California: *Final* avg. unsubsidized 2024 #ACA rate changes: +9.6% (updated)

Thu, 11/02/2023 - 3:47pm

Originally posted 7/26/23; updated 11/02/23

Covered California’s Health Plans and Rates for 2024: More Affordability Support and Consumer Choices Will Shield Many From Rate Increase

SACRAMENTO, Calif. — Covered California announced its health plans and rates for the 2024 coverage year with a preliminary weighted average rate increase of 9.6 percent.

The rate change can be attributed to many factors, including a continued rise in health care utilization following the pandemic, increases in pharmacy costs, and inflationary pressures in the health care industry, such as the rising cost of care, labor shortages and salary and wage increases.

“While this is a challenging year for health care costs, Covered California’s market remains stable and continues to deliver more choices to our consumers,” said Covered California Executive Director Jessica Altman. “Despite this year’s increases, because of the extension of enhanced federal subsidies through the Inflation Reduction Act and new financial support from the state, Californians will have more help paying for their plan than ever. In fact, many consumers who receive financial help will see no change to their monthly premiums, and some will see their deductibles eliminated entirely.”

More Affordability Support Than Ever Before

Due to the structure of Affordable Care Act subsidies and enhanced financial help in California, many enrollees will not see any change in what they pay each month for their coverage in 2024. Costs will vary based on individual and family circumstances and income, but the monthly cost of coverage for many of those receiving subsidies will not increase, and in some cases it will decrease.

As a result of the extension of the enhanced subsidies provided by the Inflation Reduction Act, consumers who enroll in health care coverage through Covered California will continue to benefit from record-low monthly costs. Consistent with the current year, nearly 20 percent of enrollees will have $0 premiums.

Over one-third of enrollees would see no change or a decrease in their monthly premiums if they stay with the same carrier in the same region.In addition, thanks to new subsidies made possible by the budget package recently passed by the state Legislature and enacted by Gov. Newsom, new benefits that will further decrease the cost of health care will be available in 2024 for Californians with incomes up to 250 percent of the federal poverty level, or $33,975 for single enrollees and $69,375 for families of four.

The new state-enhanced cost-sharing program will strengthen these Silver Cost Sharing Reduction (CSR) plans, increasing the value of Silver 73 plans to approximate the Gold level of coverage and increasing Silver 87 plans to approximate the Platinum level of coverage. Silver 94 plans already exceed Platinum-level coverage. Over 650,000 enrollees will be eligible for these cost-sharing reduction benefits.

Deductibles will be eliminated entirely in all three Silver CSR plans, removing a possible financial barrier to accessing health care and simplifying the process of shopping for a plan. Other benefits will vary by plan but will include a reduction in generic drug costs and copays for primary care, emergency care and specialist visits and a lowering of the maximum out-of-pocket cost.

For example, a 27-year-old in Los Angeles County at 210 percent of the federal poverty level, or an annual income of $28,500 per year, with an Enhanced Silver plan1 will see no change in their monthly premium. The same is true for a 36-year-old in Alameda County at 180 percent of the federal poverty level, or an annual income of $24,480, who has a Gold plan. With the new subsidies in place, neither of these consumers will face any deductible if they choose any plan at the Silver level or above.

“Nearly 90 percent of Covered California’s enrollees receive financial help, with many paying $10 or less per month for their health insurance,” Altman said. “With the enhanced subsidies and increased affordability support available to consumers, access to high-quality, affordable health care has never been more within reach for Californians.”

California’s Individual Market Rate Change for 2024

While post-pandemic medical trends — such as increased utilization of health care services, medical cost inflation and labor dynamics — are driving this year’s increase, the rates are more than a one-year story.

Over the past five years, these trends, combined with a big jump in enrollment due to the COVID-19 pandemic, increased federal and state subsidies, and implementation of the state penalty for going without coverage, have all affected premium levels for Covered California in different ways.

With steady enrollment, a strong marketplace, and active negotiations with carriers to ensure consumers are receiving the best value, Covered California has held the average annual rate increase over the past half decade to just 3.6 percent. As a result, Californians in the individual market have benefited from among the lowest average rate increases in the nation over the past five years.

California’s Individual Market Rate Changes (weighted average)

- 2020: 0.8%

- 2021: 0.5%

- 2022: 1.8%

- 2023: 5.6%

- 2023: 9.6%

- 5-yr average: 3.6%

This year’s 9.6 percent increase reflects an average of proposed rates across all health insurers who offer individual plans, and rates can differ greatly by plan and region (see Table 2: Covered California Individual Market Rate Changes by Rating Region, and Table 3: California Individual Market Rate Changes by Carrier).

The preliminary rates have been filed with California’s Department of Managed Health Care (DMHC) and are subject to final review and public comment. The final rates, which may change slightly from the proposed rates, will go into effect on Jan. 1, 2024.

