Washington Public Option: State legislature finally playing hardball?

Mon, 02/08/2021 - 2:25pm

Just over a month ago, I noticed that the Washington Healthplanfinder was touting the fairly impressive launch of their new "Cascade Care" healthcare plans overall (40% of new enrollees were choosing them!)...but that completely missing from all the praise was any breakout of how many were selecting the Public Option version of "Cascade Care"...likely for a very good reason:

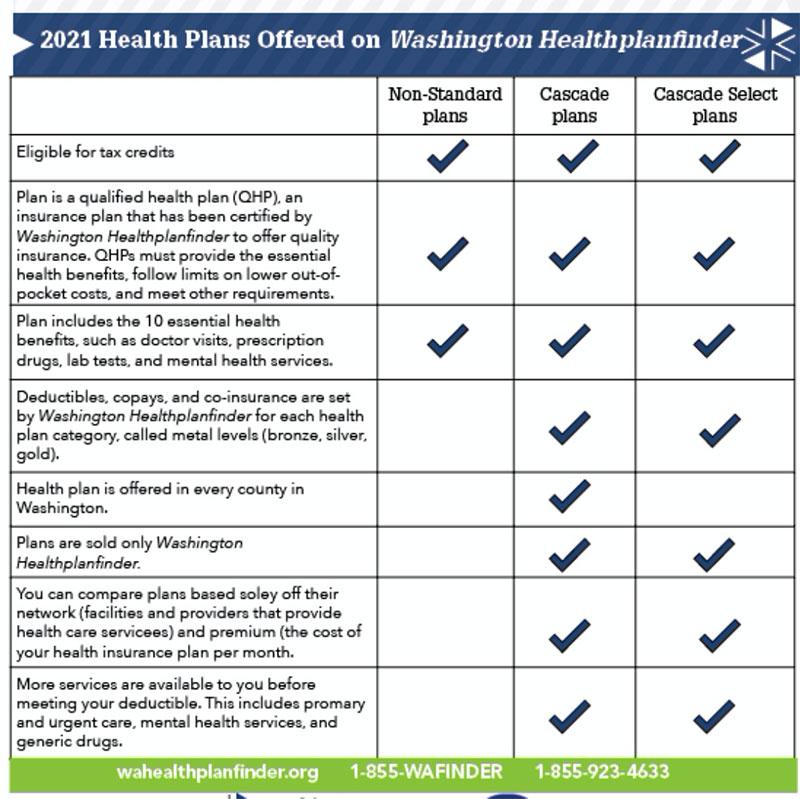

Let's step back a moment: There's actually up to three types of policies being offered depending on the carrier:

- Qualified Health Plans (QHPs)...these are the normal policies which comply with ACA regulations offered by most carriers.

- Cascade (Standard)...these are QHPs which also follow another state law passed last year (see below), and

- Cascade (Select)...these are Standardized QHPs which are also public option plans.

Here's the distinction between Cascade "standard" and Cascade "select":

SB 5526 also established standardized plans, which are statutorily required to adhere to plan designs finalized by the HBE. These plans offer lower deductibles, more services available before the deductible, and more transparent cost-sharing. Standardized plans must also allow consumers to easily compare plans by premium, network, quality, and customer service. Public option plans are required to be standardized plans and must comply with additional standards that include increasing transparency, reducing administrative burden, and aligning with state value-based purchasing models.

Here's a chart which summarizes the differences between the three. As you can see, the main distinction is that both types of Cascade Care plans have their out of pocket expenses standardized and include more zero-cost primary care services baked into the premiums:

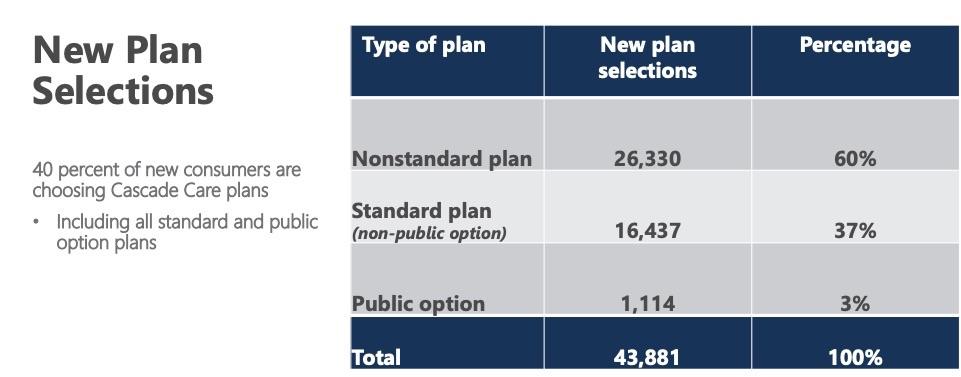

OK, so how many people actually enrolled in Public Option plans (Cascade Select) specifically? Well...they didn't say. The press release just says that ~720 had enrolled in all Cascade plans combined, which includes both Select and Standard.

