GAO confirms Trump's HHS Dept. botched Open Enrollment in many ways, but something else caught my eye...

Sun, 08/26/2018 - 4:31pm

There were several stories over the past few days about a new, just-released report from the General Accounting Office (GAO) which examined how well/poorly the Trump Administration handled the 2018 Open Enrollment Period last year.

Many of the findings were things which I had been either predicting or documenting all year:

- Enrollment through Healthcare.gov Was 5 Percent Lower in 2018 than 2017

- Stakeholders Reported That Plan Affordability Likely Played a Major Role in Enrollment

- HHS Reduced Consumer Outreach for 2018 and Used Problematic Data to Allocate Navigator Funding

- HHS Did Not Set Numeric Enrollment Targets for 2018, and Instead Focused on Enhancing Certain Aspects of Consumers’ Experiences

We identified a list of factors that may have affected 2018 healthcare.gov enrollment based on a review of Department of Health and Human Services information, interviews with health policy experts, and review of recent publications by these experts related to 2018 exchange enrollment.

Factors related to the open enrollment period:

- Open enrollment conducted during a shorter 6-week open enrollment period.

- Consumer awareness of this year’s open enrollment deadline.

Factors related to plan availability and plan choice:

- Plan affordability for consumers ineligible for financial assistance.

- Plan affordability for consumers eligible for financial assistance.

- Consumers’ perceptions of plan affordability.

- Availability of exchange-based plan choices.

- Availability of off-exchange plan choices.

- Consumer reaction to plan choices.

Factors related to outreach and education:

- Reductions in federal funding allocated to outreach and education, and lack of television and other types of advertising.

- Top Administration and agency officials’ messaging about the health insurance exchanges and open enrollment.

- National and local media reporting on the exchanges and open enrollment.

- Local outreach and education events conducted by federally funded navigator organizations.

- Outreach and education efforts and/or advertising by some states, issuers, advocacy groups, community organizations, and agents and brokers.

Factors related to enrollment assistance and tools:

- Availability of one-on-one enrollment assistance from federally funded navigator organizations.

- Availability of one-on-one enrollment assistance from agents and brokers.

- Updates to the content and function of the healthcare.gov website.

- Availability of the healthcare.gov website during the open enrollment

- period.

- Availability of assistance through the call center during the open enrollment period.

Other factors:

- Consumer understanding of the Patient Protection and Affordable Care Act and its status.

- Automatic re-enrollment occurred on the last day of the open enrollment period.

...and so forth. Other articles have gone into more detail about some of these things, especially the impact of Trump's HHS Dept. slashing the HC.gov marketing budget by 90%, slashing the navigator/outreach budget by 40% and so on, such as this writeup in Health Affairs.

However, I want to focus on an aspect related to the CSR reimbursement funding cut-off and subsequent Silver Loading/Switching workaround which this led to.

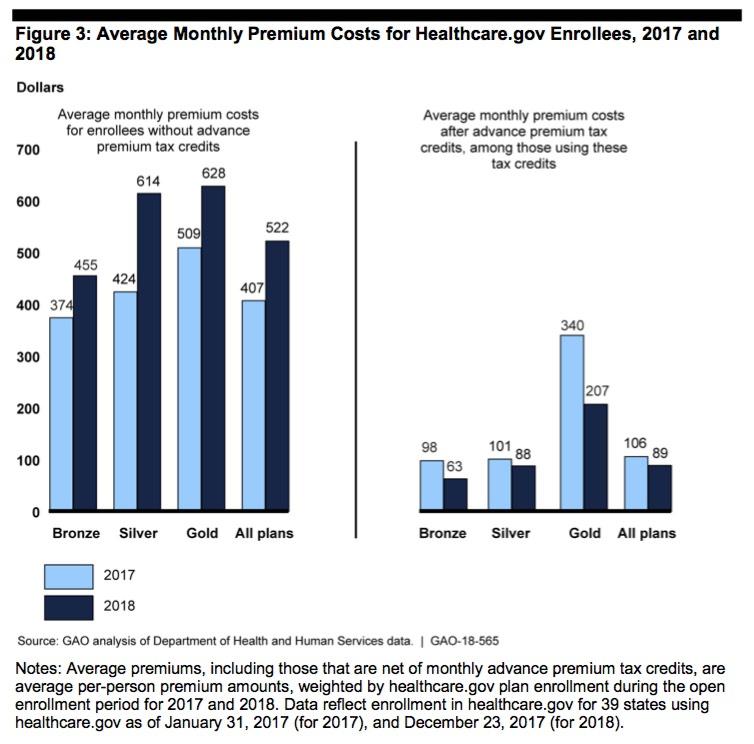

Page 15 of the GAO report is a bar graph which shows how average monthly net premiums changed year over year from 2017 to 2018 for both subsidized and unsubsidized enrollees at each metal level across the 39 states hosted at HealthCare.Gov:

As you can see, subsidized enrollees (on the right) actually made out better at every metal level, with average subsidized premiums dropping by 16%. At the same time, full-price premiums for unsubsidized enrollees (on the left) shot up a whopping 28% on average...22% for Bronze enrollees, 23% for Gold and a stunning 45% for unsubsidized Silver plan enrollees.

