OK, everyone, it's time to revisit the House and Senate ACA 2.0 bills again...

Wed, 08/21/2019 - 11:11am

If you've been following me on Twitter lately, you know that I've grown increasingly frustrated with two aspects of the Democratic Presidential primary process in recent months:

- First, Sen. Elizabeth Warren's seeming 180-degree turnaround from her March stance on achieving universal healthcare coverage ("a lot of different pathways") to her more recent rhetoric (a simple, point-blank "I'm with Bernie on Medicare for All.") at the first debate in late June. At the time, I assumed this was simply due to the absurdly short time constraints and the terrible framing of the question by the moderators, but it's mid-August now and so far she seems to be sticking to her guns re. being 100% onboard with BernieCare.

- Second, the almost complete ghosting of the dangers to and fixes needed for the the ACA itself regardless of what the Next Big Thing ends up being (whether Medicare for All, Medicare for America, Choose Medicare, Medicare X, etc).

The only one to even mention the Texas vs. Azar (#TexasFoldEm) lawsuit during any of the four debates held to date was Sen. Cory Booker...and the only major candidate who's focused on improving the ACA specifically has been Joe Biden...and even his plan would also include the creation of a federal public option which would complicate and delay the implementation of the other provisions of his plan nearly as much as the other overhaul bills on the table, as David Anderson notes:

Let’s work our way through the process of a major revamp first and then a minor revamp....

...Any major revision of the US Healthcare system will need significant rule making from federal agencies. The federal agencies need to take what Congress has written and figure out how to actually make it work. The ACA had several hundred instructions of the “Secretary Shall…” and those ranged from when open enrollment periods should be, to how calories were to be counted, and what the de minimas allowable actuarial variation in metal bands could be. Rule making (at least rule making that will stand up in court) requires notice and comment. Let’s be super-optimistic and say the major rules are drafted in six months.

...This learning process will take another four to six months to produce a final rule that is neither arbitrary nor capricious.

...A major change like Medicare for All or dedicated Health Savings Accounts and high deductible plans for everyone requires massive back-end changes. Industry scopes out the changes and figure that it is a twelve to eighteen month project.

...So the nerds start programming and the consultants start consulting on change management. We are two years in.

...So now we’re 30-36 months in and the government and industry are about ready to go live. Day 1, depending on how ambitious your favorite bill is, could see millions to tens of millions to hundreds of millions of people trying to figure out the new system. It better be mechanically sound on Day 1, so the temptation to pad another six to twelve months of plumbing time into the project timeline is strongly motivated.

Anderson's point (and mine for some time now) is that even if you assume the Major Overhaul Bill (Medicare for All, Medicare for America or similar) itself actually passes the House, passes the Senate (presumably after the filibuster has been eliminated) and is signed into law by the newly-elected Democratic President sometime in early 2021, you're still likely looking at an actual start date of no earlier than January 1, 2024 under the most optimistic of circumstances...

...and that doesn't even include the 2-5 year ramping-up period (depending on whether it's the House Med4All, Senate Med4All or Med4America bill which gets passed), during which large portions of the population would still be enrolled under the existing ACA framework. All three bills do include some transition period improvements, so it's a matter of perspective as to whether those 2-5 years should "count" or not.

In short, even under a perfect, utopian, Progressive Blue Trifecta Med4All scenario, the ACA framework as it stands now will still be with us (if it isn't stricken down altogether by the Texas lawsuit) for at least the next 5 - 9 years. And it desperately needs to be shored up for that timeframe.

Many of the improvements were already needed even before Trump took office in 2017. Trump/GOP sabotage of the ACA didn't create all of its problems; it simply worsened them. Today, Larry Levitt of the Kaiser Family Foundation addressed this head on:

A good question for Democratic presidential candidates (and President Trump): What's your plan to address the more than 3 million middle-class people not eligible for ACA subsidies who have lost individual insurance coverage since 2016?

https://t.co/qMLZhwnamR pic.twitter.com/rGsCfWlOig

— Larry Levitt (@larry_levitt) August 21, 2019

Brief ACA timeline:

2014-2016: Enrollment up with subsidies, no pre-existing condition limits. Insurers lose $.

2017: Premiums up to match costs.

2018: Trump cuts outreach and cost-sharing $. Premiums up with uncertainty.

2019: Individual mandate gone, short-term plans expanded.— Larry Levitt (@larry_levitt) August 21, 2019

There are 3 big holes in the ACA right now:

1. Unaffordable coverage for middle-class people who don't qualify for subsidies.

2. No access to coverage for poor people in states that haven't expanded Medicaid.

3. The "family glitch" for spouses and children of low-income workers.— Larry Levitt (@larry_levitt) August 21, 2019

The debate in the Democratic primary right now is whether to plug the holes in the ACA (some of which were put there or widened by the Trump administration), or abandon that effort for Medicare for all. Some candidates argue for both, playing the short and long games.

— Larry Levitt (@larry_levitt) August 21, 2019

Of course Larry's first question is rhetorical; as a top healthcare policy wonk at a top healthcare policy research organization, he knows that there are robust ACA 2.0 bills which have been introduced by Democrats in both the House and the Senate. In fact, several smaller standalone provisions of this have already passed the House with others in the hopper.

Now let's look at what Anderson says about smaller-ball fixes:

A change to the ACA subsidy formula so that no one pays more than 10% of income for a silver plan can’t go live on January 1, 2020 as insurers are just about ready to submit final plans for approval next month. But the rule making would come out via the routine Notice of Benefit and Payment Parameters in December and the plumbing would not be particularly complex. These plans would definitely be available for the November 2020 open enrollment period with a go live date of January 1, 2021.

Moving Medicare’s age eligibility date up or down a year or two is also mechanically simple.

Changing Medicaid eligibility and financing so that the enhanced match rate applies to all mandatory populations or only to the new ACA populations but changing that guideline so it is now 167% FPL instead of 138% FPL is also fairly simple. That is something that could readily go live at some point in 2020. Creating well funded high cost reinsurance pools would also be a 2020 project.

I've written about both ACA 2.0 bills several times before, but it seems like a good time to revisit them...especially given that several candidates seem to be backing off their "BernieCare-or-Bust" stance:

Sen. Kamala Harris recently ignited another round of controversy on her healthcare position when she distanced herself from the Medicare for All bill that Sen. Bernie Sanderspushed in the Senate — two years after she became its first cosponsor.

In remarks this weekend to wealthy donors at a Hamptons fundraiser, Harris said she has "not been comfortable" with the Sanders proposal, the Daily Beast first reported. Then the California senator told the Washington Post she didn't think her discomfort "was any secret."

Insider reached out to each of the four Sanders bill co-sponsors running for the presidency: Harris, and Sens. Elizabeth Warren, Cory Booker and Kirsten Gillibrand. The Warren, Harris, and Gillibrand campaigns did not respond to requests for comment asking if they stood by the Sanders bill.

Harris has already clarified her split from Sanders, so I'm not sure why they wouldn't comment (nor why they asked in the first place, actually). Gillibrand and Booker seem to be mostly irrelevant at the moment given their anemic polling numbers. That leaves Warren, who's considered one of the top contenders for the nomination...and her campaign's refusal to respond to this question goes back to the crux of my first point above.

All this being said, let's take another look at the ACA 2.0 bills in both the House (which lists Rep. Frank Pallone as the lead sponsor and has 159 consponsors) and the Senate (which was introduced by...wait for it...Elizabeth Warren, and currently has six cosponsors...including, yes, Sen. Gillibrand, Booker, Harris and Klobuchar). Also worth noting: Bernie Sanders also cosponsored the Senate bill last year...yet stripped his name off of it this spring (as did Sen. Maggie Hassan for reasons unknown).

I should also note that the House version (H.R. 1884) has also been broken up into about a dozen smaller, standalone provisions, several of which have already passed the House and are waiting for action in the Senate (not that Mitch McConnell will ever allow that to happen as long as he's Majority Leader).

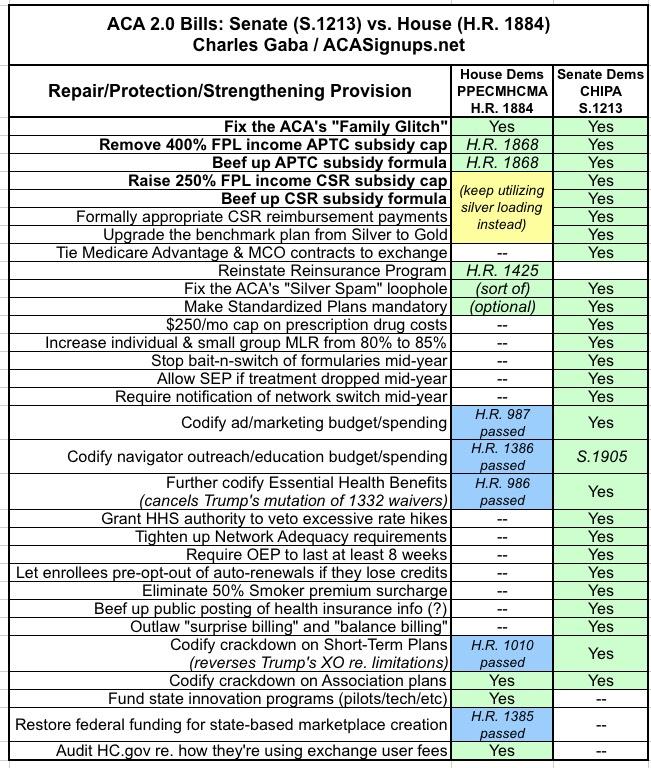

There's a lot of overlap between the two bills as you would expect...but there are also some differences:

- BOTH BILLS would #KillTheCliff by removing the upper-end 400% FPL income subsidy eligibilty cut-off for ACA exchange policies.

- BOTH BILLS would also kill the lower-bound cliff by changing the 100-133% premium cap from a flat 2% to a 0 - 1% range.

- BOTH BILLS would make the subsidies formula more generous by reducing the scale from 2 - 10% down to 0 - 8.5% of income.

- BOTH BILLS would fix the so-called "Family Glitch" which currently prevents several million people from being subsidy-eligible due to a single family member being eligible for employer-sponsored coverage

- BOTH BILLS would either partly or fully fix the "Silver Spam" problem which currently allows carriers to flood the exchanges with multiple near-identical plans to game the benchmark plan scoring and confuses enrollees, as well as standardizing plans at the different metal levels to reduce confusion further

- BOTH BILLS would restore and codify HealthCare.Gov's marketing and outreach budgets, reversing Trump Admin sabotage

- BOTH BILLS would restore and codify HealthCare.Gov's navigator/education budgets, reversing Trump Admin sabotage

- BOTH BILLS would restore and codify Essential Health Benefit requirements, reversing Trump Admin sabotage

- BOTH BILLS would crack down and codify restrictions on non-ACA compliant Short-Term Plans, reversing Trump Admin sabotage

- BOTH BILLS would crack down and codify restrictions on quasi-ACA compliant Association Health Plans, reversing Trump Admin sabotage

IN ADDITION, the House version would also do the following:

- Reinstate the federal reinsurance program (which originally sunsetted at the end of 2016) with $10 billion/year in funding. This would single-handedly reduce unsubsidized premiums by around 10% per year.

- Provide federal funding for state innovation programs

- Restore federal funding for states to create their own ACA exchanges (several are already doing so now; this would provide another $200 million in federal funding to encourage even more to do so...the ACA originally included funding for this but that ran out years ago), and...

- Audit HealthCare.Gov to see how they're using ACA exchange carrier user fees

IN ADDITION, the Senate version would also do the following:

- Upgrade the benchmark ACA exchange plan from Silver to Gold

- Raise the income threshold for Cost Sharing Reduction (CSR) assistance from 250% FPL to 400% FPL

- Beef up the underlying CSR formula from 73-94% Actuarial Value up to 85-95% AV

- Formally appropriate the actual CSR funding which was cut off by Trump in the fall of 2017

- Tie Medicare Advantage contracts to ACA exchange participation in low-competition areas

- Impose a $250/month cap on prescription drug costs regardless of the larger maximum out-of-pocket cap

- Increase the Individual and Small Group market Medical Loss Ratio minimums from 80% to 85% (to match the Large Group market)

- Stopping mid-year bait-n-switch of drug formularies as well as allowing a enrollees to change plans if their treatments are dropped by their provider mid-year

- Requiring carriers to notify enrollees of any network changes if they happen mid-year

- Grant HHS further authority over denying excessive rate hikes

- Tighten up network adequacy requirements for carriers

- Require the Open Enrollment Period to last at least eight weeks (vs. the current 7 weeks)

- Allow enrollees to opt-out of being auto-renewed if they would lose tax credit eligibility the following year

- Eliminate the 50% smoker premium surcharge currently allowed under the ACA (I was opposed to this until I did some research which showed that it's pretty ineffective anyway), and...

- Outlaw surprise/balance billing

The Cost Sharing Reduction bullets need further clarification. The original House version from 2018 also beefed up and expanded the CSR formula...but due to the #SilverLoading workaround which was put together in response to Trump cutting off CSR reimbursement payments, the House Democrats appear to have decided to cut that out of their version of the bill, presumably deciding to let sleeping dogs lie. Silver loading is a confusing and imperfect way of mitigating the damage done by the CSR cut-off, but it sounds like they've calculated that it would be better not to stir up that particular hornet's nest for the moment.

The Senate version, meanwhile, tackles the issues of CSR/deductibles/out of pocket costs head on by formally restoring CSR payments (which eliminates silver loading) but also beefing up the CSR formula and upgrading the benchmark exchange plan from Silver to Gold anyway. This is a far better solution to the issue, though I understand why the House is wary of touching it under the circumstances.

Here's a table simplifying the differences between the two, including a note about the standalone bills which have already been passed or introduced in the House:

Advertisement