The more recent press release on 12/16 didn't say either:

As of Dec. 16, about 210,000 Washingtonians have signed up for 2021 coverage, including almost 30,000 new customers. Among new customers, 41% have selected a Cascade Care plan. Cascade Care plans cover more services prior to meeting a deductible, including primary care visits, mental health services, and generic drugs. Customers who need to renew their plan for 2021 can sign in to their Washington Healthplanfinder account using the WaPlanfinder Mobile App or on WAHealthplanfinder.org and easily update and renew their coverage. Additionally, some customers may find that they qualify for free or low-cost coverage.

41% of 30,000 = roughly 12,300, so the number actually enrolling in PO plans is some subset of that. If you assume another 10K enroll by January 15th, and if you assume the 41% ratio holds for those as well, that'd bring the potential total number of both types of Cascade Care enrollees up to perhaps 16,500.

I don't know how many of those are Cascade Select (PO) plans specifically, but after discussing this with a couple of folks knowledgable about the WA individual market, I suspect that the reason why the WA Planfinder isn't breaking them out in their press releases may be because, frankly, the number is pretty small. I don't know this of course; I could be wrong...but I have a hunch that I'm not.

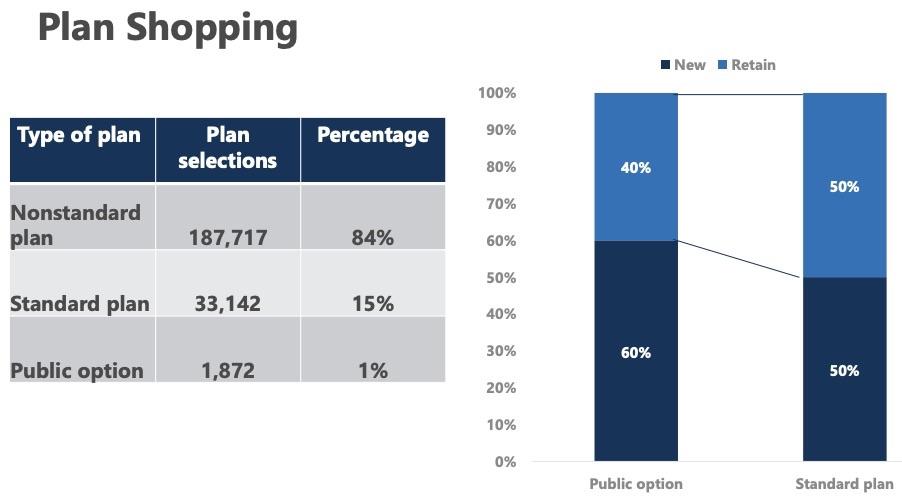

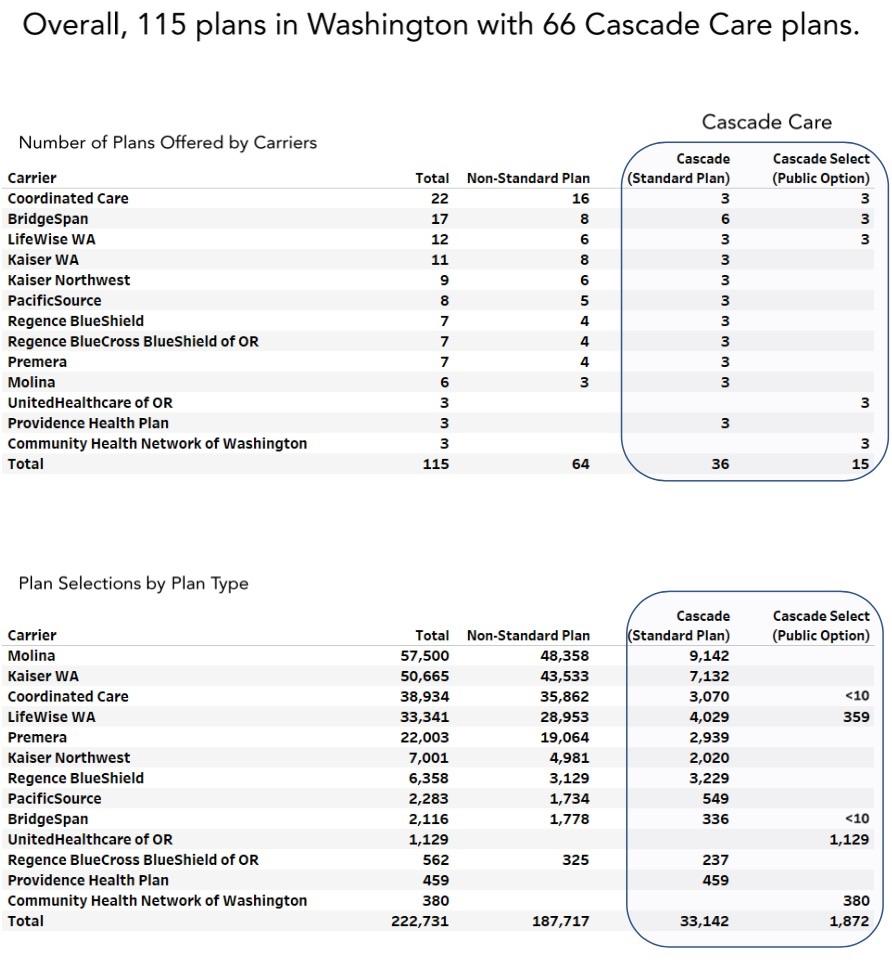

Last week, the WA PlanFinder issued their official 2021 Open Enrollment Report, and sure enough, I was right on the money:

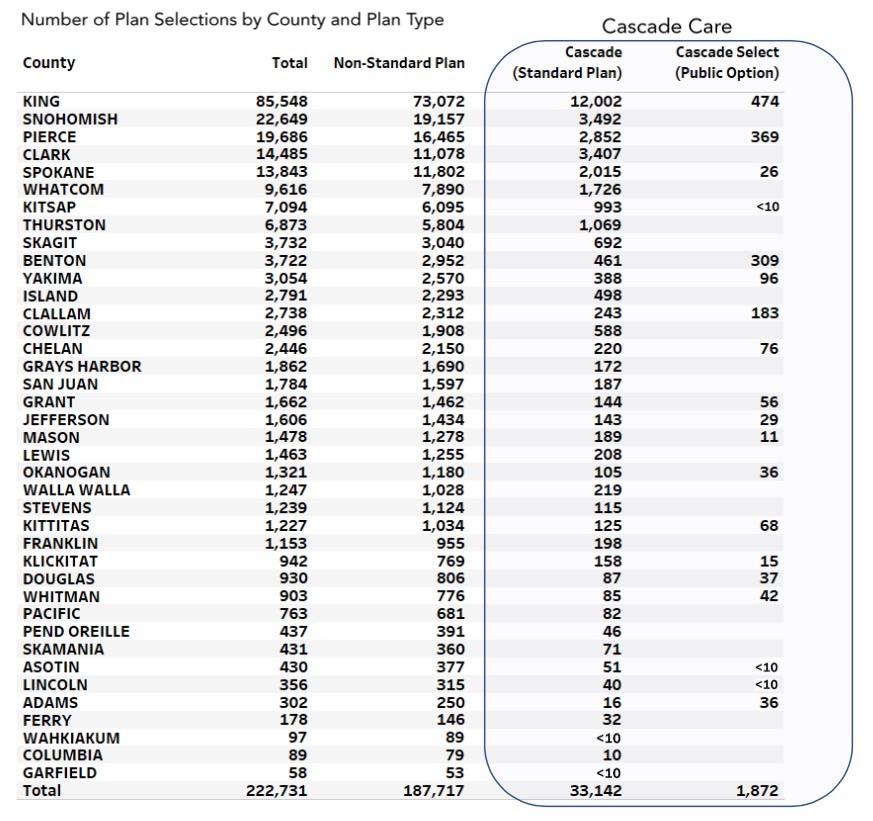

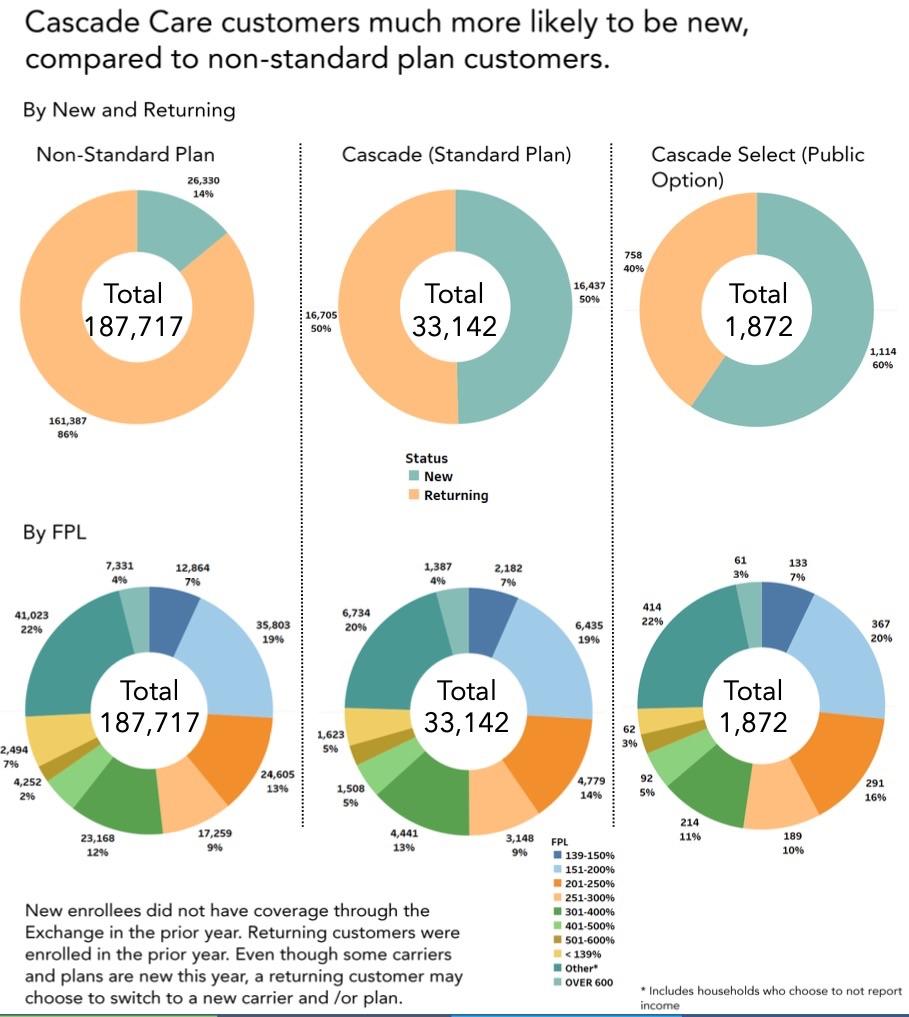

Around 16% of all enrollees were new to the exchange, and of those, around 40% chose Cascade Care plans. However, a total of just 1,872 people selected the new Public Option plans ("Cascade Select") out of nearly 223,000 total enrollees, or 0.8%, although a more fair measure is probably the 1,114 new enrollees who selected a PO plan out of nearly 44,000, or roughly 2.5%.

As I noted in my original post, there are several likely reasons for the low initial signups:

- Price: One of the biggest selling points of both the Public Option and Single Payer (Medicare for All) at the federal level has always been that it would lead to dramatic price drops in insurance premiums and out of pocket expenses compared to private insurance...but the reality is