One of the most surreal & ironic #MAGAMurderBill provisions would harm ~18x as many red state enrollees as those in blue states

Fri, 06/06/2025 - 10:54am

A couple of days ago I took a look at the letter sent by the Congressional Budget Office (CBO) to Democratic ranking committee members which broke out the ~16 million Americans expected to lose healthcare coverage via the #MAGAMurderBill passed by House Republicans, assuming they also fail to extend the IRA tax credits beyond the end of 2025.

There was a lot to unpack there, all of it pretty horrible...but I felt one provision in particular was worth its own separate post:

Funding Cost-Sharing Reductions.

Enacting section 44202 would affect the cost-sharing reductions that the ACA requires insurers to offer to eligible people who purchase silver plans through the marketplaces. Those reductions increase the actuarial value—the average share of covered medical expenses paid by the insurer—above the amount in other silver plans, resulting in lower out-of-pocket costs for eligible enrollees. To be eligible for cost-sharing reductions an enrollee’s income must generally fall between 100 percent and 250 percent of the FPL; the subsidy varies with income.

Before October 12, 2017, the federal government reimbursed insurers for the cost of those reductions through direct payments. After that date, the Administration announced that it would no longer make payments to insurers unless an appropriation was made for that purpose. Because insurers still must offer cost-sharing reductions, and they bear that cost even without a direct payment from the government, most cover the costs by increasing premiums for silver plans offered through the marketplaces. That practice, called silver loading, results in a larger premium tax credit because the credit is tied to the second-lowest-cost silver plan. The credit covers a greater share of premiums for non-silver plans and, in CBO’s estimation, primarily increases enrollment among people with income between 200 percent and 400 percent of the FPL.

I've written about Silver Loading many, many times over the past 7 years or so; here's my latest explainer which ties in with the current #OneBigUglyBill.

The CSR/Silver Loading saga is absurdly complicated and fairly stupid at some points, but the bottom line is this:

- In 2014, the House GOP sued to cut off CSR payments, while the Obama Admin defended them.

- The GOP won, and in late 2017, Trump cut off CSR payments, thinking doing so would damage the ACA

- However, regulators & insurance carriers managed to make lemonade out of lemons by "Silver Loading" CSR costs instead

- As a result, instead of harming the ACA, Silver Loading strengthened it by boosting premium tax credits for millions of enrollees

- Silver Loading has since become the norm for most carriers in most states (to varying degrees)

- In an ironic twist, the House GOP is now trying to reinstate CSR payments, which would end Silver Loading, in order to reduce premium tax credits and in the process...damage the ACA.

Basically, if the budget bill is implemented as passed by the House GOP, it would cause gross premiums to drop significantly for Silver plans...but net premiums (what enrollees actually pay) would increase dramatically for anyone enrolled in a Bronze, Gold or Platinum plan (which is basically the 6 million exchange enrollees who earn between 200-400% FPL).

HOWEVER, there's yet another very surreal & ironic twist included in the bill, which my friend Louise Norris first called to my attention:

Section 44202 would appropriate funds for cost-sharing reduction payments and only allow those payments for plans that limit any coverage of abortion services to when it is necessary to save the life of the mother or the pregnancy is a result of rape or incest. Silver loading would end if insurers were compensated for cost-sharing reductions through an appropriation, thereby reducing gross premiums for silver plans and reducing the premium tax credit.

In the absence of silver loading, CBO projects, there would be declines in enrollment primarily among people whose income is between 200 percent and 400 percent of the FPL because of the smaller subsidy available to them.

CBO estimates that enacting section 44202 would result in roughly 75 percent of marketplace enrollees living in states where silver loading would end. Because some states mandate coverage of certain abortion services, and marketplace plans still must offer cost-sharing reductions, CBO projects that the other 25 percent of enrollees would live in states where silver loading would continue, consistent with current practices.

In other words, Silver Loading would continue in states which mandate abortion coverage by ACA exchange plans.

And which states would that be?

- California

- Colorado

- Illinois

- Maine

- Maryland

- Massachusetts

- Minnesota

- New Jersey

- New York

- Oregon

- Vermont

- Washington

That's right: Most of the blue states are actually the ones which wouldn't be harmed by this particular provision, while every red & purple state (plus some blue ones) would be hit by it. Surreal, but here we are.

If you're wondering why in the world House Republicans would deliberately include a provision which spares enrollees in blue states only from one of their pieces of sabotage, I can only assume it's because they're more obsessed with making sure federal dollars aren't spent on abortion. It's a weird sort of logic but I suppose it makes sense if looked at through a GOP lens.

In any event, if this were to happen....

All told, CBO estimates, enacting section 44202 would increase the number of people without health insurance by 300,000 in 2034.

...none of whom would live in any of the 12 states above, although millions of people would still lose coverage in those states due to the other provisions included in the House GOP bill.

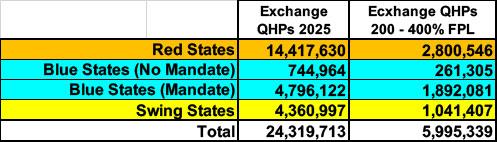

Out of ~24.3 million total exchange enrollees this year, around 4.8 million live in the 12 states above and would therefore presumably still continue to benefit from Silver Loading.

Of the remaining ~19.5 million, only ~815,000 live in the remaining blue states (CT, DE, DC, HI, NH, NM, RI & VA)...while over 14.3 million live in red states, or a whopping 17.6x as many.

The remaining 4.36 million live in the 7 swing states (AZ, GA, MI, NV, NC, PA & WI).

If you take the CBO's projections literally, the breakout of those losing coverage due to this specific provision would be roughly 74% in red states, 4% in blue states & 22% in swing states.

UPDATE: OK, I've re-run the numbers, and it looks like it's actually more like 19.3x as many in the Red States (14.4 million) vs. the Blue States (only ~745,000 living in states w/out an abortion coverage mandate).

On the other hand, if you only look at 2025 exchange enrollees who earn 200-400% FPL (which should comprise the vast majority of enrollees who will be hurt by Silver Loading being terminated), the ratio is lower...more like 10.7x as many (2.8M vs. 261K).

Assuming you take the CBO's 300K total literally, it would be something like ~205,000 losing coverage in red states, ~19,000 in blue states and ~76,000 in swing states.

The obvious play for the rest of the blue states is to codify abortion coverage into law ASAP, of course (which they should do anyway), but something tells me this particular provision isn't gonna make it into the final version of any bill that passes (or if it does, Trump will try to kill Silver Loading in the remaining states via regulatory action instead).

Advertisement