New York: NYSOH releases highly-detailed OE3 ACA exchange report!

Fri, 08/12/2016 - 4:28pm

Thanks to Dan Goldberg for the heads up:

NY State of Health: The Official Health Plan Marketplace 2016 Open Enrollment Report August 2016

It's a whopping 64 pages long. Some of it is stuff like "how many people speaking Cambodian called the support lines?" (answer: 6) and the like, but there's also a whole bunch of handy data regarding actual healthcare policy/program enrollment in the Empire State. I don't mean to be ungrateful, as this is extremely comprehensive...but it would've been far more useful if the report had included data from the end of March (or even later), as opposed to cutting off at the end of the 2016 Open Enrollment period (January 31st). Due to attrition due to people who never pay their first premium, are denied policies for legal reasons (residency status, etc) and so on, only around 82% of the 272,000 people who selected QHPs in NY during OE3 were still actually enrolled as of two months later. A good 10-12% or so never paid in the first place and another 6-8% were kicked off involuntarily for one reason or another...none of which is reflected in this report.

Still, that aside, let's take a look!

More than 2.8 million people—about 15 percent of the State’s population—were enrolled in plans through the NY State of Health as of the end of the 2016 open enrollment period on January 31, 2016. That represents a net increase of nearly 700,000 since the second open enrollment period when 2.1 million people enrolled. New York has seen a significant, corresponding reduction in the number of uninsured. Since the Marketplace opened in 2013, the number of uninsured New Yorkers has declined by nearly 850,000. The rate of uninsured declined from 10 percent to 5 percent between 2013 and September 2015, according to data recently released by the Centers for Disease Control and Prevention.

That 2.8 million figure includes exchange QHPs, Basic Health Plan enrollees (BHP, or Essential Plan as NYSOH calls it), and Medicaid expansion (along with NY's unique "Child Health Plus" program, which is not to be confused with CHIP):

- 271,964 QHP enrollees (down to 223K as of 3/31)

- 379,559 BHP enrollees (unclear what the 3/31 figure is, but it's almost certainly higher since BHP enrollment is year-round)

- 1,966,920 Medicaid enrollees

- 215,380 Child Health Plus enrollees

- 2,833,823 grand total

It's important to remember, too, that just as there are additional off-exchange QHP enrollees, the bulk of Medicaid/CHIP enrollment is off-exchange as well in most states. In New York, another 4.4 million people are already enrolled in traditional Medicaid/CHIP, for a total of over 6.4 million people state-wide, or roughly 1/3 of the entire state population.

The BHP (Basic Health Plan) was just introduced in New York this year via the ACA (Minnesota already had their own BHP system prior to the ACA, though it has since been pretty much converted over to the ACA version). It's important to remember that there are two populations which can enroll in the BHP:

- Individuals under age 65 with household incomes of 0-138 percent of FPL who are lawfully present in the United States, but do not qualify for Federal Medicaid because they have been legal residents for less than five years.

- Individuals under age 65 with household incomes between 138 and 200 percent of the federal poverty level (FPL), who would have otherwise been eligible for a QHP with financial assistance.

According to NYSOH, 98% of those who qualify for the BHP sign up for it, which makes sense. It's a great program at $20/month.

As for the actual "official" exchange QHPs, only 54% of the 272K who selected these are eligible for APTC assistance, far lower than the 83% national average...due to a large chunk of lower-income QHP enrollees being cannibalized by the BHP program, of course.

Medicaid expansion:

Through January 31, 2016, 1,966,920 individuals enrolled in Medicaid through NY State of Health. This includes 1,743,805 enrollees who renewed 2015 coverage and 223,115 enrollees who are new to the Marketplace during the 2016 Open Enrollment Period. A lower share of Marketplace Medicaid enrollees are new to the Marketplace (11 percent) compared with QHP and EP enrollees. Through the Affordable Care Act, New York expanded Medicaid eligibility levels to 138 percent of FPL to all eligible adults. Since New York’s eligibility levels already largely met this new federal standard prior to the Affordable Care Act, this expansion affects single and childless adults whose eligibility had previously been set at less than or equal to 100 percent of FPL. Approximately nine percent of Medicaid enrollees are part of the expansion population, consistent with 2015.