that the vast bulk of the cost of health insurance is dependent on how much healthcare providers charge. Even if you run an insurance company as a non-profit with minimal overhead expenses, that doesn't necessarily change how much hospitals, doctors, drug companies and medical device makers charge for their services/products. The PO plans were originally supposed to only pay providers Medicare rates, but the final bill ended up being set at 160% of Medicare.

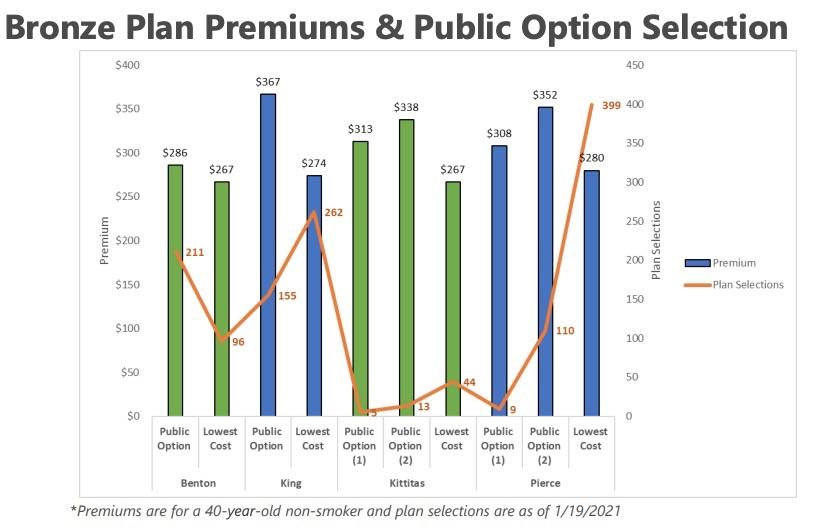

In addition, of course, baking in more zero-cost primary care services means the premiums themselves are higher instead. This point is underscored by one of the graphs in last week's OEP report: In all four of the counties listed, the lowest-priced Bronze plan was not the Public Option plan, but one of the private carrier plans:

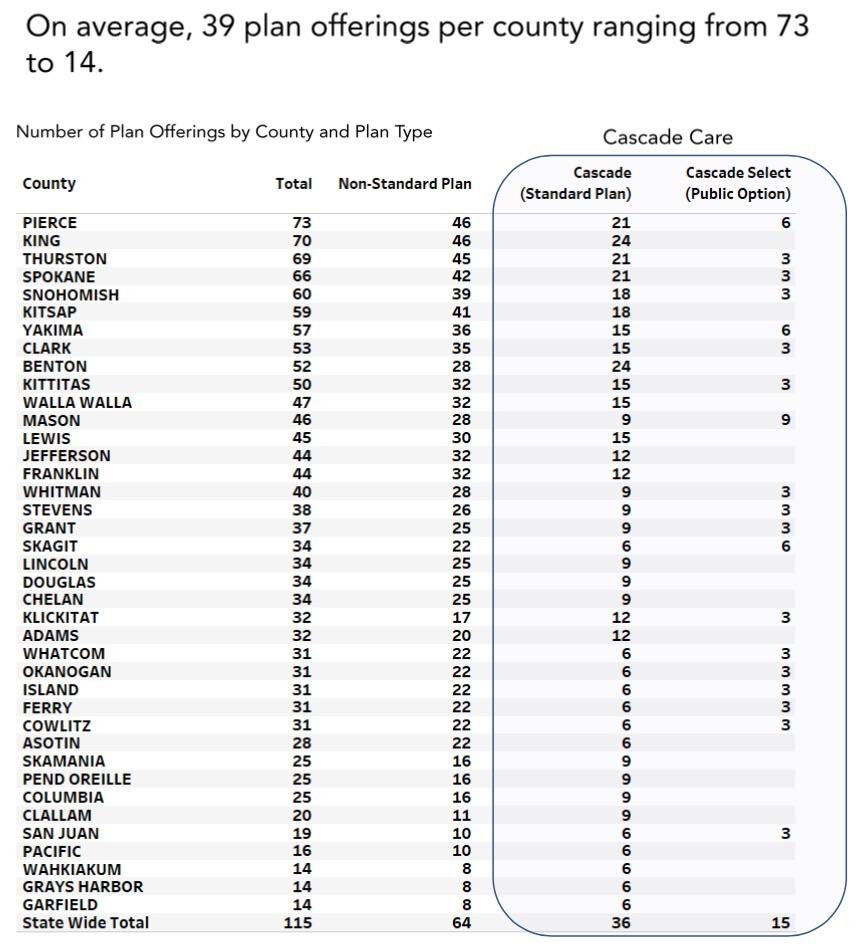

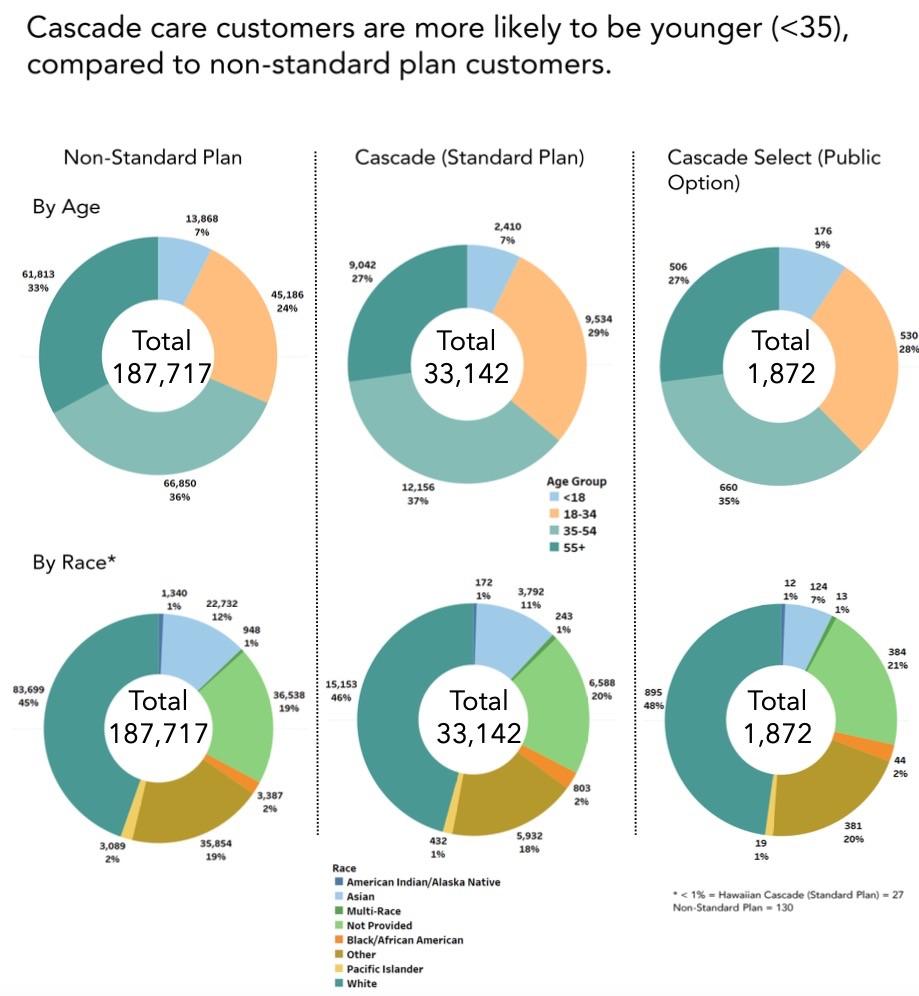

- Availability: While other Cascade Care plans are currently available in all 39 WA counties, the Cascade Select plans (PO) are only available in 19 of them. The counties in question only represent around 66% of the total state population: Adams, Asotin, Benton, Chelan, Clallam, Douglas, Grant, Jefferson, King, Kitsap, Kittitas, Klickitat, Lincoln, Mason, Okanogan, Pierce, Spokane, Whitman and Yakima Counties.

There's a lot of other factors which would have been at play, but I'm going to assume total PO enrollment would've been perhaps 50% higher if the plans were available statewide...perhaps 2,800 or so total?

- Timing: The negotiations between the state, the carriers administering the new plans and the healthcare providers were going on last spring...which is to say, right in the middle of the initial wave of the Coronavirus pandemic. Needless to say, most healthcare providers probably weren't really in the mood to talk about entering into a whole new type of insurance contract arrangement. They were...a little preoccupied with this looming threat to their capacity and bottom line.