Increased Competition, More Consumer Choice

Covered California’s strong enrollment combined with one of the healthiest consumer pools in the nation continues to attract health insurance carriers, which has resulted in increased competition and choices that benefit Californians.

In 2024, with 12 carriers providing coverage across the state, all Californians will have two or more choices, 96 percent will be able to choose from three carriers or more, and 92 percent will have four or more carriers to choose from.

Changes to this year’s carriers include:

- Inland Empire Health Plan, one of the 10 largest Medicaid health plans in the nation that serves more than 1.6 million residents, will join Covered California and begin offering coverage in Riverside and San Bernardino counties.

- Aetna CVS Health, which joined Covered California in 2023, will expand into Contra Costa and Alameda counties next year.

- Health Net will expand into Imperial County, offering an additional HMO plan.

- Oscar Health, which serves just over 31,000 enrollees in California, announced that it will be withdrawing from California in 2024, following its withdrawal from several other markets nationwide in prior years. Enrollees will be given the opportunity to choose a new plan or to move to the carrier with the lowest-cost plan in the same metal tier.

“Increased competition benefits our marketplace and provides our enrollees with meaningful choices for their health coverage,” Altman said. “With Inland Empire Health Plan joining the marketplace and carrier partners like Aetna CVS and Health Net expanding their service areas, Covered California consumers will have more choices than ever to shop, compare and find a plan that best fits their family’s needs.”

Covered California’s Special-Enrollment Period

While the rate changes and increased choices will not go into effect until coverage begins on Jan. 1, 2024, Californians with qualifying life events, such as losing health coverage, getting married, having a baby or permanently moving to California, can enroll now during the ongoing special-enrollment period.

A full list of qualifying life events can be found here.

Consumers who sign up during special enrollment will have their coverage begin on the first of the following month.

Consumers Can Easily Check Their Eligibility and Options on CoveredCA.com

Consumers can explore their options in multiple ways, including:

- Covered California’s online Shop and Compare Tool will show consumers if they are eligible for financial help and which plans are available in their area.

- Find the nearest certified enroller for free, confidential help in multiple languages and dialects.

- Call Covered California at (800) 300-1506 to get free information or enroll by phone.

Covered California’s online enrollment portal and certified enrollers will also help people find out whether they are eligible for Medi-Cal. Medi-Cal enrollment is available year-round, and the coverage will begin the day after a person signs up.

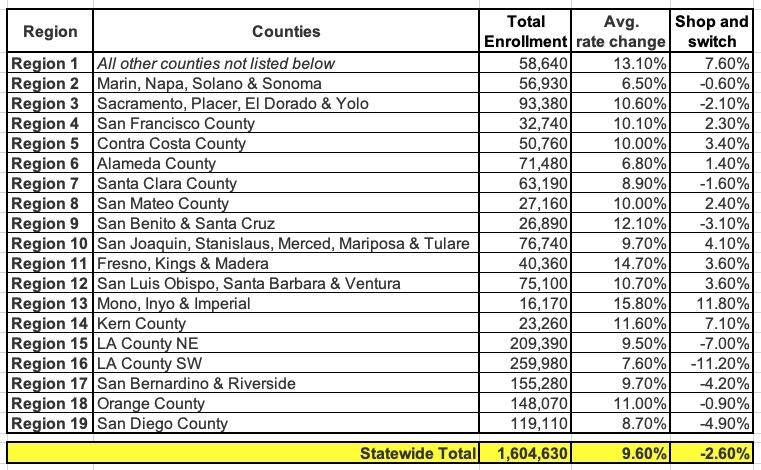

Table 2: Covered California Individual Market Rate Changes by Rating Region

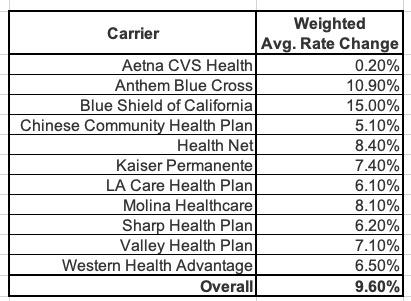

Table 3: California Individual Market Rate Changes by Carrier

- Note: Total Enrollment = Effectuated enrollment for coverage in the month of March 2023.

- Note: Shop and switch refers to the average rate change consumers could see if they shop around and switch to the lowest-cost plan in their current metal tier.

