MAJOR UPDATES: GOP Senate blames CBO for doing exactly what GOP House told them to.

Mon, 07/03/2017 - 10:05am

Several regular commenters here at ACA Signups have been wondering why the Congressional Budget Office keeps using March 2016 as the "baseline" for projecting the net impact on healthcare coverage numbers under the GOP's Trumpcare bills (the House's AHCA and the Senate's BCRAP), as opposed to the more recent January 2017 baseline. After all, according to the March 2016 baseline, the CBO was projecting that under the ACA, the total individual market would have 25 million people as of 2026 (18 million on the exchanges plus another 7 million off-exchange), whereas under the January 2017 baseline, their projections are for the individual market to only be 20 million as of 2027 (13 million on the exchanges plus 7 million off-exchange). Taken at face value, this would seem to suggest a 5 million enrollee discrepancy. This drumbeat has been taken up more recently by GOP Senators, particularly Wisconsin Senator Ron Johnson.

However, it's important to note that these numbers don't exist in a vacuum...both projections still assume that the total number of uninsured Americans would still be around 28 million as of 2026-2027 under current law (ie, the ACA) regardless; those 5 million people would presumably have coverage via their employer, Medicaid, etc. instead under the January 2017 projection.

Still, it's a reasonable question to ask: Why not use January 2017 estimates as your baseline if they're available? Well, according to the CBO, that's the way the GOP wanted it:

CBO acknowledges that it is using the March 2016 data. But it says it is following standard procedure in doing so.

Republicans are moving their healthcare bill through the Senate under special budget reconciliation rules that prevent Democrats from filibustering the legislation. As part of that process, they passed a budget for fiscal year 2017 in January. That budget was based on CBO’s March 2016 baseline.

CBO traditionally uses the same baseline for bills passed under reconciliation as is used for the budget. This is why it used the March 2016 data as a baseline for its score on the Senate’s healthcare bill.

Senate aides agreed that the CBO used the older data based on instruction by House GOP leaders, who did not expect the process of passing the healthcare bill to drag on for so long. At a GOP retreat in Philadelphia in January, Speaker Paul Ryan (R-Wis.) outlined a 200-day agenda that anticipated repealing and replacing ObamaCare in April.

But as the Senate continues to struggle to pass its own healthcare bill, and as centrists worry over the CBO’s findings, that is looking like a costly error.

Republican senators grilled CBO Director Keith Hall over the issue when he spoke to the GOP conference on Tuesday, the day after it issued its damning report.

...Hall, the CBO director, pushed back against GOP senators in the meeting, arguing that it could take weeks to build new models based on more recent data, setting up a contest of wills between Senate Republicans and Congress’s official scorekeeper.

In short, Paul Ryan insisted on using the March 2016 projections because it was apparently the only way they'd be able to cramp the Trumpcare bill through the Senate with only 50 votes. Now that the score based on March 2016 numbers sucks, the GOP Senate is insisting on using the January 2017 projections.

Of course, it's worth noting that even if the CBO did go with the January 2017 baseline instead, they'd lkely still project a good 17 million people losing coverage by 2027, which isn't exactly anything to cheer about either. That's only "good" news relative to how horrible the prior projections were.

It's also worth noting that the GOP Senate might want to be careful what they wish for here. Remember, the CBO's primary function is to issue budget projections. If 5 million fewer people were otherwise expected to be enrolled in subsidized exchange policies, that means that the baseline budget projection could also be quite a bit lower.

MAJOR UPDATES: I've had to rework the entire last part of this entry, correcting both the estimates in the March 2016 and January 2017 baseline projections; thanks to Larwit in the comments for bringing the 2017 correction to my attention (I realized my March 2016 error on my own):

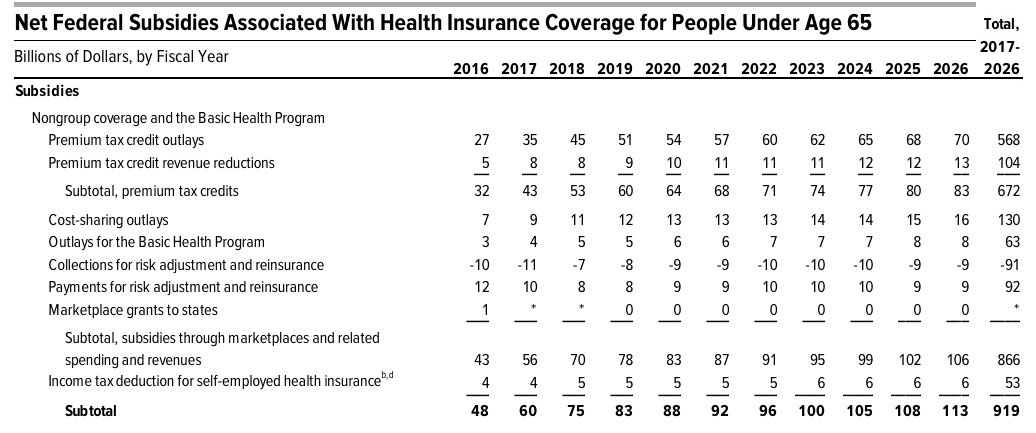

The March 2016 baseline assumes that from 2017 - 2026, the APTC, CSR & BHP programs would cost a net of $919 billion total for an average of 15.2 million subsidized enrollees per year (14.2 million receiving APTC/CSR, plus another 1 million BHP enrollees), or around $6,046 per subsidized enrollee per year on average.

Meanwhile, the January 2017 projection states:

The agencies also estimate net federal subsidies for coverage obtained through the marketplaces to be $49 billion, or 0.3 percent of GDP, in fiscal year 2017. Those subsidy amounts are projected to rise at an average annual rate of about 9 percent, reaching $110 billion (or 0.4 percent of GDP) in 2027. For the 2018–2027 period, the net subsidy is projected to total $919 billion under current law.

The January 2017 baseline assumes the exact same $919 billion...but only covering an average of around 12.5 million people per year (11.5 million APTC/CSR, plus another 1 million BHP enrollees). That works out to around $7,352 per subsidized enrollee per year on average.

Hmmm...OK, it looks like I might be wrong about my assumption above. It looks like they reduced the number of subsidized enrollees projected but also increased the projected amount of the average subsidy by about 22%, making the dollar amounts a wash. If they used the newer CBO score as the baseline, the "deficit savings" would appear to be identical after all, but with about 3 million fewer people losing coverage (since the newer baseline assumes an average of 3 million fewer covered under present law in the first place).

However, Loren Adler of the Brookings Institute reminds me that it's not as simple as that; again, as I noted above, none of this exists in a vacuum. He suspects that if they did use the January 2017 numbers, the 2027 projection might still end up with over 20 million losing coverage, since the reduction in individual market loss might be cancelled out partly by an increased loss in employer coverage and so forth. The larger point still holds, though: The law of unintended consequences may be at play here for the GOP.

Advertisement