The cause of the divergence between subsidized premiums dropping while unsubsidized premiums increased dramatically was Donald Trump's order to discontinue Cost Sharing Reduction reimbursement payments to carriers. Since the carriers were still contractually required to provide the CSR assistance to eligible enrollees, they made up the difference (around $10 billion, I believe) by increasing the unsubsidized premiums instead. This in turn caused the ACA subsidy formula to skew higher...and since most carriers in most states "Silver Loaded" by dumping the entire CSR cost onto Silver plans only, it meant that the subsidies didn't just increase slightly, they increased by more than the amount of the premium increases in most cases.

As a result, most subsidized enrollees ended up seeing what they actually paid drop year over year...while unsubsidized enrollees saw their full-price premiums increase dramatically, especially those enrolled in Silver plans.

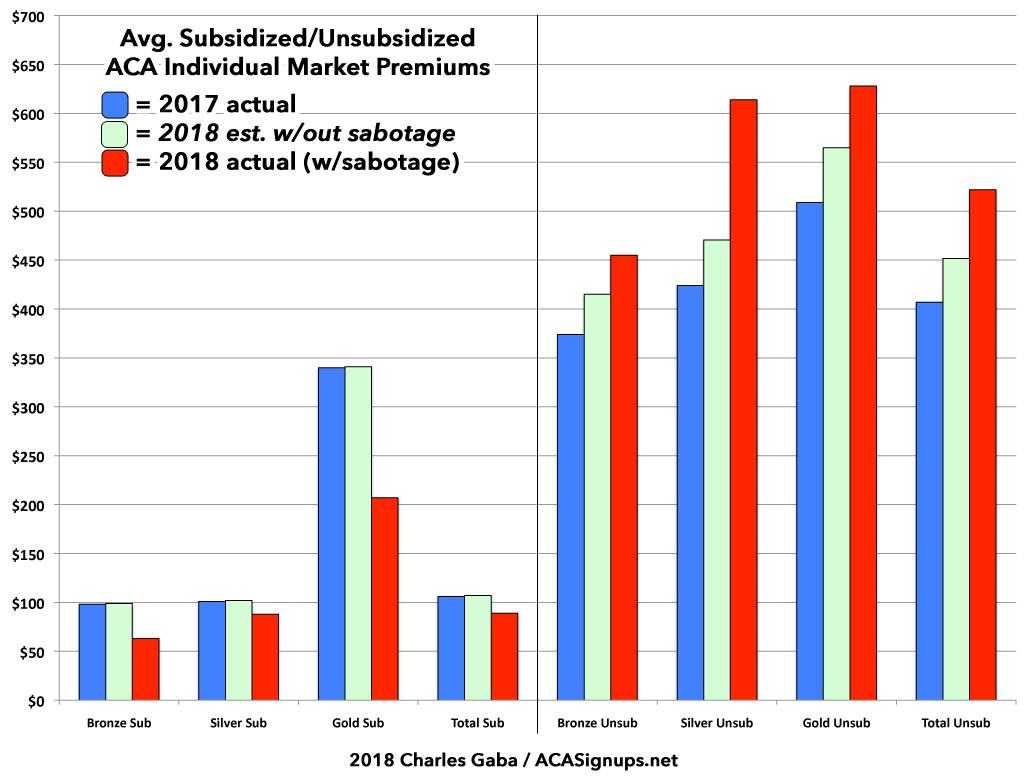

The only problem with the bar graph above is that it doesn't show what the 2018 premium situation would have been if CSR payments hadn't been cut off...that is, what would it look like without last year's sabotage efforts by Donald Trump and his administration?

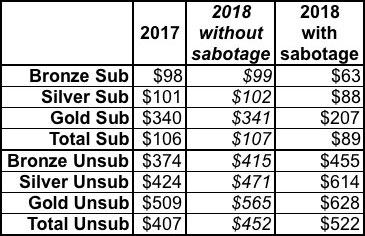

Well, as I demonstrated repeatedly last fall and earlier this year, of the 28% average unsubsidized rate hikes nationally, rates would have only gone up perhaps 10-11% in that scenario, with the additional 17 points or so being caused by the CSR cut-off and related sabotage efforts. I've therefore expanded on the GAO graph above with my own, which includes my best estimates of how 2018 premiums would have changed for each population in that alternate universe (I've also moved the subsidized enrollees to the left side of the graph, where it makes more sense to have them). I've sandwiched the "alternate universe" bars in light green between the actual 2017 and 2018 premiums:

In a world where premiums had increased due to the normal factors only (medical trend, the reinstatement of the ACA carrier tax, etc), subsidized premiums would have only changed slightly--increasing by perhaps a dollar or two per month at most due to fluctuations in the risk pool and plan choices.

Unsubsidized premiums, however, would have only increased roughly 11% or so across the board (there may have been some variances between the different metal levels). Bronze enrollees would likely have paid around $41 more per month instead of $81 more...a savings of $480 for the year. Gold enrollees would have paid $56 more instead of $119 more...an annual difference of $756. And Silver enrollees would have, on average, paid $47/month more instead of $190/month more...a difference of $143/month or an eyebrow-raising $1,716 for all of 2018.

Overall, unsubsidized enrollees are paying around $840 more this year due to Trump's sabotage than they would have otherwise...while subsidized enrollees are paying around $216 less than they would have. It's the second fact which led Democrats and other ACA supporters (including myself) to back off of the "Fund CSRs!" attacks last fall; Silver Loading and Silver Switching made the situation more complicated, since funding them now--without any other structural or formula changes--would, ironically, have the opposite effect--premiums for unsubsidized enrollees would indeed drop...but the cost for subsidized enrollees would actually increase. One of life's little ironies.

Advertisement