Kansas GOP rewards Dem Gov. Kelly for reluctantly allowing discriminatory health plans by...trying to strip her of power.

Tue, 04/23/2019 - 2:36pm

(sigh) I wrote about "Farm Bureau Plans" several times last year. They've been widespread in Tennessee for a long time, and are a big part of the reason for the state's high ACA premiums (TN doesn't have the highest premiums, but they're definitely near the top of the list). Here's the description of typical Tennessee "Farm Bureau" plans:

Traditional plans require medical underwriting that may affect eligibility and rates. Medical information will be requested for any person over the age of 40 and children 25 months and under; medical records may also be requested if any health condition on the application is marked “yes.” Any fees for obtaining medical information will be at the applicant’s expense.

Underwriting guidelines regarding particular conditions may necessitate a benefit exclusion rider, a member exclusion rider or an adjusted rate for coverage. There will be a 6-month or 12-month waiting period for pre-existing conditions, depending upon the plan chosen.

Yeah, that's right: These are the exact same policies which used to be sold on the individual market before the Affordable Care Act: They ask a bunch of nosey questions about your medical history and health status, they can make you wait up to a year before your policy kicks in, they can charge you a ton extra if they come up with anything they don't like, and yes, you have to do all the legwork and pay for getting all the records they want together.

Around 170,000 Tennesseans are enrolled in Farm Bureau plans which not only don't include any ACA protections, compared to around 220,000 in ACA exchange policies. Since you have to be fairly healthy in order to qualify for a reasonably-priced Farm Bureau plan, of course this means that they cherry-pick the healthier people, leaving the sicker, more expensive folks to enroll in ACA exchange plans...thus driving premiums and deductibles up in the ACA risk pool. It's similar to the #ShortAssPlans phenomenon.

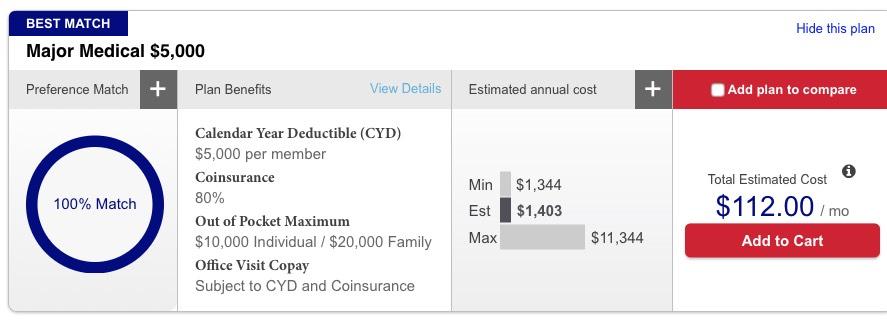

To get an idea of how much of a difference being able to discriminate against people with pre-existing conditions can make, here's a couple of sample plans from for a single 48-year old man living in Adams, Tennessee.

Here's a typical Farm Bureau plan. Remember, this assumes they allow me to enroll at all and don't require a condition exclusion rider or jack up my rates due to my medical condition:

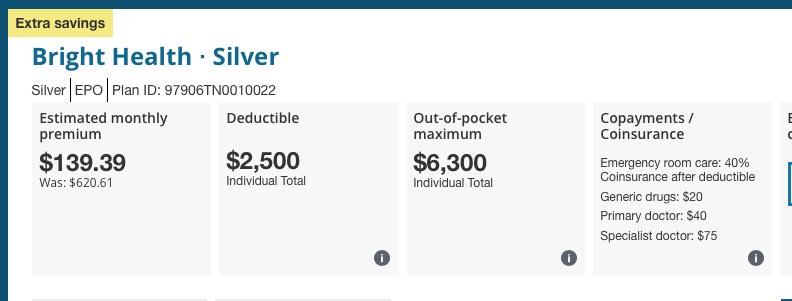

Next, here's what the least-expensive Silver plan would cost if the 48-year old single adult earned $25,000/year, or roughly 200% of the poverty line:

At $25K income, the ACA plan looks like a bargain! The premiums are $27 more per month ($324 more for the year), but the deductible is half as much, and the out-of-pocket maximum is a lot lower as well!

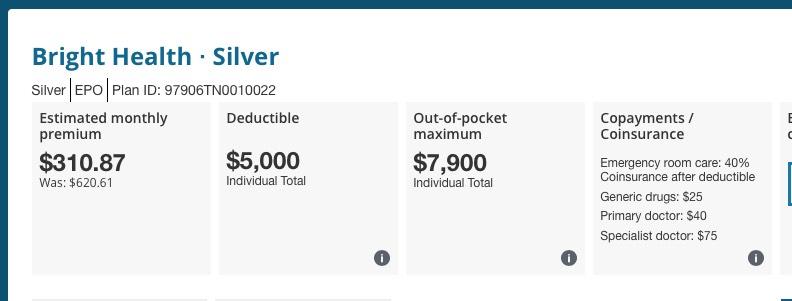

How about if the same 48-year old earns $38,000/year (around 300% FPL)?

At $38K you begin to see the problem. The deductible is identical, while the out of pocket maximum is still quite $2,100 lower...but premiums are now 2.7x as much.

