New York: I've Got a Theory...(warning: sheer speculation ahead)

Mon, 07/30/2018 - 10:56pm

Monday afternoon there was a hell of a jaw-dropper out of the Empire State:

Gov. Cuomo just announced that he has directed Supt. Vullo to reject any individual market rate increase that included an increase to compensate for the repeal of the individual mandate

...Assuming that nothing else changes during the rate review process, this makes carriers that didn't associate a % of their rate request with the loss of the mandate big winners...and those who did, not so much.

Sure enough, after watching the half-hour speech by Cuomo, it sure as hell sounded like he was doing exactly that: Instructing the state insurance commissioner to only allow 2019 ACA individual market premiums to increase by around the 12.1% (on average) that they were expecting to go up with the ACA's individual mandate penalty in place instead of the roughly 24% (on average) that they said they'd have to raise them to cancel out the adverse selection impact of the mandate being repealed:

"Removal of the individual mandate is making insurance companies nervous, so they're adding big rate increases...it's diabolical..."

"They've come to the state and asked for a 24% increase...they would be effective in collapsing the exchange if that happens."

"We're not gonna let that happen. If we allow that rate increase to go through, it'd be hundreds of millions of dollars as a bonanza for the private insurance companies."

"Today I am directing the DFS superintendent to reject any rate increases as an effect of the individual mandate being removed."

"Insurance rates must be based on actual cost, not on political maniupulation."

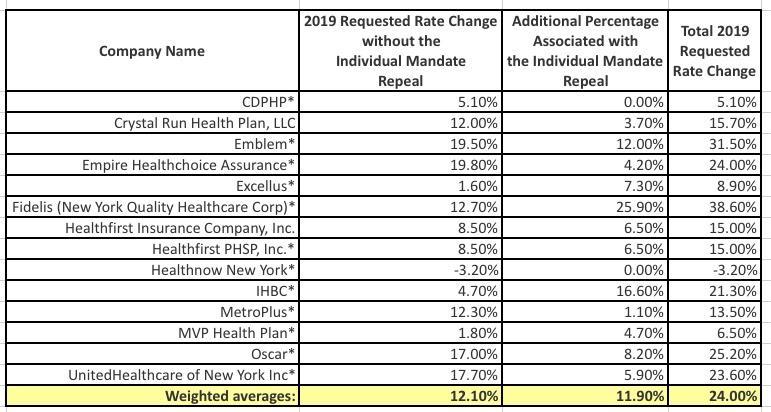

Here's the actual requested rate changes in question. Out of 14 carriers total, two of them (CDPHP and Healthnow NY) didn't plan on baking in some amount of a cushion to counter mandate repeal anyway, and one more (MetroPlus) tacked on a fairly nominal 1.1 percentage points. The rest, however are pretty significant, with Fidelis asking for a rather stunning 25.9% increase specifically tied to mandate repeal:

Now, as I noted earlier Monday, one would normally expect this to cause at least a few of the carriers to run fleeing for the hills. This is exactly what happened last fall in North Dakota, when Medica, one of the four carriers participating in the ACA indy market bailed after the state insurance commissioner refused to let them raise premiums to cover their impending Cost Sharing Reduction losses even though it was obvious that Donald Trump intended on cutting CSR reimbursement payments off (and which, of course, he did do just a few weeks later).

However, last summer, NY Gov. Cuomo issued an executive order tying MCO (Medicaid Managed Care Organization) contracts to ACA exchange participation. This would normally be a good thing, but in this case it means that any carrier which has won an MCO contract is required to stick around the NY exchange but isn't allowed to bake mandate repeal into their 2019 premium rates, which means they're stuck between a rock and a hard place: They can't leave but they may also be guaranteed losses if they stay.

Furthermore, as my friend Wesley Sanders reminded me, the deadline for carriers to completely pull out of the NY market was...June 30th. That means that even carriers without MCO contracts on the line apparently can't drop out now. They can drop out of the on-exchange market but would be required to keep at least a few policies available off-exchange. Of course, they might just pull a Freedom Life, in which they deliberately "offer" exactly one Bronze or Comprehensive policy in a single county off-exchange to technically fulfil their legal obligation to remain "on the market", but then effectively bury any knowledge of that policy's availability.

