One Of These Things is Not Like the Others.

Mon, 08/28/2017 - 1:18pm

Note: This entry is in response to Kimberly Leonard's article at the Washington Examiner in which she interviews unsubsidized individual market enrollees.

Amidst all the discussion and debate about how to fix/improve/strengthen/expand the Affordable Care Act, one thing I've written about as much as anyone else (and far more than many others) is people enrolled in the unsubsidized individual market. To recap: Around 18 million people are enrolled in individual market policies, of which around half (9 million) receive tax credits to help cover a chunk of the premiums. Of those, around 7 million also receive CSR assistance to help cover deductibles and co-pays. The amount/portion of their expenses which are covered varies from high to low based on a sliding income scale, and it's frankly too skimpy at the upper end of that range, but at least these folks receive some assistance.

The other half of the individual market, however--a little under 9 million--receive no financial assistance whatsoever. 1-2 million of these folks aren't bothered too much by this...but only because they're still enrolled in pre-ACA Grandfathered or Transitional policies, which aren't nearly as comprehensive as ACA plans. They pay far less, but they're also generally covered for far fewer services. That leaves perhaps 7-8 million people who are a) on the individual market and b) enrolled in ACA-compliant policies but c) aren't eligible for ACA subsidies. They have to pay 100% out of pocket for their insurance policies, including premiums, deductibles and co-pays.

Officially the subsidy cut-off point is 400% of the Federal Poverty Line: Around $48,000 for a single adult or $98,000 for a family of 4.

Now, don't get me wrong: If you earn, say, 1000% of the poverty line (half a million dollars if you're single, a million bucks for a family of 4), I'm not exactly gonna be wringing my hands over your plight if you have to pay $700/month apiece for your health insurance; that's only 1-2% of your income. However, the vast majority of people earn far less than that...and that's where the most obvious problems with the ACA tax credit structure lie.

For instance, let's suppose you earn just above 400% FPL. In my case, at 47 years old with a spouse and one child, that would be around $82,000/year. Our least-expensive option would be a $576/mo Bronze plan...with a $13,300 deductible. Ouch. Knocking the deductible down below $5K would start at $710/month for a Silver plan. What about if we were all 7 years older? Then we'd bee looking at $752/mo for a bare-bones Bronze or $926/mo for the Silver...or nearly 14% of our total income. That smarts. And if we were 14 years older, with our son just barely below the 26 young adult cut-off point, we'd be facing over $1,000/mo for the Bronze or $1,238/mo for the silver...a whopping 15% of income. Granted, you could argue that our theoretical 25-year old son should've started pulling his weight by then, but let's suppose he's wrapping up grad school or whatever, while my wife and I are still earning what we did when he was a kid? The point is, that's gonna sting.

In addition, that 400% FPL cut-off point is the upper limit, but it's lower than that for many folks. Depending on exactly where you live, how old you are and what the benchmark plan is in your area, your income could be quite a bit lower and you still won't qualify for tax credits. For instance, a single 21-year old living in Oakland County, Michigan could have an income as low as $28,500 (236% FPL) and still not qualify (at $28,000 even they're eligible for a nominal $5/month), due to how the benchmark Silver premium formula works.

OK, so the obvious solution here is to a) raise or remove the income level cut-off point for tax credits and b) beef up the formula below that, as I've been arguing for awhile now, right?

The only real argument I've heard against this is that it "encourages more people to mooch off the government teat paid for by hard-working taxpayers who pull themselves up by their own bootstraps", bla bla bla Libertarian Ayn Rand self-sufficiency yadda yadda yadda.

Here's the problem with that: It's bullshit.