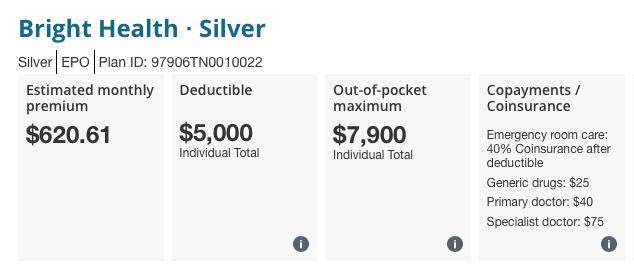

It's once you pass the 400% FPL subsidy eligibility cut-off point that you see the real problem, however:

Ouch. At $50,000 or higher, the 48-year old would have to pay 5.5x as much for a policy with the same deductible (still a $2,100 lower maximum out of pocket cost, however).

If the House Democrats' ACA 2.0 bill were to become law, of course, this wouldn't be nearly as much of a problem, since his premiums would drop to $269/mo at $38K and $354/mo at $50K. He might still go for the Farm Bureau plan (premiums would still be $1,900 or $2,900 more, but the maximum OOP would be $2,100 less and the peace of mind of not being subject to nosey questions or exclusion riders would likely make it worth it).

Unfortunately, ACA 2.0 isn't a thing yet...so this is what Tennessee does instead.

Last spring, Iowa decided to jump onboard the Farm Bureau Express as well.

Last summer, North Carolina Republicans tried to do the same thing, although I'm not sure if it ever actually went through.

And this week, in Kansas, newly-elected Democratic Governor Laura Kelly had little choice but to watch as the Sunflower State pushed a similar Farm Bureau bill into law:

Democratic Gov. Laura Kelly said Friday the bill granting Kansas Farm Bureau authority to sell health coverage exempted from state and federal regulation would become state law without her signature and linked the gesture to her desire for passage of a Medicaid expansion bill.

Kelly’s options were to veto, sign or permit the controversial bill to be enacted in accordance with wishes of the 2019 Legislature. The law allows the politically influential farm organization to market health policies that would fall short of federal standards of the Affordable Care Act. It wouldn’t be regulated by the Kansas insurance commissioner because the statute technically defined the coverage as something other than insurance.

Before anyone judges her too harshly for not vetoing it, however, it's important to note that...

House Bill 2209 passed 84-39 in the House and 28-12 in the Senate -- both veto-proof majorities -- at behest of GOP leadership.

Kelly isn't happy about the situation:

“After long and careful deliberation – including in-depth discussions with both opponents and proponents -- I continue to harbor serious reservations about this legislation,” Kelly said. “I believe it is fundamentally wrong to deny health coverage to anyone because they have a pre-existing condition. I also fundamentally believe that governing demands a relentless pursuit of common ground.”

She's trying to get Medicaid expansion in return for the discriminatory plans which aren't even regulated as insurance...

The governor said the 2019 Legislature, blocked at this juncture by Senate Republicans, ought to approve a Medicaid expansion bill capable of delivering quality health coverage to 150,000 Kansans. Under the ACA, the federal government would pay 90 percent of expansion costs.

...but we're still talking about Trump era Republicans here, so naturally...

Farm Bureau said the nonprofit organization could sell coverage to as many as 42,000 Kansas individuals and families at a lower cost if not bound to mandates requiring insurance providers include expensive treatments and procedures. The bill patterned after laws in Tennessee and Iowa earned support from rural legislators aware of unmet demand for health care as well as urban lawmakers opposed to the ACA.

...The Senate rejected a Medicaid expansion amendment to the Farm Bureau bill.

Oh yeah, and as an additional "f*ck you" to Kelly:

Democratic Gov. Laura Kelly’s power to fill vacancies in some top state posts would be stripped and given to party leadership under new legislation introduced in the House.

Under the state Constitution, the governor holds the power to appoint a replacement if the office of the attorney general or secretary of state becomes vacant. HCR 5013, however, would allow the legislature to move that power to party delegates. The system would work much in the same way legislative vacancies are filled now, Rep. Blake Carpenter, R-Derby, said.

“More or less we’re just modeling the appointment process after how we appoint legislators,” Carpenter said.

The appointment power would fall to the delegates of whichever party last held the executive office. For example, if Attorney General Derek Schmidt, a Republican, were to leave, it would be up to to the Republican party to choose a replacement.

It “allows both parties to have a fair shake,” Carpenter said.

Something tells me that if & when the next Republican Governor and a Democratic AG or SoS are elected, the GOP-held legislature will suddenly change their minds and reverse course on this policy.

A second bill, HB 2410, would remove the governor’s power to fill vacancies in the offices of the state treasurer and insurance commissioner. The bill was requested for introduction on March 25, also by Carpenter.

The legislation may be a sign that Republicans are expecting top leaders to depart before their terms end in 2022. State Treasurer Jake LaTurner has already announced his candidacy for U.S. Sen. Pat Roberts’ seat in 2020. Earlier this year, Attorney General Derek Schmidt expressed also expressed interest in running for the senate.

Imagine that.

Advertisement