In short, from what I can gather, the Affordable Care Act …

… the law which has consumed 99 percent of the Republican Party’s attention for the past 6 years or so …

… the law which has survived over 50 repeal attempts …

… the law which recovered from an unprecedented epic technical meltdown …

… the law which survived a federal government shutdown designed specifically to destroy it …

… the law which survived hundreds of millions of dollars worth of Koch Brothers attack ads …

… the law which survived two major Supreme Court decisions …

… proved to be worth perhaps three minutes of total airtime and discussion out of nearly four hours of Republican Party Presidential debate.

Because FOX News – FOX NEWS – had consciously decided that Obamacare is no longer a top issue to spend time screaming about.

Louise Norris has again done some of the heavy lifting for me over at healthinsurance.org, this time for New Hampshire:

In 2015, New Hampshire’s exchange had five carriers, up from just one in 2014. There will still be five carriers in 2016, although there’s one swap: Assurant/Time is exiting the market (nationwide), but Ambetter (offered by Celtic) is joining the exchange in New Hampshire.

...Two carriers in the exchange – Minuteman Health and Community Health Options – have requested double digit rate increases, although they have not yet been approved. Both carriers are CO-OPs created under the ACA, and both expanded into New Hampshire at the start of 2015, so their claims data for the state is very limited.

NOTE: The bold-faced clarifiers are important. For instance, unlike surveys by Gallup, the Kaiser Family Foundation and so forth, this report covers the full calendar year, which can make a big difference. It also cuts off as of the end of 2014, which means that none of the additional coverage added in 2015 is included.

Democrats in the Wisconsin Legislature are pushing a bill designed to prevent large increases in health insurance rates, but it’s doubtful Republicans who hold a majority and control the legislative agenda will get behind it.

The bill would require insurance companies give consumers 60 days’ notice for rate increases and require the state Office of the Commissioner of Insurance to hold public hearings on rate increases of more than 10 percent.

Over a year and half into Medicaid expansion and the launch of Kynect, the state’s health insurance exchange program, Kentucky is among the nation’s leaders in reducing its uninsured population.

As a result of providing more services to more people throughout the commonwealth, however, Kentucky hospitals are reporting healthy improvement in their revenues.

I want to get a couple of things straight right off the bat:

Yes, I wholeheartedly support single-payer healthcare...and in fact, the longer I track the ACA and the more I learn about the healthcare/health insurance system in America as a whole, the more certain I am that moving to single payer would make far more sense than the crazy-complex system we have today.

I agree with Bernie Sanders on most other issues as well, but I'm still leaning towards Hillary Clinton at the moment (and I'd be perfectly fine with Joe Biden if he were to jump in as well).

Even so, I still believe that the ACA is a massive improvement over the previous system, and I find it unlikely that single payer would be likely to happen at the national level for at least a decade or more even if Sanders were to win and the Democrats were to retake both the Senate (likely) and the House (extremely unlikely).

With all that out of the way, Tuesday's Wall Street Journal published an absolutely absurd story which tries to make it sound as though a) Bernie Sanders has proposed a specific, detailed Single Payer universal healthcare plan which b) would cost $15 trillion over the next decade c) on top of existing healthcare spending.

In my latest exclusive for healthinsurance.org, I take a deeper look at all 17 (er, 16) Republican Presidential candidates and how they might fare if "forced" to enroll via the ACA exchanges as Ted Cruz falsely claimed he had to earlier this year.

Way back in May, the requested rate hikes on the individual market for our nation's capital appeared to average roughly 5.3%. Earlier today, the District of Columbia Dept. of Insurance, Securities & Banking (DISB) announced the approved rate changes for DC:

DISB announced Sept. 15 the approved health insurance plan rates for the District of Columbia’s health insurance marketplace, DC Health Link, for plan year 2016.

Eight carriers through four major insurance companies – Aetna, CareFirst BlueCross BlueShield, Kaiser Permanente and UnitedHealthcare – will have plan offerings for individuals, families and small businesses on DC Health Link when enrollment opens Nov. 1, 2015.

As we head into the final batch of states, it looks like the national weighted average rate increases, which had been hovering in the 11-12% range up until a week or so ago, are unfortunately starting to inch upwards, slammed by 20%+ averages out of South Dakota, Montana, West Virginia, Oklahoma and Utah. Lower average rate hikes out of Connecticut and Wyoming have also been announced, but the other 5 states more than cancelled those two out.

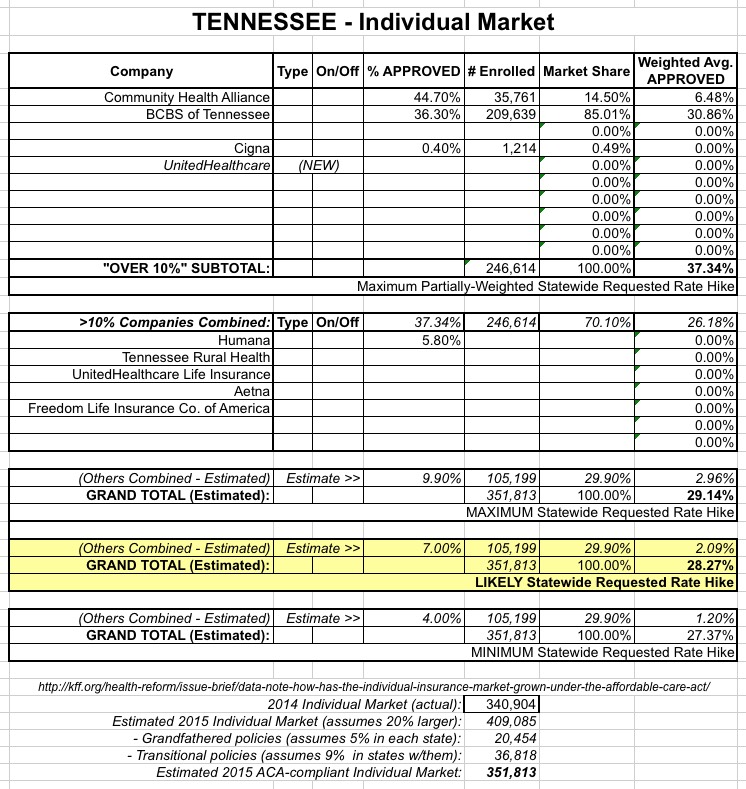

And now you can add Tennessee to the mix. Starting with Louise Norris' exchange-only data (which comes in at a 33% average hike), I've also plugged in additional off-exchange individual market numbers to come up with what looks like an overall average rate hike of around 28.3%:

Wyoming's total individual health insurance market in 2014 was just 27,000 people. While the total market likely increased somewhat this year, those gains are likely offset by perhaps 15% being either "grandfathered" or "transitional" policies.

Just over 18,000 were enrolled in effectuated exchange-based policies as of June 30 of this year, leaving perhaps 9,000 more enrolled in off-exchange plans.

According to Louise Norris of HealthInsurance.org, there's only two companies operating on the exchange in Wyoming this year: WINhealth Partners and BCBS of WY. WINhealth is asking for a 13.37% average rate hike; Blue Cross is asking for an uknown increase...except that it's under 10%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}