West Virginia: *Final* avg. 2020 #ACA premiums: 6.7% increase...for the highest premiums in the country

Thu, 10/31/2019 - 1:52pm

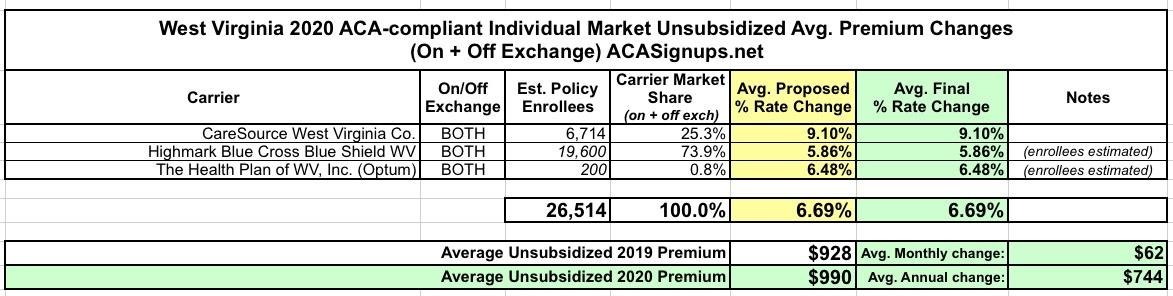

There are three insurance carriers offering ACA-compliant individual market plans in West Virginia: CareSource, Highmark BCBS and Optum, although Optum has barely any enrollees at all, and the other two combined only total around 26,000 people in the state.

The final, approved average unsubsdized premiums for 2020 haven't changed from the requested rates--the weighted statewide average is a 6.7% increase.

Nothing terribly noteworthy about any of this, except that with that 6.7% increase, West Virginia has just taken the title for Most Expensive Obamacare Premiums in the Country, with average premiums averaging $990/month per enrollee, or nearly $12,000/year apiece.

This record was held by Wyoming last year (prior to that I believe Alaska had by far the highest rates in the country, until they instituted their ACA reinsurance waiver a few years back, which reduced full-price premiums by a good 25% or so).

It's important to understand that West Virginia has taken pretty much no actions whatsoever to tackle this problem.

- Back in 2014 they simultaneously did and didn't choose to allow insurance carriers to offer transitional plans, which hurt the ACA-compliant risk pool...but then decided to sue the federal government for allowing them to make this decision on their own.

- Unlike a dozen other states, West Virginia has not, as of yet, even started the process of submitting an ACA Section 1332 waiver to reduce unsubsidized premiums. Granted, reinsurance also has the downside of reducing APTC assistance for subsidized enrollees, so it's possible they decided to leave it alone for now.

- Finally, and most perplexingly, West Virginia remains one of just three states (along with Indiana and Mississippi) which has refused to institute Silver Loading for 2020, as Kelly Allen of the West Virginia Center on Budget & Policy wrote about the other day:

Marketplace plans cost thousands of West Virginia residents more than they should because our state is one of only three states where insurers aren’t using a technique called “silver loading” when calculating their premiums. For 2020 health plans, affected West Virginia consumers across the state could have saved thousands of dollars if the state had allowed insurers to utilize silver loading.

Again, as a quick refresher:

- ACA premium subsidies are based on the cost of the 2nd lowest-cost silver plan available in the area (the "benchmark plan")

- As benchmark premiums increase, so do ACA subsidies

- Normally, if premiums increase by roughly the same percentage for every metal level (Bronze, Silver, Gold, Platinum), the subsidy increase doesn't make that much difference one way or another, since it just rises to match the trend

- However, in 2017, Donald Trump cut off CSR reimbursement payments in a failed attempt to "blow up" the ACA exchanges

- In response, carriers in most states instituted a pricing strategy called "Silver Loading" in which they add the cost of the lost CSR payments to Silver premiums only...without raising prices on other metal levels to account for the CSR losses

- This caused Silver premiums...including the benchmark plan...to increase substantially more than Bronze or Gold plans in most areas

- This in turn caused ACA subsidies to increase dramatically...which could then be applied to Bronze or Gold plans instead

- That, in turn, has led to far lower net premiums for several million ACA exchange enrollees nationwide

In 2018, about half the states instituted Silver Loading. By 2019 this had spread to almost all of them. For 2020, every state except Mississippi, Indiana and West Virginia are doing so. What are they doing instead? "Broad Loading":

In response, most states allowed or required insurers to silver load, which means they built the cost of CSRs into silver plan premiums only. But six states, including West Virginia, required insurers to “broad load,” meaning they built CSR costs into premiums for all metal levels. Since then, three more states shifted from broad loading to silver loading. But not West Virginia.

While enrollment in the ACA’s marketplaces declined by nine percent nationally between 2017 and 2019, West Virginia’s Marketplace saw a much larger drop of 34 percent, the second-highest decline in the nation. Silver loading has driven a significant drop in the premiums that subsidy-eligible enrollees pay in most states, but in West Virginia net premiums for this population have increased by 16 percent, the largest increase in the country.

There is a potential downside to Silver Loading for unsubsidized enrollees, of course...but only if they're enrolled in Silver plans. They can avoid the CSR hit by either switching to Bronze or Gold plans as well or (in many states) by enrolling in a "mirrored Silver" plan off-exchange (this gets into something called the "Silver Switcharoo", which I wrote about two years ago). According to Allen, however, there's been minimal downside to silver loading in other states, while broad loading in WV has led to substantial harm to unsubsidized enrollees as well as those who are subsidized.

Advertisement