Even so, this still leaves the question of what the hell Andrew Cuomo was thinking this afternoon. I've been pondering this for the past few hours, and after discussing it with someone who seems to have pretty good insight into the situation (who wishes to remain anonymous), I've developed the following theory.

I need to stress that this is completely speculative.

- Andrew Cuomo is up for re-election in November.

- Andrew Cuomo is facing a primary challenge from the left in the form of one Cynthia Nixon, a single payer advocate.

- New York's Gubernatorial primary takes place on September 13th.

- Andrew Cuomo has been pretty good about protecting/supporting the ACA.

- Having 24% premium increases on the ACA market making headlines just before the primary would not be helpful to Cuomo's image.

Cuomo's speech today makes sense politically: It gives him some populist cred (he's fighting for the little guy!) while "sticking it" to the Big Greedy Insurance Companies (who, let's face it, everyone hates anyway, so it's not like they're gonna get a whole lot of sympathy). Still, they're gonna be pretty pissed off at Cuomo ifthey end up being stuck eating massive losses a third time (after the Risk Corridor Massacre and the Cost Sharing Reduction cut-off).

But here's the thing: You have to keep in mind that even without today's announcement, there was no guarantee that the requested rate increases above would be granted. These are preliminary only. They still have to be reviewed and approved by the state Insurance Commissioner at the Dept. of Financial Services, and state regulators often cut rate hikes down. Sometimes it's minor, sometimes it's by a significant amount.

For instance, in Oregon earlier this year, carrier BridgeSpan originally asked for a 9.4% rate increase, but this was cut down to 4.5% by state regulators before being approved. Carrier Providence asked for a 13.6% hike...which was cut down to 10.6% during the first round of review and then cut again to 9.5% before being approved.

In other words, there's a good chance that New York regulators might have been planning on cutting down some of the requested increases listead above anyway...both with or without the mandate being in place.

For example, it's possible they were planning on cutting Fidelis' request (12.7% with the mandate, 38.6% without) down by, say, 5 points each (7.7% or 33.6%), and so on.

For all I know, the 12.1% / 24.0% averages may have been scheduled to be lopped in half to around 6% with the mandate in place...or 12% without it.

What made me think about this possibilty? Well, if you look at the 28 states which have submitted preliminary 2019 rates so far, the thing which sticks out in my mind is that there's only 8 states seeking double digits, and New York's 24% is the second highest in the country (right below Maryland)...both with and without the mandate penalty in place. MAYBE both the 12% and 24% are legitimate projections by the actuaries...but maybe they simply overestimated on both fronts. Nothing neferious here, actuarial science isn't exact, which is why state regulators have a review process in the first place. I'm just saying that it's possible that there was some elbow room for them to cut rates down regardless of Cuomo's announcement today.

AGAIN, I have absolutely no idea if this is the case...but let's suppose it is. Let's further suppose that Cuomo knew this (or at least suspected it).

If that's what happened, then his move today makes sense. He'd be able to score political points ("See? Cuomo is fighting to keep our rates low!") by taking credit for something which was already going to happen anyway.

Anyway, it's a theory. If you have a better one, I'm all ears.

SIDENOTE: Someone else suggested that Cuomo may be secretly planning to reinstate the individual mandate penalty via executive order, either soon or even after the primary election. I find this to be even more farfetched than my own theory above, especially since I suspect he doesn't have the legal authority to do so without the state legislature passing a law first, but I don't know enough about New York state law to hazard a guess. Anything's possible, I suppose.

If he's legally allowed to do so, it's even conceivable that he could reinstate the penalty after Open Enrollment starts as a sort of emergency measure. The 2019 rates would already be baked in at "mandate levels", so he'd simply be filling in the other half of that equation. Again, not likely, but nothing about his announcement made much sense without something like this in the works.

Advertisement