- Prioritization: I also delved into just how the various plans are being promoted on the WA Planfinder website, and noticed that while "Cascade Care" plans are listed prominently by default, "Cascade Select" (the PO options) don't show up until #31 (at least in Seattle), which is obviously connected to the "price" item above...and if you sort by "Star Rating" (an overall ranking of the quality of networks, customer service, etc) the PO plans don't show up until #60, several pages in...because one of the only two carriers even offering the PO plans is brand new to the state, and therefore doesn't have any history to compare quality against.

Well, along with the overall 2021 OEP report, the WA exchange also released another report which specifically focuses on how the first year of Cascade Care went and the changes they plan to make in the future. In addition to what I've already noted:

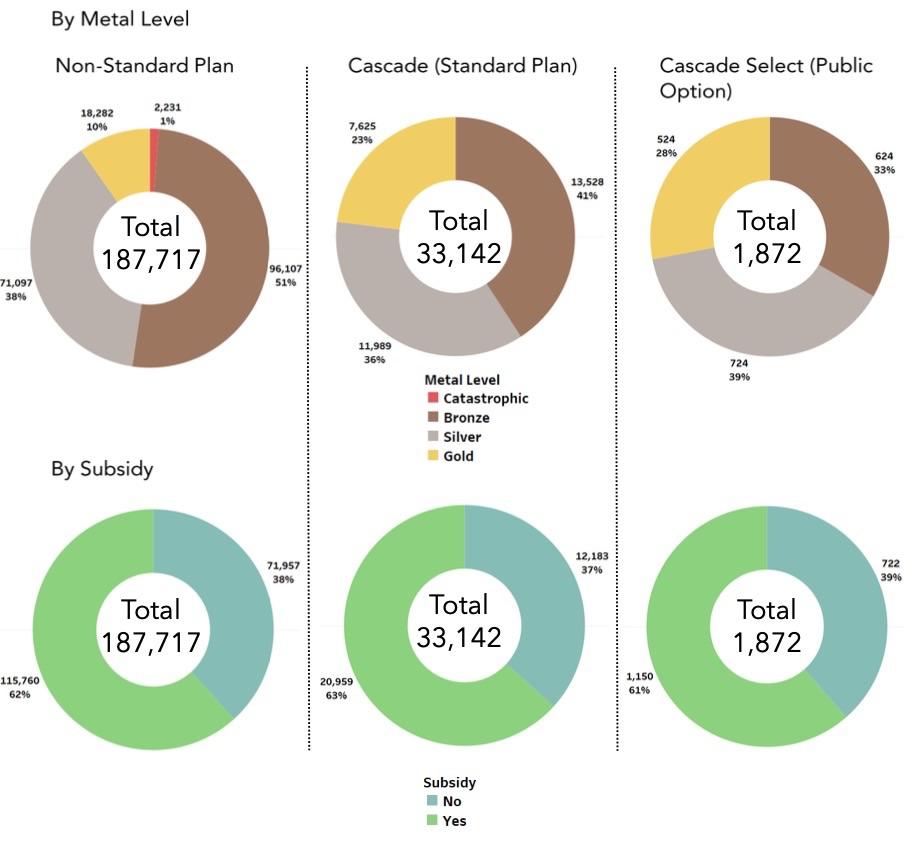

- Cascade Care (CC) deductibles average $1,000 lower than non-standardized plans

- CC Silver plans have the lowest cost in 8 counties (out of 39 total) (a typo in the report makes it impossible to tell about Bronze plans)

- 23% of those who chose a CC plan went with a Gold plan with a $500 deductible...this is twice as high as the percent of WA enrollees who chose Gold overall (12%).