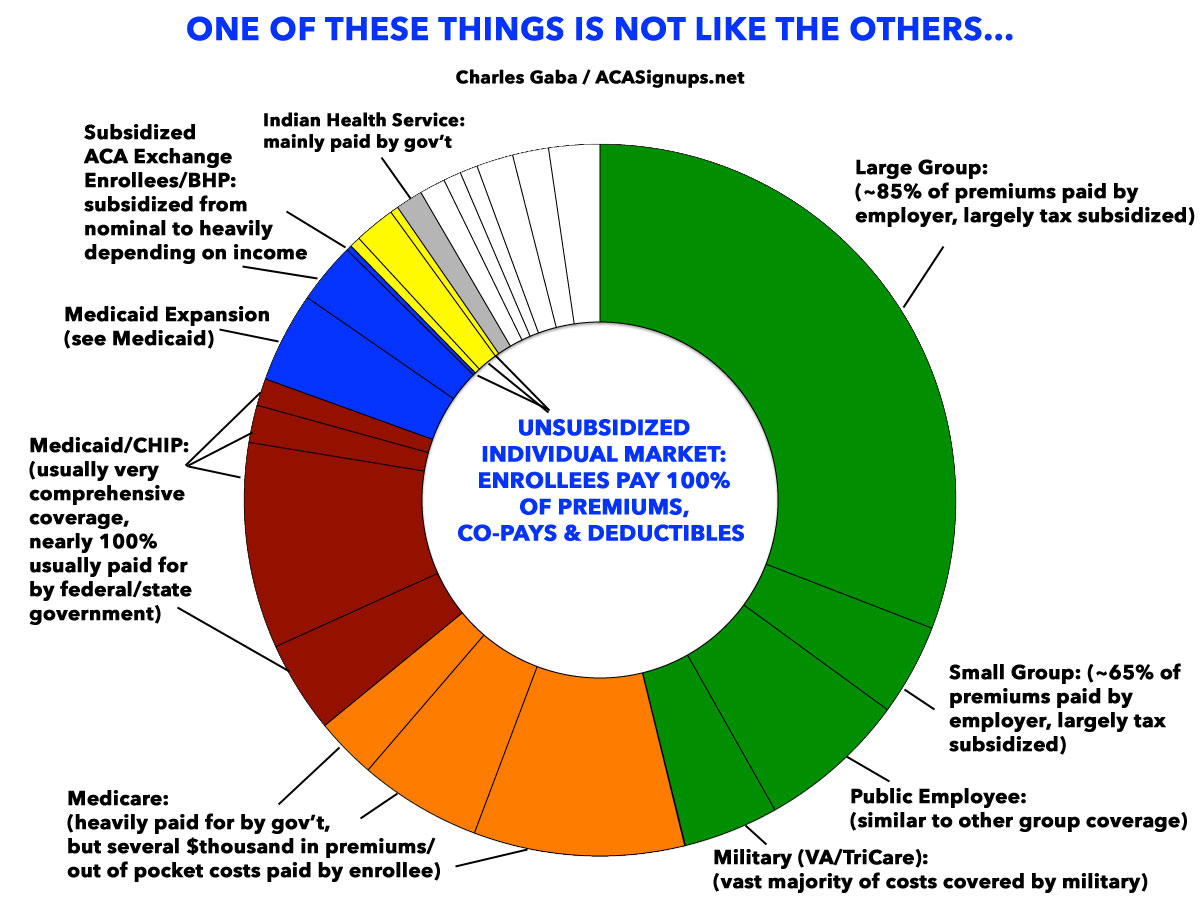

A year and a half ago I compiled a pie chart breaking out the type of healthcare coverage which everyone in the U.S. has (or doesn't have, in the case of the uninsured)...employer coverage, Medicare, Medicaid, the individual market and miscellaneous. Below, I've updated the proportions to reflect slight changes as of Spring 2017...but the main point is that EVERY GROUP OF HEALTHCARE COVERAGE ENROLLEE is heavily subsidized EXCEPT for these 7-8 million people (along with the ~28 million uninsured folks, of course).

Medicaid is nearly entirely taxpayer funded, of course. Medicare only covers about 80% of most medical expenses, and has premiums/deductibles/co-pays for some services...but it's still mostly taxpayer funded. TriCare and the VA? Taxpayer funded. Most public employees have the bulk of their policies subsidized by their employer...the government. And even employer coverage is heavily subsidized, with 65-85% of premiums generally paid for by the employer. Yes, that's considered part of their compensation as an employee...but even then, an average of over $1,800 per enrollee is still taxpayer subsidized because employer-sponsored insurance is tax deductible. The federal government loses $270 billion per year due to the employer tax exclusion rule...which, of course, is the main reason we have our "employer-based insurance" model in the first place.

Removing the 400% FPL cap on APTC assistance (and beefing up the structure below that) wouldn't be "giving away" anything to "undeserving moochers"...it would be bringing the remaining insured population more in line with everyone else in the country (except, of course, for the ~9% who have no healthcare coverage whatsoever, which is a whole different discussion...except that taking these steps would by itself shift several million more people from the "uninsured" to "individual market" category anyway).

As it happens, Sen. Feinstein of California, along with several other Democratic Senators, actually has introduced a bill to resolve the first half of this issue...it would simply remove the 400% cap altogether, which would mean instead of the upper-end 9.69% income cap being limited to those earning 300-400% FPL, it would apply to everyone from 300% and up. No one would pay more than 9.69% of their income for a benchmark Silver plan, regardless of income.

This would not mean billionaires receiving tax credits, however, because at a certain point, that 9.69% cut-off would taper off. At $100,000/year for a single adult, for instance, the benchmark plan would have to cost them at least $808/month ($9,700/year in premiums) before they'd receive any assistance at all. They average around $410/month this year, for comparison.

Advertisement