(sigh) Senate GOP tries to cover their asses on #TexasFoldEm by slapping together a sham pre-existing condition bill

Fri, 08/24/2018 - 10:41pm

With the idiotic #TexasFoldEm lawsuit coming up for oral arguments in just two weeks and the midterms in just ten, Senate Republicans appear to be in a bit of a panic over how to deal with the massive negative fallout if they win their court case (technically it was brought by 20 GOP attorneys general, not the Senators themselves, but they've spent the past 8 years trying to accomplish the same goal).

As a quick reminder: The #TexasFoldEm case uses the World's Flimsiest Excuse to try and eliminate the Affordable Care Act's critical health insurance coverage protections for the 130 million Americans who have pre-existing conditions.

In response, Republican Senators Tillis, Alexander, Grassley, Ernst, Murkowski, Cassidy, Wicker, Graham, Heller and Barrasso have introduced a new bill which they claim would ensure pre-existing coverage protections. Unfortunately, it...doesn't.

I've been out and about all day and will also be unable to update the blog all day Saturday, so I'll keep this one short. Besides, several others, including Jeffrey Young of the Huffington Post have already written up good overviews of this garbage:

Right there in the text, it says health insurance companies would not be allowed to deny an individual coverage or charge extra because of “health status, medical condition (including both physical and mental illnesses), claims experience, receipt of health care, medical history, genetic information, evidence of insurability (including conditions arising out of acts of domestic violence), disability, [or] any other health status-related factor determined appropriate by the Secretary [of Health and Human Services].”

But it’s what the bill doesn’t say that makes the above mostly meaningless.

Yes, insurance companies wouldn’t be allowed to refuse to offer coverage to someone who, for example, has a history of cancer or is pregnant. But they could sell someone a policy that doesn’t cover cancer treatments or the birth of a child.

Sure, premiums wouldn’t be allowed to vary based on health status or pre-existing conditions. But prices could dramatically vary based on age, gender, occupation and other factors, including hobbies, in ways that are functionally the same as basing them on medical histories. Insurance companies have a lot of experience figuring out that stuff.

Larry Levitt of the Kaiser Family Foundation also has a nice explainer:

A new bill would require insurers to guarantee access for people with pre-existing conditions and prohibit premiums based on health. But, it would allow insurers to exclude any coverage of the pre-existing conditions. A bit of a catch.https://t.co/Dgc1DNor0B

— Larry Levitt (@larry_levitt) August 24, 2018

This new Republican bill would prohibit insurers in the individual market from varying premiums based on health. But, premiums could vary based on age, gender, occupation, or leisure activities. Small business premiums could vary based on the health of their workers.

— Larry Levitt (@larry_levitt) August 24, 2018

So-called "pre-existing condition exclusions" were common in individual market insurance policies before the ACA, and are also typical in current short-term policies. The new Republican bill would allow them, making guaranteed access to insurance something of a mirage.

— Larry Levitt (@larry_levitt) August 24, 2018

Or, as someone else put it...

So they’d have to cover people WITH cancer or diabetes, they just wouldn’t have to cover that person’s cancer or diabetes. That’s...not helpful. https://t.co/rIrvCgcMnF

— Charles Gaba (@charles_gaba) August 24, 2018

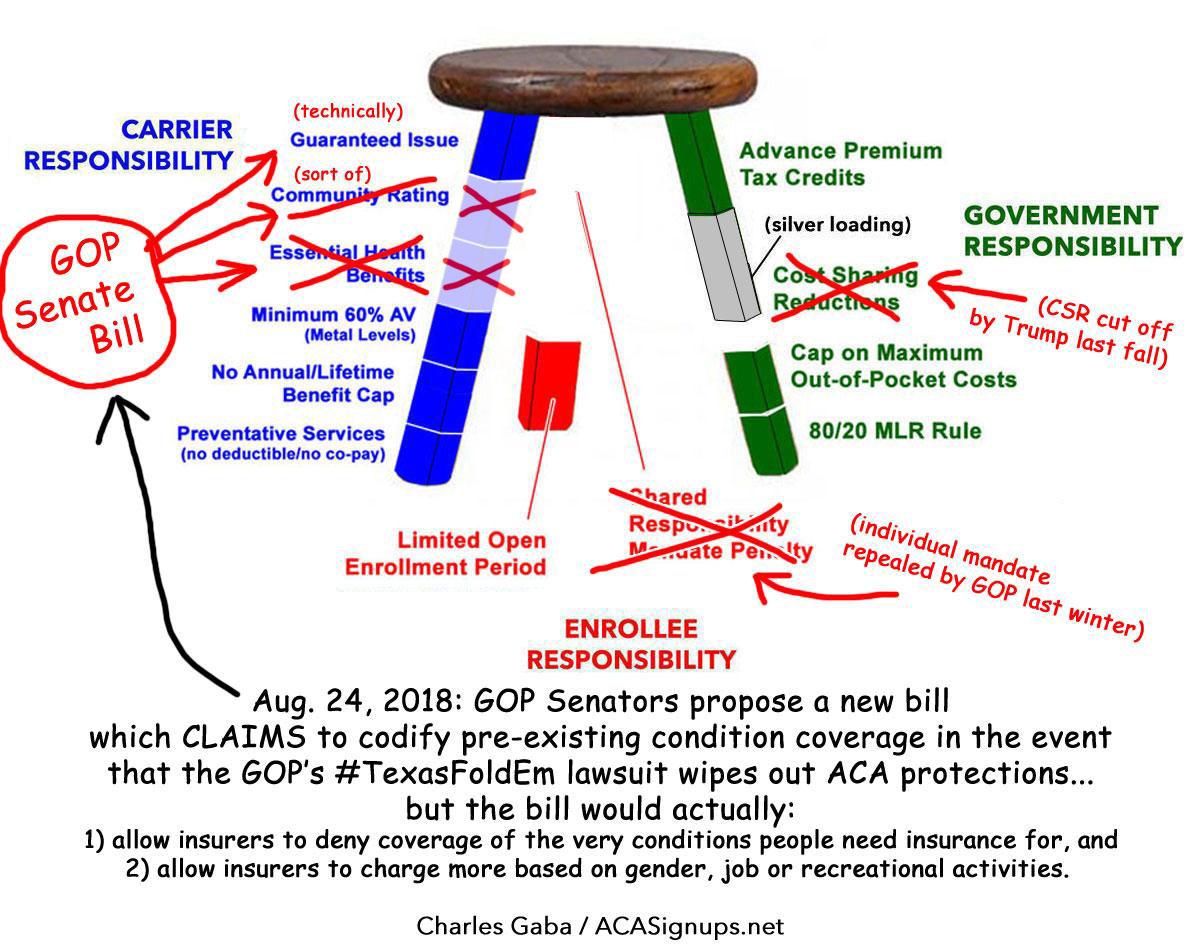

In short, this is basically what this sham bill would look like in practice:

Advertisement