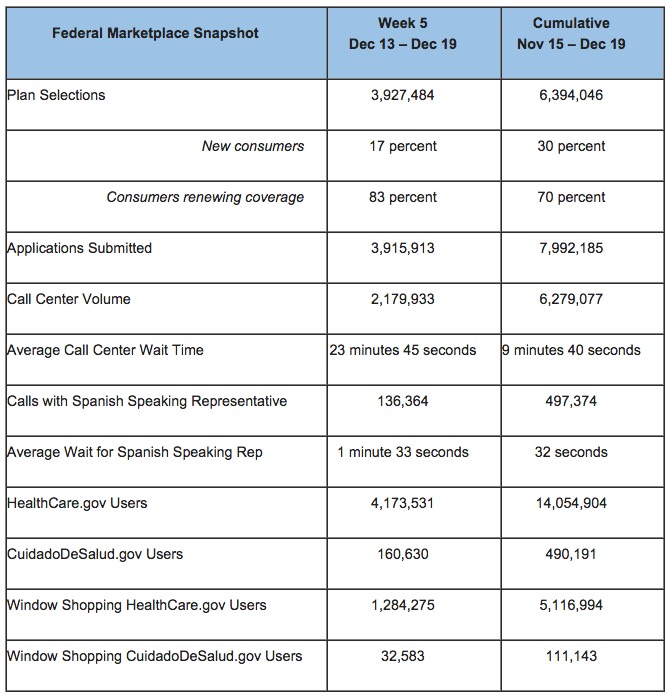

Today should be a big day in ACA enrollment news. It's the deadline for January enrollment in 2 more states (Massachusetts and Washington State). More to the point, the HHS Dept. is expected to release their 5th weekly "snapshot" report. This should be a big one, since it runs through 12/19, meaning it includes the big December 15th deadline which impacted all 37 states being run through HC.gov this year.

I don't know whether they'll just give the weekly numbers (through Friday the 19th) or if they'll also give a 12/15 number (remember, either one would be for HC.gov only, not including the 14 state-based exchanges).

I also don't know how they plan on reporting the millions of autorenewals which should have kicked in on Tuesday the 16th. If the snapshot runs through the 19th, they may be included in the "snapshot" total. Then again, they may be listed separately, or not at all. For all I know, some will be included but not others (it's possible that they've only processed a portion of them).

PROVIDENCE, R.I. (AP) — Rhode Island's health insurance exchange is extending the deadline for residents hoping to sign up for coverage beginning on Jan. 1.

HealthSource RI announced on Monday that people who can't meet the original Tuesday deadline will now have until Dec. 31 to enroll. They must also pay the first month's premium by Jan. 15.

There's a catch, however:

HealthSource officials caution, however, that customers who enroll after Dec. 23 may not receive their insurance cards or have active coverage on the first of the year. That could mean having to pay upfront for any care they receive during the gap and be reimbursed by their insurer after submitting receipts.

Individuals can choose health plans and enroll for coverage through the HealthSource website. They can also call or visit walk-in centers in Providence or Warwick between 8 a.m. and 9 p.m.

That makes 4 states pushing things out until New Year's Eve: Vermont, Minnesota, Hawaii and now Rhode Island.

When we last checked in on New York State, they had added a total of 195,000 new people since November 15th in addition to those already enrolled for 2014. This broke out to around 126.6K added to Medicaid and 68.4K set up for 2015 private policies.

NY's enrollment deadline for January QHP coverage ended on Saturday, and they've just come out with an updated total. Again, this does not include renewals of current enrollees:

NY up to 225,244, enrollment, not counting renewals @charles_gaba hopefully medicaid /qhp breakdown soon

Again, no breakout yet; that usually shows up within an hour or so of the initial total, based on Dan Goldberg's past scoops. Assuming it's roughly a 65/35 split like the prior total was, that should mean roughly 79,000 private policies and 146,000 Medicaid/CHIP.

I'll update this with more details as they come out...

On Friday I discovered that my estimate of roughly 60% of Massachusetts "determined eligible for QHPs" actually selecting a plan was way too high; the actual ratio was closer to 48% overall, meaning that my prior estimate of about 62K QHP selections was too high; the actual number was 53,490 as of Thursday the 18th, which is still excellent, just not as great as I thought it was.

Today I received confirmation directly from the exchange that total enrollments (ie, selected plans) are up to 61,470 as of this morning, which means that the ratio is indeed starting to move up, just later and not as quickly as I had thought (61,470 / 124,403 QHP determinations is just shy of 50%).

I haven't written much about the recent announcement by Vermont's governor that after years of pushing a single payer plan for the state, he's basically pulled the plug on it (at least for the time being). I noted the announcement but didn't have much to add myself.

Part of this is because I'm swamped with the actual ACA open enrollment itself, of course. Part of it is because it's too depressing a development for me to really think about right now. Part of it is because others far more knowledgeable than I am have much more to say about it.

One such person is Vox's Sarah Kliff, and she's written a fairly definitive explanation of what went wrong. The short version: Vermont's tax base is too small to support the initial costs, even if it would save gobs of money in the longer term.

In Vermont, this is massive: the state only raises $2.7 billion in taxes a year for every program it funds. Early estimates said that Vermont's single-payer plan might need $1.6 billion in additional funds — a huge lift. But $2.5 billion was impossible.

Way back in July, when the Halbig v. Burwell case was on the media radar, I wrote about the potential backlash against Republican governors/legislators who failed to take any action towards establishing a state-based exchange to salvage the tax credits for tens or hundreds of thousands of their own residents. At the time, I speculated that doing so could be as simple as slapping up a simple splashpage & redirect to HC.gov, which I termed the "Grand Slam Solution" (ie, "for less than the cost of a Denny's Grand Slam breakfast...")

...the "domain solution" I describe above would still have one more hurdle, of course: You'd still have to get the individual states to agree to pony up $9.95 per year and set up a simple domain redirect. Illinois has already done so; presumably other blue-leaning states would follow. That would leave about 30 states, give or take, including Texas, Florida and so forth.

One persistent Obamacare fear, for years now, has been that the new law would decimate the employer-sponsored insurance system. Why would companies waste money on buying coverage for their workers, the argument goes, when they could hand these people off to Obamacare's new exchanges?

And some high profile companies like Walmart went through and did this, leading to much speculation about whether Obamacare would kill employer-sponsored coverage.

New research from the Urban Institute suggests that, at least in year one, companies like Walmart were the exception rather than the norm: employer-sponsored coverage held steady through the Affordable Care Act's launch.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}