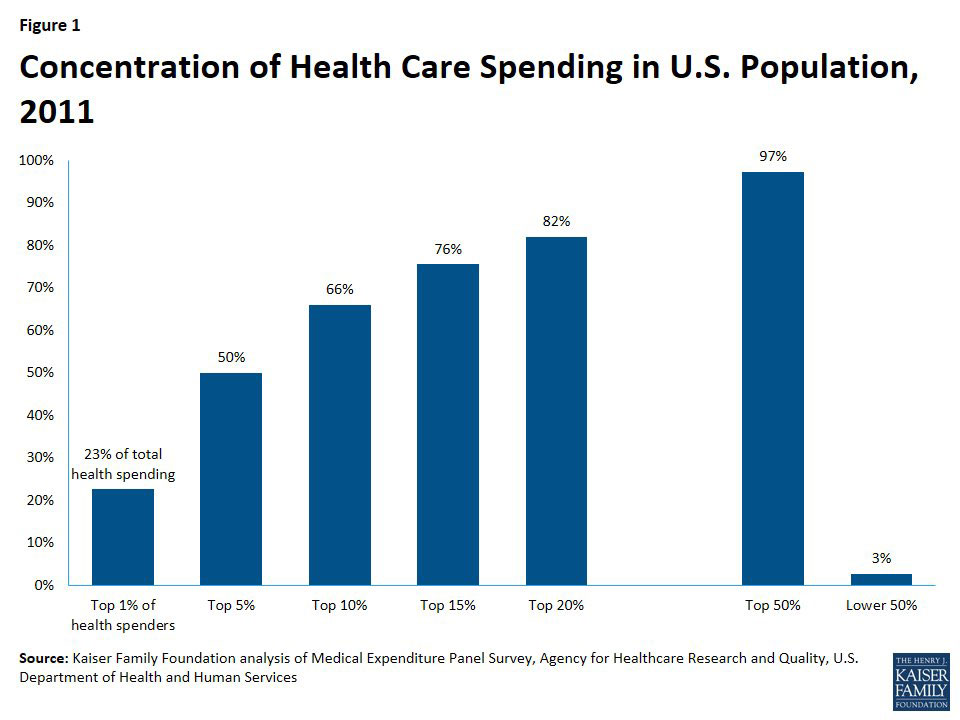

To help explain how this would happen, I used this bar graph from the Kaiser Family Foundation to show how medical expenses are actually split up by different subsets of the population:

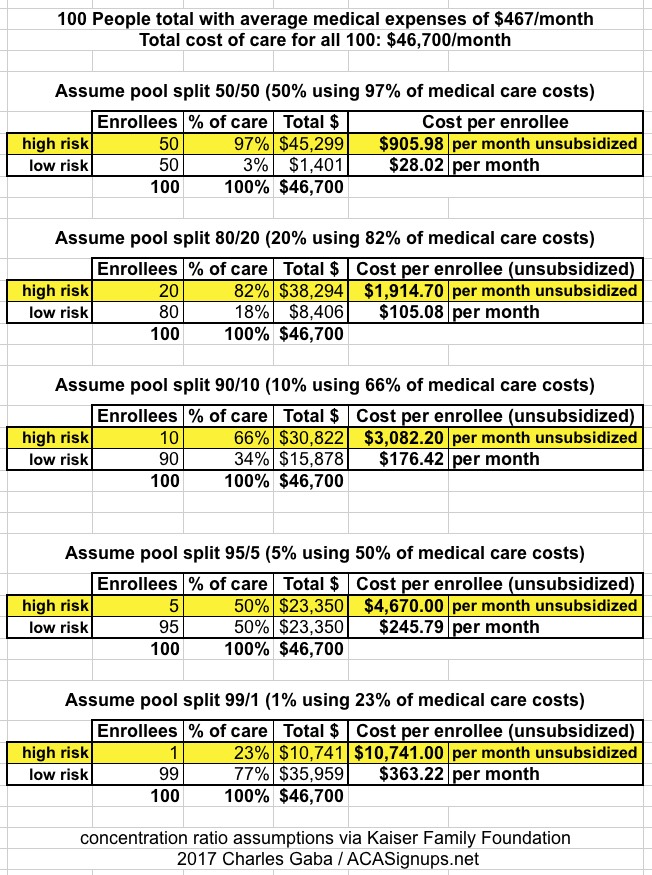

Based on these averages, I put together several scenarios showing what typical premiums might be for "ACA Enrollees" and "Cruz Enrollees" depending on how the market was split up:

His proposal, which he’s circulating to his colleagues on typed handouts, wouldn’t explicitly create and fund the special insurance markets, as the House bill did. Instead, insurance experts said, it would create a sort of de facto high risk pool, by encouraging customers with health problems to buy insurance in one market and those without illnesses to buy it in another.

...There is no public legislative language yet, but here’s how Mr. Cruz’s plan appears to work, based on his handout and statements: Any company that wanted to sell health insurance would be required to offer one plan that adhered to all the Obamacare rules, including its requirement that every customer be charged the same price. People would be eligible for government subsidies to help buy such plans, up to a certain level of income. But the companies would also be free to offer any other type of insurance they wanted, freed from Obamacare’s rules.

Several regular commenters here at ACA Signups have been wondering why the Congressional Budget Office keeps using March 2016 as the "baseline" for projecting the net impact on healthcare coverage numbers under the GOP's Trumpcare bills (the House's AHCA and the Senate's BCRAP), as opposed to the more recent January 2017 baseline. After all, according to the March 2016 baseline, the CBO was projecting that under the ACA, the total individual market would have 25 million people as of 2026 (18 million on the exchanges plus another 7 million off-exchange), whereas under the January 2017 baseline, their projections are for the individual market to only be 20 million as of 2027 (13 million on the exchanges plus 7 million off-exchange). Taken at face value, this would seem to suggest a 5 million enrollee discrepancy. This drumbeat has been taken up more recently by GOP Senators, particularly Wisconsin Senator Ron Johnson.

Three GOP senators — Shelley Moore Capito, Susan Collins, and now Lisa Murkowski — all will vote "no" on the new plan to repeal and then replace the Affordable Care Act.

Why it matters: This guarantees what was already widely expected: that Senate Republicans wouldn't be any more successful with a straight repeal plan, without a replacement, than they were with the repeal-and-replace legislation that stalled yesterday. Republicans could only lose two votes.

What's next: Senate Republicans are still likely to schedule the vote — even if it fails — because they have to prove to conservative groups (and President Trump) that they've tried everything.

Then again, who the hell knows...

UPDATE 7/18/17: REPOSTING since Mitch McConnell is now back to a "repeal with a 2-year delay" strategy:

UPDATE 7/20/17: The CBO score of BCRAP 2.0 has just been released, and while there are some tweaks/changes to their conclusions here and there, they still project about 22 million people to lose coverage by 2026 if BCRAP 2.0 is signed into law. They still expect about 15 million Medicaid enrollees to lose coverage by 2026. The only significant change on the "net loss of coverage" front is that they estimate that instead of 7 million people losing individual market coverage, they now project a net indy market reduction of 5 million...but also now expect about 2 million people with employer-based coverage to lose that, resulting in a net loss of...22 million.

I don't know if CAP plans on recrunching their numbers, since the BCRAP 2.0 bill still doesn't include the Cruz amendment which is supposedly going to be part of the final version voted on, but in the meantime, I'd imagine all numbers below could be updated by simply lowering all Individual Market column numbers by 29%...and just adding those numbers over to a new, Employer Coverage column.

Back on March 24th, a couple of hours after Paul Ryan pulled the House GOP's first ACA repeal vote, I posted the following:

CELEBRATE A FEW HOURS. Then come back and read this.

TRUMP'S PLAN B: Do everything he can to sabotage the ACA, then blame Democrats.

... there's the other doomsday possibilities, like Trump issuing an executive order stopping payment on CSR reimbursement payments to carriers.

I'll be addressing all of this and much more in the near future, of course, including my own suggestions for how the ACA should be changed to repair/improve the situation.

For the moment, however, I'm very tired, it's a beautiful Friday afternoon, and I'm going to go play with my kid for a few hours. I think I've earned it.