The report notes that "The Exchange is continuing to work with interested legislators to improve the stability and affordability of the individual market and provide better value for Exchange customers" before going on to a whole bunch of breakout tables & donut graphs:

OK, so what about next year? Well, that's where an interesting piece of legislation comes in: SB 5377. Here's the Senate Bill Report:

Background:

... In 2019, the Legislature passed ESSB 5526, which created standardized health plans on the Exchange. The Exchange, in consultation with the Health Care Authority (HCA) designed standardized plans at the bronze, silver, and gold metal tiers. The standardized plans are designed to reduce deductibles, make more services available before the deductible, provide predictable cost sharing, maximize subsidies, limit adverse premium impacts, and encourage choice based on value, while limiting increases in health plan premium rates.

Beginning on January 1, 2021, any health carrier offering a QHP on the Exchange must offer one standardized silver plan and one standardized gold plan on the Exchange. If a health carrier offers a bronze plan on the Exchange, it must offer one bronze standardized plan on the Exchange. Carriers may continue to offer non-standardized plans on the Exchange, but a non-standardized silver plan may not have an actuarial value less than the actuarial value of the silver standardized plan with the lowest actuarial value.

ESSB 5526 also established state-procured QHPs, or public option plans. These plans are standardized plans that must meet additional participation requirements to reduce barriers to maintaining and improving health and align to state agency value-based purchasing, including standards for population health management, high value and proven care, health equity, primary care, care coordination and chronic disease management, wellness and prevention, prevention of wasteful and harmful care, and patient engagement.

The total amount a public option plan reimburses providers and facilities for all covered benefits in the statewide aggregate, excluding pharmacy benefits, may not exceed 160 percent of the total amount Medicare would have reimbursed providers and facilities for the same or similar services in the statewide aggregate. Beginning in 2023, the director of HCA, in consultation with the Exchange, may waive the Medicare reimbursement requirement if HCA determines selective contracting will result in actuarially sound premium rates that are no greater than the plan's previous plan year rates adjusted for inflation using the consumer price index. The public option plan's reimbursement rates for critical access hospitals and sole community hospitals may not be less than 101 percent of allowable costs.

So far this just explains the background of the ACA exchange in Washington State and of both types of Cascade Care plans. However, there was an additional provision of ESSB 5526: Adding state-based ACA subsidies to partially address the ACA "subsidy cliff" problem, similar to how California has done:

The Exchange, in consultation with HCA and the commissioner, was required to develop a plan to implement and fund premium subsidies for individuals whose modified adjusted gross incomes are less than 500 percent of the federal poverty level and who are purchasing individual market coverage on the Exchange. In 2020, the Exchange released its report on Senate Bill Report - 2 - SB 5377 premium subsidies, recommending a fixed dollar subsidy program and providing analysis and modeling for a $200 million, $150 million, and $100 million program.

The next part explains the new bill, SB 5377:

Summary of Bill:

Premium and Cost-Sharing Subsidies. Subject to the availability of amounts appropriated for this specific purpose, the Exchange must establish a premium assistance program, and it may establish a cost-sharing reduction program. The Exchange must establish the procedural requirements for eligibility and participation in the program and requirements for facilitating payments to carriers.

To be eligible for the program, an individual must:

- be a resident of the state;

- have an income up to 500 percent of the Federal poverty level;

- be enrolled in the lowest cost bronze, silver, or gold standardized plan offered in their county;

- apply for and accept all advanced premium tax credits;

- be ineligible for minimum essential coverage through Medicare, Medicaid, or Compact of Free Association islander premium assistance; and

- meet other criteria established by the Exchange.

Interestingly, under these criteria, the extra assistance would not be available to anyone enrolled in the benchmark Silver plan, which is defined as the 2nd-lowest cost Silver plan available on the exchange...you'd have to enroll in the lowest-cost Bronze, Silver or Gold plan, which is an odd requirement, but whatever. However, it then goes on to say:

Alternatively, eligibility criteria may be established in the budget.

...which pretty much cancels out those requirements. Huh.

The Exchange, in consultation with HCA and the Office of the Insurance Commissioner, must explore all opportunities to apply for federal waivers to:

- receive federal funds for the implementation of the subsidies program;

- increase access to qualified health plans; and

- implement or expand other Exchange programs to increase affordability or access to health insurance.

In other words, they have to do what they can to dig up funding from the feds before tacking on taxes or fees at the state level.

The state health care affordability account is created in the state treasury to hold funds for premium and cost sharing assistance programs. A carrier must accept payments for premium or cost-sharing assistance provided through the subsidies program and must clearly communicate premium assistance amounts to enrollees as part of the invoice and payment process.

In other words, the money has to be kept segregated from the general fund and carriers have to accept state-based exchange subsidy funds for premiums or cost sharing, as well as clearly letting the enrollees know that a chunk of their premiums/deductibles/etc. are being paid for through the state program.

It's the other part of the bill which addresses changes to the Cascade Care program:

Public Option Participation and Reimbursement. Beginning in plan year 2022, at the request of a public option plan, an ambulatory surgical facility or a hospital that receives payment for services provided to enrollees in Public Employees Benefits Board, School Employees Benefits Board, or Medicaid, must contract with the public option plan to provide in-network services to enrollees of that plan.

Dammmn. This legislation has some serious teeth--the state is basically requiring large chunks of hospitals throughout the state to accept Cascade Select (PO) plans if they accept Medicaid or any public employee policy, including teachers and other school administrators.

But wait, there's more:

A hospital reimbursement rate formula is established for inpatient and outpatient hospital services provided to enrollees of a public option plan on or after January 1, 2023. The rate formula must be based on a percentage of the Medicare reimbursement rates, with the base reimbursement rate for hospitals not exceeding 135 percent of the amount Medicare would have reimbursed the hospital. The reimbursement rate may be adjusted as follows:

- a hospital with a percentage of medicaid patients that exceeds the statewide average must receive up to a five point increase in its base reimbursement rate, with the actual increase to be determined based on the hospital's percentage share of medicaid patients; and

- a hospital that is efficient in managing the underlying cost of care, factoring the hospital's total margins, operating costs, and net patient revenue, must receive up to a five point increase in its base reimbursement rate.

So much for that 160% of Medicare rule. If passed and signed into law, starting in 2023 this would lock those hospitals in at 135% of Medicare...except that those with an unusually high percent of Medicaid patients can be bumped up to 140%, as can hospitals which prove that they can crack down on their expenses.

I have no idea how well this will work; I'm sure there will be legal challenges, and even if it survives those, it might be a disaster...but it might also be a huge success, since one of the biggest problems in rising healthcare prices is runaway hospital costs.

By December 1, 2022, HCA, in collaboration with the Exchange, must establish the hospital reimbursement rate in rule. HCA may adopt rules to ensure compliance with participation and reimbursement requirements and may take action against a hospital or ambulatory surgical facility that fails to comply with the requirements.

By December 15, 2024, HCA, in consultation with the Health Care Cost Transparency Board and the Exchange, must submit a report to the Legislature with recommendations on any adjustments to the base reimbursement rate or other factors to be considered in the hospital reimbursement rate formula.

HCA's authority to waive the 160 percent of Medicare reimbursement benchmark requirement if it determines selective contracting will result in actuarially sound premium rates that are no greater than the plan's previous plan year rates, is repealed.

Wow. They really aren't screwing around here. Again, I have no idea if there's any legal issues here or whether it will blow up in their faces down the road, but it's certainly a bold step.

Cost and Quality of Care Data Collection. At the request of HCA or the Exchange, for monitoring, enforcement, or program and quality improvement activities, a public option plan must provide cost and quality of care information and data to HCA and the Exchange, and may not enter into an agreement with a provider or third party that would restrict the provision of this data. All submitted data is exempt from public disclosure.

Standardized and Non-Standardized Plans. Any carrier offering a QHP on the Exchange must offer the silver and gold standardized plans designed by the Exchange and if a carrier offers a bronze plan, it must offer the bronze standardized plans designed by the Exchange.

Beginning January 1, 2023, a health plan offering a standardized health plan on the Exchange may also offer up to one non-standardized bronze, silver, and gold plan.

Appropriation: The bill contains a section or sections to limit implementation to the availability of amounts appropriated for that specific purpose.

I'm all for expanding the use of standardized plans...I'm not in favor of continuing to allow non-standardized plans, however, since that kind of defeats the point of...standardized plans. Still, it's a step forward.

Here's the archived video of the first state legislative hearing on the bill. It'll be interesting to see whether this bill makes it all the way through to the Governor's desk, and how much it gets changed along the way. In addition, of course, if #HR269 (the federal bill to #KillTheCliff & #UpTheSubs) goes through, that could impact the "up to 500% FPL subsidy enhancement" portion considerably, though it would probably just be redirected towards cost sharing instead.

Advertisement