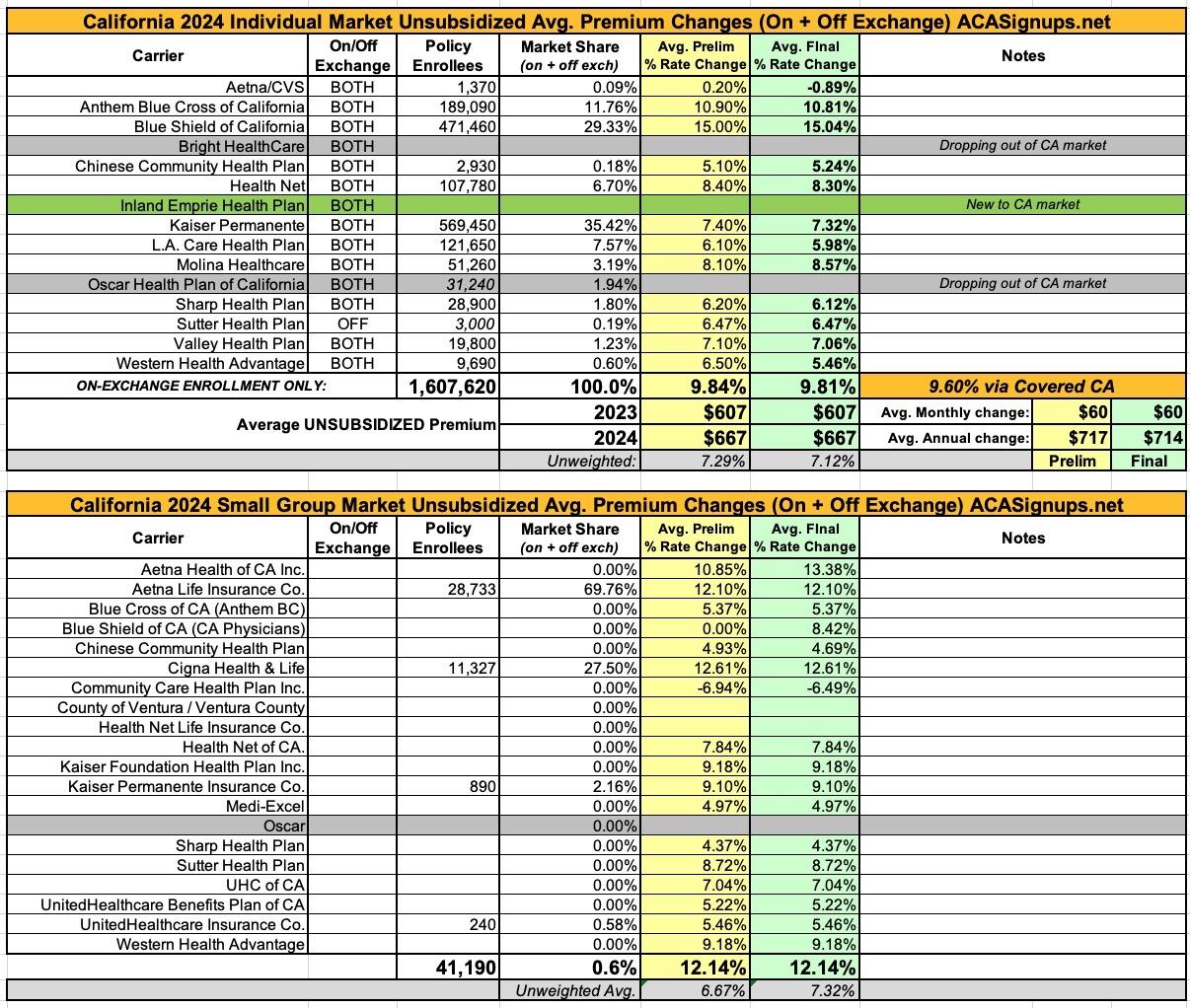

Here's how this looks when plugged into my annual rate filing spreadsheet format. The weighted average comes in slightly higher than the 9.6% stated by CoveredCA, but this could easily be due to rounding or some other clerical anomaly:

UPDATE 11/02/23: The final/approved rates have been posted to the federal Rate Review database. It looks like there were only nominal changes to a few of the preliminary rate changes--Aetna went from +0.2% to -0.9%; Western Health dropped from +6.5% to +5.5%. A few others shifted by a tenth of a point or so. Overall these amount to barely a rounding error, however.

The small group plans come in at an unweighted average increase of 7.3% (I don't have any credible enrollment data for individual carriers).

It's important to keep in mind that the enrollment numbers listed for California carriers only include on-exchange enrollment. As of 2 years ago, California still had roughly 270,000 residents enrolled in off-exchange ACA individual market policies. Curiously, a year ago the CoveredCA press release stated that the state's total individual market was ~2.3 million (which would make the off-exchange market far larger, at ~700,000). In any event, they also stated that the off-exchange market plans were similar in nature/design to the on-exhange plans, so I'd imagine the market share breakout is similar as well.

Advertisement