...and included this clip from the underrated film "Dead Again":

I've had to spend most of the afternoon/evening taking care of my kid (he has a 2-hour karate class Monday evenings), so I'm just now getting a chance to actually read the CBO's score of the GOP Senate's BCRAP bill, beyond their general summary of the score which I simply posted verbatim (with a handful of highlights and notes) earlier today.

There's a lot to digest; I'm sure everyone's already heard the main lowlights/takeaways: 22 million losing coverage by 2026 (14 million kicked off of Medicaid, 7 million losing individual market coverage, 1 million miscellaneous/rounding, I presume), "deficit savings" of around $321 billion (giving Mitch McConnell $202 billion to try and buy the votes he needs from a handful of "moderate" Senators) and so on. I'll be writing my full analysis for tomorrow, though there's probably not much point in it, since every other healthcare reporter will already have beaten me to the punch.

However, there's one little bit which infuriates me so much I have to get it off my chest right now. But first, the setup:

(I don't have time for a full analysis right now, so I'm just highlighting some key points and making a couple of notes for the moment...plenty of other reporters/bloggers/wonks are furiously writing analysis right now as well, of course)

The Congressional Budget Office and the staff of the Joint Committee on Taxation (JCT) have completed an estimate of the direct spending and revenue effects of the Better Care Reconciliation Act of 2017, a Senate amendment in the nature of a substitute to H.R. 1628. CBO and JCT estimate that enacting this legislation would reduce the cumulative federal deficit over the 2017-2026 period by $321 billion. That amount is $202 billion more than the estimated net savings for the version of H.R. 1628 that was passed by the House of Representatives.

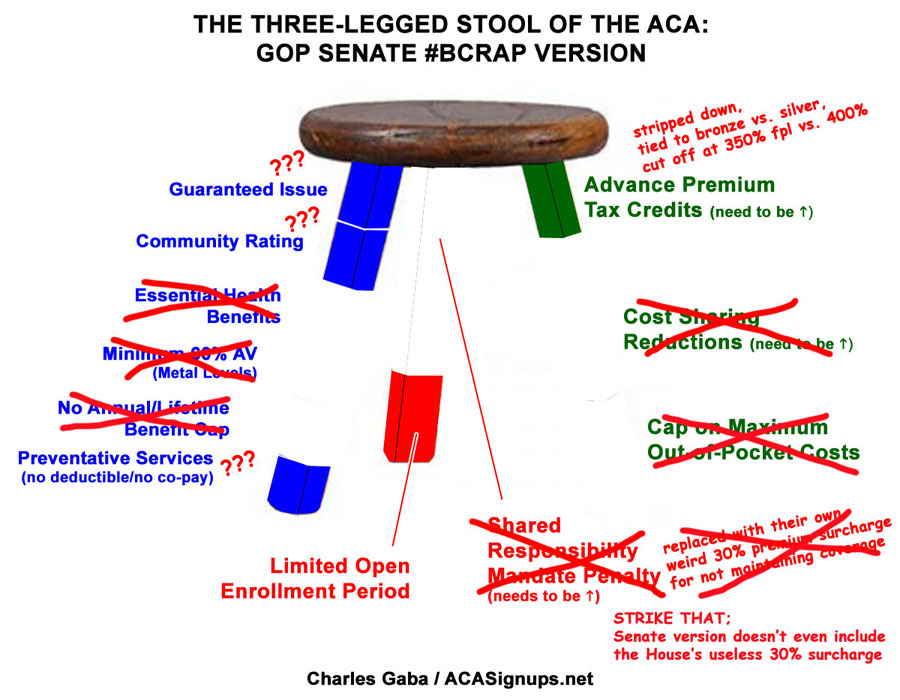

The other day it looked like the GOP Senate's BCRAP bill was going to take a hatchet to all 3 legs of the ACA's "three-legged stool", by getting rid of some provisions outright (CSR assistance and the Individual Mandate), weakening and slashing others in half (premium tax credits) and, most cynically, allowing virtually open-ended waivers which would allow individual states to wipe out many others (essential health benefits, minimum AV ratings, annual/lifetime benefits and the ACA's cap on maximum out of pocket costs). Here's what I figured this would make the "stool" metaphor look like: