UPDATED: LET'S DIVE IN: Reps. DeLauro & Schakowsky's "Medicare for America"

Tue, 01/22/2019 - 10:22am

UPDATE 4/16/19: Please note that this overview refers to the version of Medicare for America introduced in December 2018. There's a revised version of the bill being re-introduced in the near future which is expected to include several important changes. The only two which have been made public so far are: 1) Deductibles are expected to be eliminated altogether; and 2) the upper-end percent-of-income maximum premium is supposed to drop from 9.69% to an even 9.0%.

There's a half-dozen or more different healthcare policy overhaul bills which are being batted around by Congressional Democrats these days, ranging from the fairly modest ("lower the Medicare buy-in to age 50!") up through the full-blown, "pure" Single Payer bill being pushed by Bernie Sanders & other "Medicare for All" activists.

Nearly a year ago, I wrote a deep dive into another plan being proposed by the Center for American Progress, a leading left-leaning policy think tank. Their plan was rather awkwardly titled "Medicare Extra for All" (MEFA), and it's based in large part on three previous proposals:

- Congressman Pete Stark's "AmeriCare" Health Care Act,

- Institute for Social & Policy Studies Jacob Hacker's "Medicare Part E", and

- Jon Walker of ShadowProof's "Medical Insurance & Care for All" (MICA)

Anyone who read my analysis of CAP's "MEFA" plan knows that I was pretty excited about it. I concluded:

Well, obviously the end result is likely to differ somewhat from what they posted today in quite a few ways, but assuming the plan were to be enacted pretty much as described above...I like it. A lot.

Read my post over at Cracked from last year in which I describe about a half-dozen major headaches/barriers which need to be overcome in order to make any large-scale changes to the U.S. healthcare system. The Center for American Progress Medicare Extra for All proposal tackles most of them, and does so in a way which will piss off the fewest number of people while also being scaled up gradually enough to cause minimal disruption but quickly enough to achieve universal coverage within 8 years of being passed...which is about as quickly as anyone could reasonably expect it to happen in my view.

By an amazing coincidence, 8 years also happens to be the exact length of 2 Presidential terms of office. Even if it were to pass and be signed into law, I don't think CAP expects that to happen any earlier than January 20, 2021, of course...even with a massive Blue Wave in November, you'd still have Donald Trump in the White House (er...Mar a Lago, that is). But assuming we elect a Democratic President in 2020, 8 years is just about the right timeframe.

As much as I like CAP's MEFA proposal, it wasn't an actual Congressional bill--it was basically a white paper (or whatever the appropriate term is).

Well, as it happens, back in December, legislative text was introduced by two Democratic members of Congress (Reps Rosa DeLauro of Connecticut and Jan Schakowsky of Illinois) for a healthcare system overhaul bill which seems to bear more than a small resemblance to CAP's MEFA proposal, called "Medicare for America":

DeLauro, Schakowsky Introduce Medicare for America

December 19, 2018WASHINGTON, DC (December 19, 2018) – Congresswoman Rosa DeLauro (CT-03) and Congresswoman Jan Schakowsky (IL-09) today introduced the Medicare for America Act, a new healthcare bill that would ensure universal, high-quality, affordable health coverage by making Medicare accessible to all Americans and expanding the program’s covered benefits and services. The Medicare for America plan includes coverage for prescription drugs, dental, vision, and hearing services, as well as long-term supports and services for seniors and Americans living with disabilities.

Medicare for America achieves universal coverage while preserving quality employer-sponsored insurance for those who have it and are satisfied. Americans who are uninsured or do not have employer-sponsored insurance—including those on the individual market—would be auto-enrolled into Medicare for America.

This is precisely the point I was making in my MEFA analysis. One of the trickiest parts about trying to overhaul the entire U.S. healthcare system is twofold:

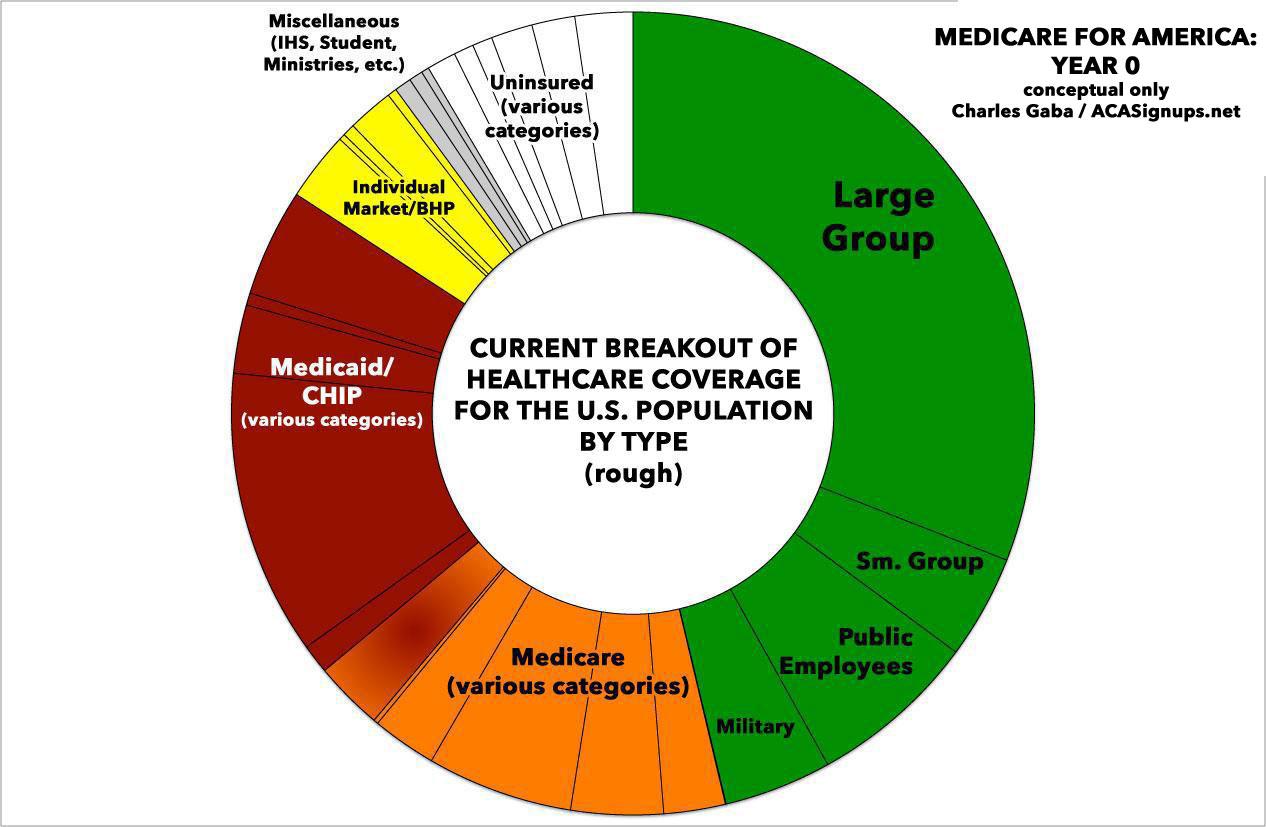

- On the one hand, there's nearly 30 million Americans still uninsured, while another 20 million or so are covered via a hodge-podge of healthcare plans ranging from pretty good (subsidized individual market enrollees) to crap ("short-term plans" and so forth). Pretty much all of these folks would be far better served by being added to a more comprehensive Medicare/Medicaid-style public program with lower out of pocket costs than whatever they're on (or not on) today.

- On the other hand, nearly half the population (around ~160 million or so of us) are covered through our employers...and while plenty of those with employer coverage hate it, polls consistently show that a large majority of them are pretty happy with it (or at least reasonably satisfied, to the point that they aren't willing to let it be torn away and replaced with an all-new, unknown/unproven system, anyway).

The thing about health insurance risk pools is that you need low-cost healthy people enrolled in order to help cover the expenses for high-cost sick people. In order to do this, you have to make participation mandatory to some degree to prevent healthy people from skipping out when they're healthy but gaming the system when they become sick.

On the other hand, people who are satisfied with their current system tend to hate being forced into participating in a Big Government Program (remember the massive backlash over President Obama's "If You Like It You Can Keep It" statement? The ACA only "forced" around 5-6 million people to switch policies, yet the outrage was so fierce and loud that he had to tell his HHS Dept. to issue a 1-year extension of noncompliant plans...which was later bumped out to three years, then four, then five...)

The "Medicare for America" bill, along with the three previous proposals it's modeled after, neatly walks this tightrope by making a vastly improved/enhanced "Medicare" program mandatory for roughly half the country (those least likely to object) but completely optional for the other half (those most likely to object).

“Healthcare affects the lives of every American, yet our current system fails far too many of them each day,” said Congresswoman DeLauro. “From exorbitant premiums and deductibles to skimpy plans that do not cover the essentials, healthcare in America is complex and costly when you need it. Even worse, the gains Americans secured through the Affordable Care Act—such as coverage for those with pre-existing conditions and Medicaid expansion—are under attack from President Trump and Congressional Republicans, who say one thing publicly while they work to dismantle healthcare coverage. This is not the path we should be on.”

“But we cannot just stay on the defensive—people’s lives are at stake,” continued DeLauro. “An individual’s zip code should not determine their benefits, as our current healthcare system is largely a patchwork of what states cover under Medicaid and state mandates for private insurance. That is why we must continue to fight until every American has healthcare coverage they can afford and that meets their needs. Through Medicare for America, we can finally ensure that all Americans have the same robust benefits and services package.”

One of the largest drivers of healthcare costs in the United States is the cost of prescription drugs. Currently, the United States government is banned from negotiating prescription drug prices under Medicare, which keeps prices artificially high for millions of Americans. Medicare for America will finally remove that ban, and if negotiations fail, the Department of Health and Human Services (HHS) will use the prices paid by the Department of Veterans Affairs (VA) or the average price of these drugs in Organization for Economic Co-operation and Development (OECD) nations.

“Every person in America deserves quality, affordable, and comprehensive healthcare,” said Congresswoman Schakowsky. “That is why I am so proud to join Representative DeLauro in introducing Medicare For America. Now more than ever, we must look into every way to address the problems in our healthcare system. This bill goes a long way to strengthen Medicare and provide excellent healthcare to all Americans. As a member of the Medicare for All Caucus, I believe this bill is an important step to expanding coverage to reducing out-of-pocket healthcare costs and covering important services like long-term care and prescription drugs.”

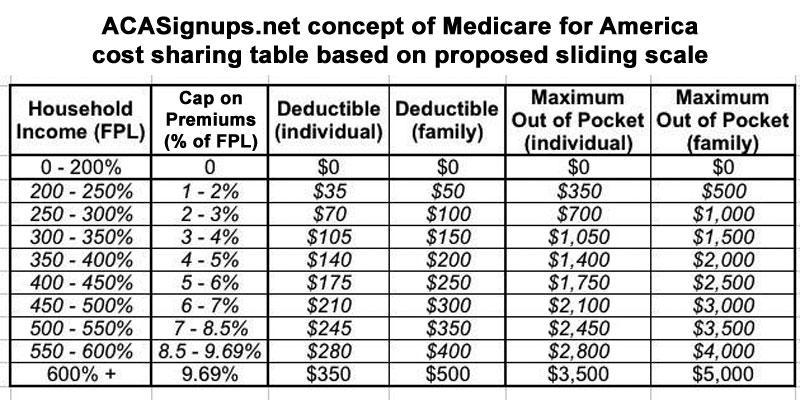

Medicare for America offers a simple, transparent cost structure. Individuals will have a $350 deductible and $3,500 maximum out-of-pocket spending. For households, their deductible will be $500 and $5,000 maximum out-of-pocket spending. Medicare for America also ensures coverage is affordable for all by capping individual and household premiums at 9.69 percent of their monthly income. Individuals or families making less than 200 percent of the Federal Poverty Level will not pay a premium, have to meet a deductible, or have a maximum out-of-pocket spending. Individuals or families between 200 percent and 600 percent of the Federal Poverty Level will receive subsidies to lower their contribution to the premium.

This portion of M4A basically amounts to a massively strengthened ACA:

- Instead of zero-out-of-pocket-cost Medicaid up to 138% FPL...the zero cost threshold is bumped up to 200%.

- Instead of strong subsidies from 138 - 200% FPL, decent subsidies from 200-400% FPL and no subsidies above that...it's strong subsidies from 200-600% and decent subsidies above that.

- One of the most critical points to me (as regular readers know) is that it would cap premiums at no more than 9.69% of income no matter what (which means you'd still receive light subsidies even over the 600% FPL line depending on your age/where you live).

“Medicare for America sets a new standard for universal health care that’s affordable, universal, comprehensive—and possible,” said Jacob S. Hacker, Stanley Resor Professor of Political Science and Director of the Institution for Social and Policy Studies at Yale University. “It not only builds on the best aspects of Medicare; it also improves the program for those now within it so it can be a secure foundation for quality coverage for all Americans for generations to come.”

“Health care is a fundamental human right and the foundation of economic security for all people,” said Neera Tanden, CEO of the Center for American Progress Action Fund. “‘Medicare for America’ is an important contribution to the debate over how to improve our health care system. By making an enhanced Medicare program available to all Americans, ‘Medicare for America’ would guarantee universal health care and dramatically lower out-of-pocket costs. The legislation would ensure that every American, no matter where he or she lives, is no longer subject to Republican sabotage or the whims of insurance companies.”

Obviously neither Hacker nor CAP see Medicare for America (which is gonna cause a great deal of confusion with "Medicare for All" given the "MFA" acronym...) as "co-opting" their proposals; they're fully on board with it. To help distinguish between the two, I'm going to use the hashtag/abbreviation "Med4America" going forward.

Med4America also addresses another important shortcoming in our current healthcare system:

Currently, there is incredibly limited access to long-term supports and supports in Medicare and private insurance, leaving Medicaid to be the primary payer of these services and supports. With an emphasis on home and community-based settings, Medicare for America establishes and guarantees access to long-term support and services.

“The Consortium for Citizens with Disabilities is thankful to Representative DeLauro and Representative Schakowsky for introducing a healthcare reform bill that recognizes that all must mean all, people and services,” said Kim Musheno, Chair of the Consortium for Citizens with Disabilities. “We appreciate that the bill includes a benefit for community-based long term supports and services. These services are imperative for people with disabilities and older adults to live healthy lives in their communities.”

“The Arc is grateful that Representative DeLauro and Representative Schakowsky have included a robust Long Term Supports and Services benefit, with an emphasis on community-based services in this bill,” said Nicole Jorwic, Director of Rights Policy for The Arc of the United States. “It is imperative that any healthcare reform include these services, that are vital to the lives of people with intellectual disabilities and their families.”

Here's the summary version of the bill:

The MEDICARE FOR AMERICA Act of 2018

The Medicare for America Act would establish the Medicare for America (MFA) health program to provide universal, comprehensive, and affordable health coverage to all Americans.

Who Can Join?

Medicare for America achieves universal coverage by enrolling the uninsured, those who purchase their health insurance on the individual market, and those currently on Medicare, Medicaid, and CHIP. Large employers can continue to provide employer-sponsored care, if it is gold-level coverage. Or, they can direct that contribution toward their employee’s MFA premiums. Or, employees will have the option to choose MFA over employer-sponsored coverage.

AGAIN: For the ~47% of the country with employer-based coverage, if it's awesome, you can keep it (assuming your employer chooses to...and that's something every employee is already at the mercy of each year as it is anyway). If it sucks, you can switch over to Med4America. For the ~37% of the country currently on (today's) Medicare or Medicaid, along with the other ~16% or so on the individual market, non-ACA compliant plans or completely uninsured, it's a significant upgrade for them no matter what.

What Does It Cover?

Medicare for America improves on Medicare’s and Medicaid’s benefits: covering prescription drugs, dental, vision, and hearing services. And unlike Medicaid, your zip code does not determine your benefits. Medicare for America also comprehensively covers long-term supports and services for Americans living with disabilities and seniors, which Medicare and private insurance do not. And unlike Medicaid, MFA compensates family caregivers, who play a crucial role in resolving America’s long-term care crisis.

You really couldn't ask for much more in terms of what services it covers.

What Does It Cost Me?

Premiums, to be established by the Secretary, will be no more than 9.69% of individuals’ or households’ monthly income. Current Medicare beneficiaries will pay either Medicare’s premium (how it is presently calculated) or MFA’s, whichever is cheaper. And, individuals and families between 200 and 600 percent of the Federal Poverty Level will receive subsidies. Those below 200 percent will have no premium (or deductible or out of pocket limit). Deductibles for an individual (including seniors and current Medicare beneficiaries) will be $350; $500 for a family (based on a sliding scale for individuals and families between 200 and 600 percent of the Federal Poverty Level). Maximum out of pocket costs for an individual (including seniors and current Medicare beneficiaries) will be $3,500; $5,000 for families (based on a sliding scale for individuals and families between 200 and 600 percent of the Federal Poverty Level). Premiums will vary by family composition, but no individual or family can pay more than 9.69% of monthly income towards their monthly premium.

The payment choice for current Medicare enrollees is critical to ensuring they don't freak out: If they really want to, they can keep their existing payment level/structure.

To be honest, I'm not sure why they're going with precisely 9.69% of income as the premium cap as opposed to a round 9% or 10%...and the "sliding scale" for the 200-600% FPL range isn't specifically stated within the actual legislative text itself. There's several references to:

"a linear sliding scale, in the case of an individual whose household income is at least 200 percent of the poverty line, but not more than 600 percent of the poverty line, with the premiums ranging between the amount determined for individuals described in clause (i) and for individuals described in clause 3 (iii)"

...but I'm not entirely certain what those clauses refer to. I think the scale would be something along the lines of the following:

...which would be a massive improvement over today's ACA formula.

For instance, right now a single 40-year adult earning $30,000/year (247% FPL) has to pay about 8.25% of their income ($2,475/year) for a Silver plan covering 70% of their medical expenses; it would likely have roughly a $6,000 deductible and a $7,900 maximum out of pocket total. Under Med4America, they'd likely pay around 2% of their income ($600/year) for a plan covering well over 90% of their medical expenses; it would likely only have a nominal deductible ($35) and a $350 MOOP.

The maximum amount they'd have to pay total under the worst-case scenario would drop from $10,375 to just $950. And keep in mind that the current scenario assumes that every doctor, hospital and prescription drug they visit/take is in network; under Med4America, they'd never have to worry about whether the doctor, hospital, anesthesiologist or whatever was "in network" since pretty much all of them would be.

For the same single adult, if they earned $60,000 (494% FPL), right now they'd have to pay full price...which would likely be around $7,300/year for the same plan. That's 12.2% of their income...whereas under Med4America (assuming the table above is accurate), they'd only have to pay around 7% of their income ($4,200/year), with a $210 deductible and $2,100 MOOP. That's a $6,300 total worst-case scenario vs. $15,200 today.

What About Employer-Sponsored Insurance (ESI)?

Large employers can continue to provide insurance, if it is gold-level coverage with benefits comparable to MFA. Or, they enroll their employees in MFA and contribute 8% of annual payroll to the Medicare Trust Fund. Employees can choose to enroll in MFA, even if their employer offers qualifying coverage. And in either case, if an employer contributes to MFA in lieu of ESI or an employee chooses MFA over ESI, the employee’s MFA premiums will be based on income. And, they will be eligible for subsidies. The same deductibles and cost-sharing apply for these individuals and households.

THIS is the key to the whole program: Employer-sponsored coverage will continue, but only if it's a comprehensive plan. If it's crap, they have to either upgrade to a comprehensive plan or they can shift their employees over to Med4America and pay a flat 8% payroll tax. Frankly, I'm guessing most employers would prefer to just pay a fee instead of dealing with all the headaches of health insurance anyway (not just the cost, but the administrative overhead/decision-making process, etc etc). And if the employees prefer, they can switch over to MFA regardless of what their employer chooses to do.

What Doctors Can I See?

Doctors who participate in current Medicare remain a participating provider under MFA. The Secretary would establish a process for adding more providers not yet participating in Medicare (e.g. pediatric specialties).

Practically all doctors accept Medicare, so this mostly eliminates the "out of network" issue in one shot.

How Are Doctors Reimbursed?

MFA’s rates for medical providers and services would equal current Medicare rates, while proactively increasing rates for primary care and other mental and behavioral health and cognitive services. Far too many individuals who need care face roadblocks because reimbursement rates are too low. Health coverage serves no one any good if they do not have access to care.

This is gonna cause some doctors/hospitals to be furious...while others will be thrilled. Medicare currently only pays about 80% as much as private insurance, so it's gonna be a 20% pay cut for many providers...but Medicaid only pays around 50% as much on average, so it'd be a huge pay increase for them. Medicaid reimbursement rates, in particular, vary widely from state to state, so the doctor/hospital/clinic lobbies in some states will be more upset/happy than others.

What About Skyrocketing Prescription Drug Prices?

MFA would end the Big Pharma giveaway banning Medicare from negotiating drug prices. Under MFA, the Secretary would negotiate prescription drugs based on value assessments. If negotiations fail, the Secretary shall use prices paid by the Department of Veterans Affairs or the average price of these drugs in OECD nations. If drug manufacturers refuse to negotiate, MFA will not cover any of their products, with an exceptions process for drugs otherwise unavailable for individuals with chronic conditions. Additionally, MFA bans the use of prior authorization and step therapy in any type of health insurance: public or private.

This would be playing a dangerous game of chicken, and cuts to one of the uncomfortable truths about letting Medicare negotiate prices: In order to negotiate something, you have to be willing to make an ultimatum if your opponent refuses to budge. If X number of people desperately need a certain medication in order to live (or at least live a normal life), are they willing to actually cut off coverage of that medication?

What About Medicare Advantage?

Individuals will have the option to enroll in a Medicare Advantage for America plan, but these plans will need to charge an additional premium if they cover additional benefits. The bill also includes the Medicare Advantage Bill of Rights, which would prohibit plans from dropping providers during the middle of the plan year unless they can show cause, and would improve notice to plan enrollees about annual changes to provider networks before they commit to joining the plan.

THIS is something else (in addition to making the program optional for half the country and charging premiums/deductibles, even though those are already part of Medicare anyway) which "pure" single payer activists will likely flip out about. There's a contingent of SP purists who are opposed to any private/profit motive-based provisions being included in a theoretical SP plan. I'm not thrilled about Medicare Advantage, but it seems to be pretty popular, so killing it off seems like asking for more headaches/opposition to the bill without much reason.

How Is Medicare For America Paid For?

Medicare for America will be financed by sunsetting the Republican tax bill, imposing a 5% surtax on adjusted gross income (including on capital gains) above $500,000, and increasing the Medicare payroll tax and the net investment income tax. Medicare for America also increases the excise taxes on all tobacco products, beer, wine, liquor, and sugar-sweetened drinks.

Everyone wants to go to heaven but no one wants to die to get there. Expanding publicly-financed healthcare coverage to any significant degree will obviously involve raising taxes to some extent. Oddly, I suspect that the sugar-sweetened drink excise tax will actually cause the biggest public stink...not because it's the largest source of revenue (it's probably one of the smaller ones), but simply because it impacts everyone. I have no problem with any of the listed funding sources, of course, but obviously a lot of people would.

States will also need to make maintenance of effort payments equal to the amounts they currently spend on Medicaid and CHIP. For states that did not expand Medicaid, these amounts would be inflated by the growth in gross domestic product (GDP) per person plus 0.7 percentage points. For states that did expand Medicaid, these amounts would be inflated by the growth in GDP per person plus 0.4 percentage points.

After 10 years of payments, they would then increase by the growth in GDP per person plus 0.7 percentage points for all states. This structure would ensure that no state spends more than they currently spend, while giving a temporary discount to states that expanded their Medicaid programs.

That makes perfect sense to me; the states which sat on their asses and refused to expand Medicaid for what would amount to nearly a decade by the time Med4America was signed into law shouldn't get off the hook. I'd have to read the exact wording to see if there are any variances for states which did expand Medicaid, but did so late in the game (like Pennsylvania, Indiana, Virginia, Utah and so forth).

If states refuse to make the maintenance of effort payments, they will be no longer be eligible for funding under the Mental Health Services Block Grant program, Social Services Block grant program, the Substance Abuse Prevention and Treatment Block Grant program (Federal Health Centers Program), State Targeted Response to Opioid Crisis Grants, Community Services Block grants, Section 330 grants, and the Ryan White HIV/AIDS Program grant program.

The federal government can't legally require that individual states pay into a program which no longer exists, but they can certainly cut off federal assistance to those which don't, so this seems like a pretty compelling move.

It's important to note that the bill defines eligible individuals as:

every individual who is a resident of the United States is entitled to benefits for health care services under this title. The Secretary shall promulgate a rule that provides criteria for determining residency for eligibility purposes under this title.

In other words, the Med4America bill should cover pretty much everyone...although it sounds like it would be up to whoever the HHS Secretary is to decide how far that goes in terms of undocumented immigrants. It sounds like they're dropping this hot potato in the lap of the HHS Secretary instead of codifying that yes, it includes undocumented immigrants or no, it doesn't.

Also worth noting re. another hot button issue:

- YES, the Med4America would cover abortion and related reproductive health services, period:

‘(c) RESTRICTIONS SHALL NOT APPLY.—Any other provision of law in effect on the date of enactment of this title restricting the use of Federal funds for any reproductive health service, including abortion, shall not apply to monies in the Trust Fund.

...SEC. 127. ABORTION COVERAGE. Notwithstanding any other provision of law, Federal funds may be used to provide for abortion services under any health program under any of the following: (1) Indian Health Service. (2) Benefits provided to women veterans. (3) Benefits provided through the United States Immigration and Customs Enforcement to women in detention centers under the jurisdiction of such agency.

Unlike undocumented immigrants, Med4America tackles the Hyde Amendment head on. It doesn't technically repeal Hyde...it just states that Hyde doesn't apply to Med4America. I'm sure that won't cause any controversy or backlash either :)

Again, there's a lot of overlap with CAP's "MEFA" proposal from last year; instead of rehashing all of it, I'd advise reading my overview of that plan with the understanding that some elements have been changed in this one. I'm sure there would be further changes/tweaks if Med4America were to actually make it all the way through the legislative process anyway.

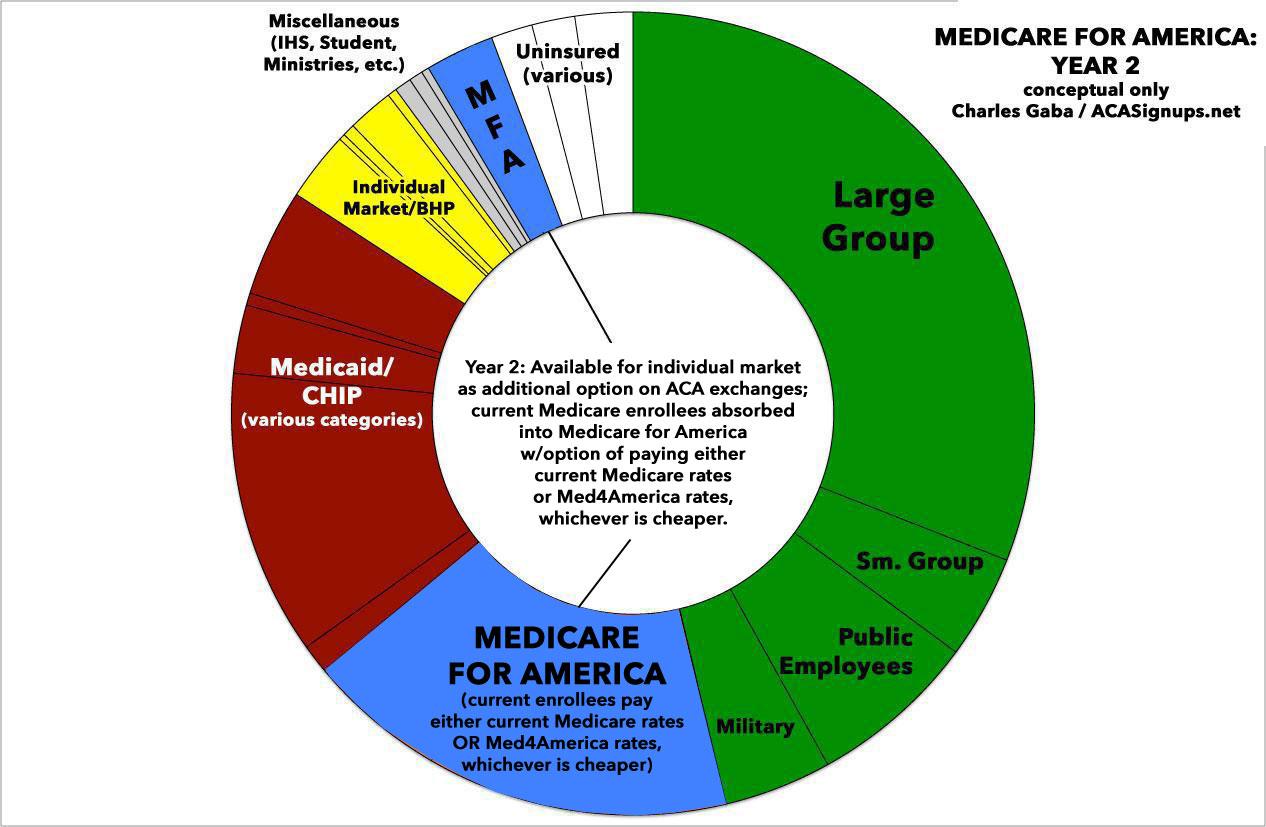

UPDATE 1/29/19: Whoops! It looks like there are a couple of important differences between MEFA and Med4America, especially surrounding "legacy" Medicare. I've updated the bullets and graphics below to better reflect how Med4America would be phased in.

If you scroll down to the bottom of my MEFA write-up, you'll see my "Psychedelic Donut" graphics, which give a general idea of how the Med4America law would eventually expand to provide comprehensive, universal coverage for everyone. I think the phase-in timeline is the same as under "MEFA" but could be wrong. I've recreated the graphics below with slight modifications.

- Years 1-2 (2020 - 2021): Med4America available as a public option on the existing ACA individual market exchanges only...and mainly in rating areas where the HHS Secretary determines it's really needed (i.e., only one carrier on the exchange or rural areas with excessively high costs, limited service providers, etc). I think the subsidy structure would still be based on the current ACA formula for the first two years but could be wrong.

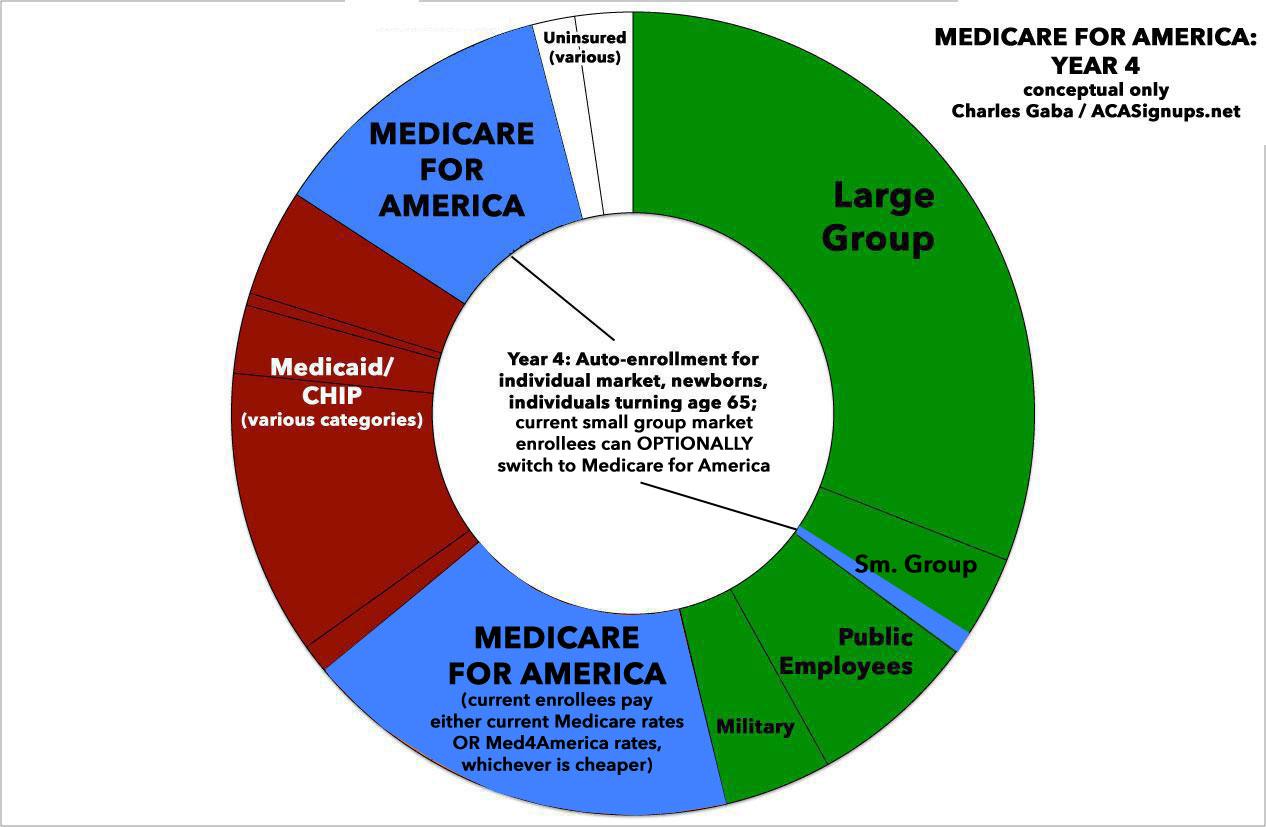

- Years 3-4 (2022 - 2023): Med4America autoenrolls everyone currently enrolled in the individual market; short-term plans/other non-ACA compliant plans; Medicare (although current enrollees could choose to pay existing Medicare rates if they're cheaper); all newly-eligible Medicare enrollees (i.e., those turning 65); all dual-eligible (Medicare/Medicaid) enrollees; and all newborn babies (around 4 million per year). Small group employers could also optionally start enrolling their employees into Med4America as well. This would also be the point that the massively-enhanced subsidy structure noted earlier would go into effect...which means huge chunks of the currently-uninsured population should also jump onboard.

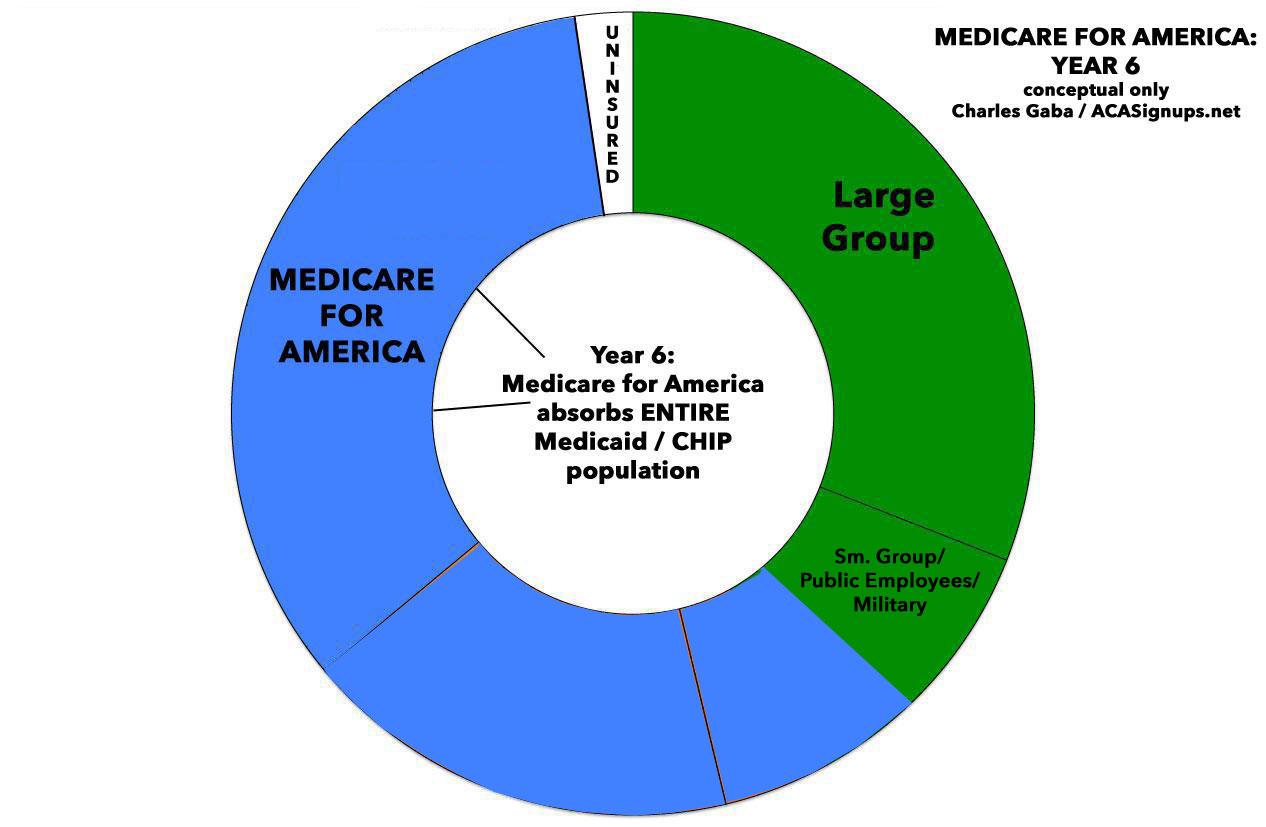

- Years 5-6 (2024 - 2025): Med4America would absorb the entire Medicaid/CHIP enrollment population, including those enrolled in Medicaid via ACA expansion. At this point, MEFA would be covering something like 60% of the entire U.S. population, with employer-based insurance still covering perhaps 30% and maybe 5% of the population (15 million) still uninsured for one reason or another.

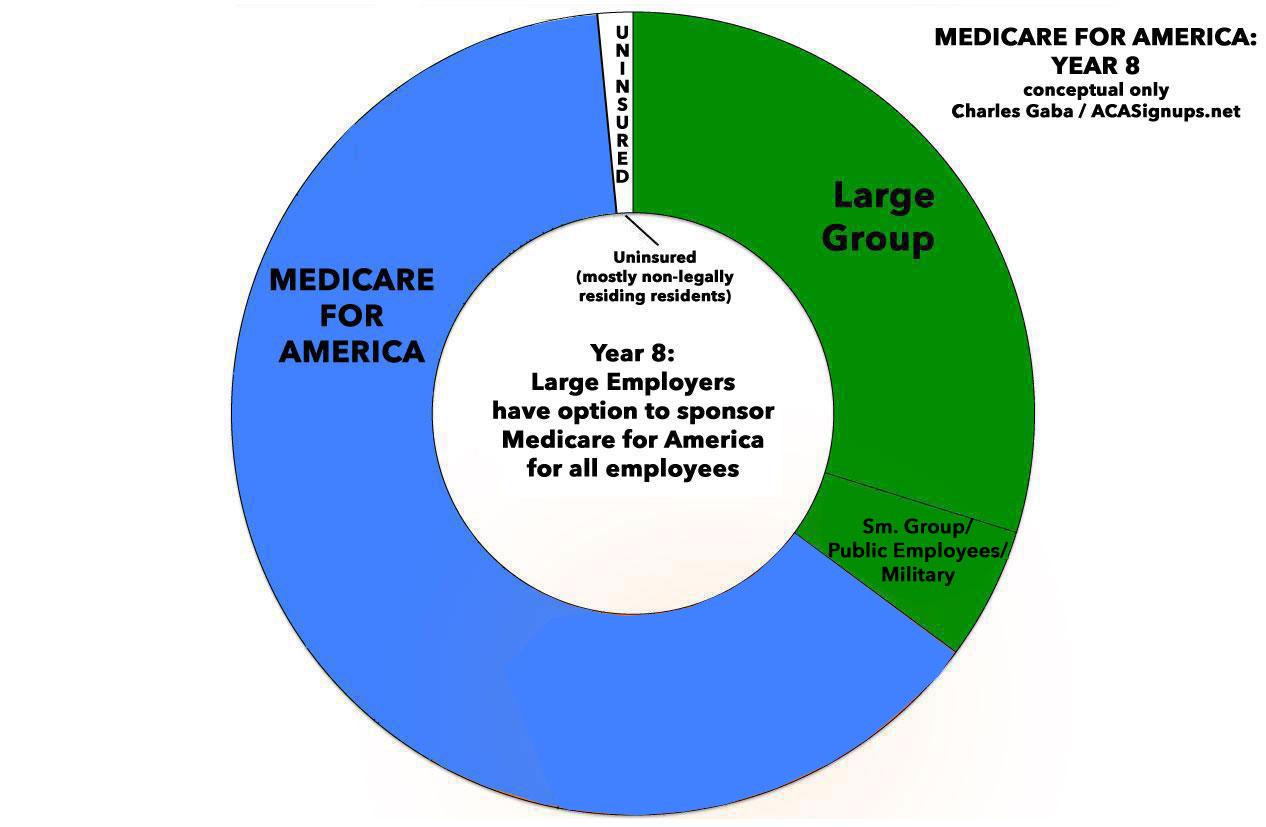

- Years 7 and beyond (2026 +): This is the point at which Large Employers (over 100 employees) would have the option to drop their coverage in favor of shifting their employees over to Med4America and paying a flat 8% annual payroll tax instead.

In general, this is a more fleshed-out version of CAP's MEFA proposal, particularly on the funding side fo the equation. I still have to read through the entire bill text, and I'm sure there's more stuff in there worth noting (both good and potentially not so good), but overall I like it very much, for the same reasons I like MEFA but more so.

One more thing: We still need a robust ACA 2.0 bill in the meantime, although if Med4America were to be signed into law exactly as described and along the timeline above, the ACA 2.0 bill would only theoretically be needed for 2 years instead of 5-6.

NOTE: I'm actually scheduled to meet with Rep. DeLauro in DC this week, so I hope to find out a few more details. I might have to make some corrections to my assuptions above.

Advertisement