I think that's 9% of the total Medicaid enrollment in NY, which would be roughly 576,000 people; the rest would presumably already be eligible for Medicaid in New York regardless of the ACA.

Child Health Plus:

Through January 31, 2016, 215,380 children enrolled in Child Health Plus (CHP) through the NY State of Health, including 46,479 enrollees (22 percent) who are new to the Marketplace during the 2016 Open Enrollment Period. Children up to age 19 in households with incomes up to 400 percent of FPL can enroll in subsidized insurance through CHP. CHP eligibility begins where Medicaid eligibility ends (223 percent of FPL for children under 1 and 154 percent of FPL for children over 1). There is no CHP premium for children in households with incomes below 160 percent of FPL, and a sliding scale premium for those in households with incomes between 160 and 400 percent of FPL. Households with incomes above 400 percent of FPL have the option to purchase CHP or QHP coverage at full premium. Ninety-six percent of children enrolled in CHP through the Marketplace are enrolled with no premium or sliding scale premiums, and 4 percent are enrolled with full premiums.

As noted above, CHP is unique to New York and shouldn't be confused with the Children's Health Insurance Program, or CHIP, which every state has (the 8.4 million which Hillary Clinton keeps campaigning on). Around 600,000 NY children are enrolled in CHIP in addition to the 215K enrolled in CHP, although I think those 600K are already included in the 6.4 million Medicaid figure above.

In terms of how many exchange enrollees are newly insured/covered thanks to the ACA:

At the end of the 2016 open enrollment period, ninety-two percent (92 percent) of those who enrolled through the Marketplace reported that they did not have health insurance at the time they applied.

This sounds astonishing, until you remember that it includes the Medicaid, CHP and BHP enrollees, who are obviously far more likely to be previously uninsured. When you look strictly at QHP enrollees, it drops to 57%, which is still very good...except that even then, that's based only on the 54% who are receiving APTC assistance. This figure probably drops considerably if you were to include those paying full price (over 400% FPL income). Still not bad.

There's another too-good-to-be-true statistic here as well: "61% of marketplace enrollees are 34 or younger!!" Woo-hoo, the risk pool problem is solved!

Well...not quite. Again, that 61% incluedes Medicaid and BHP, neither of which is part of the QHP risk pool. If you look purely at QHPs (which is crucial), it drops to 31%...and only 28% are 18-34, exactly the same as the rest of the country. Ah, well.

There's a whole bunch of ethnic and geographic data in the report; check it out if you're interested.

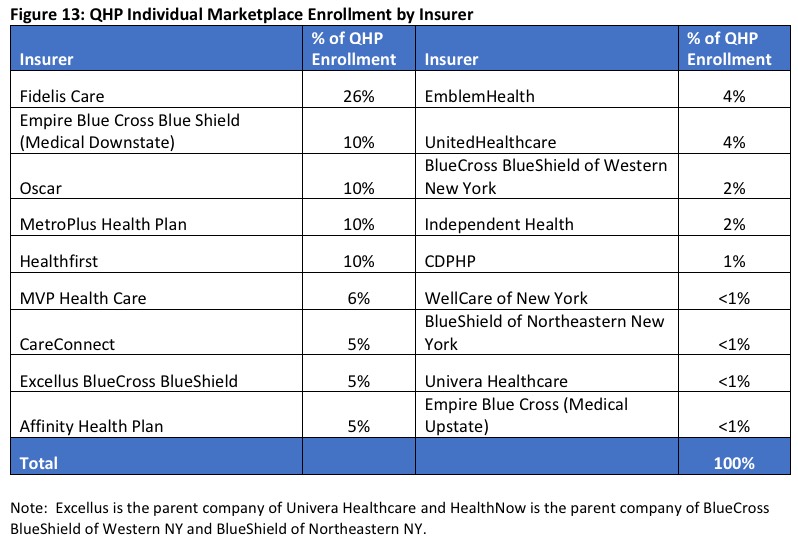

Oh, for corporate/market share geeks, there's a breakout of the QHP enrollment by insurance carrier:

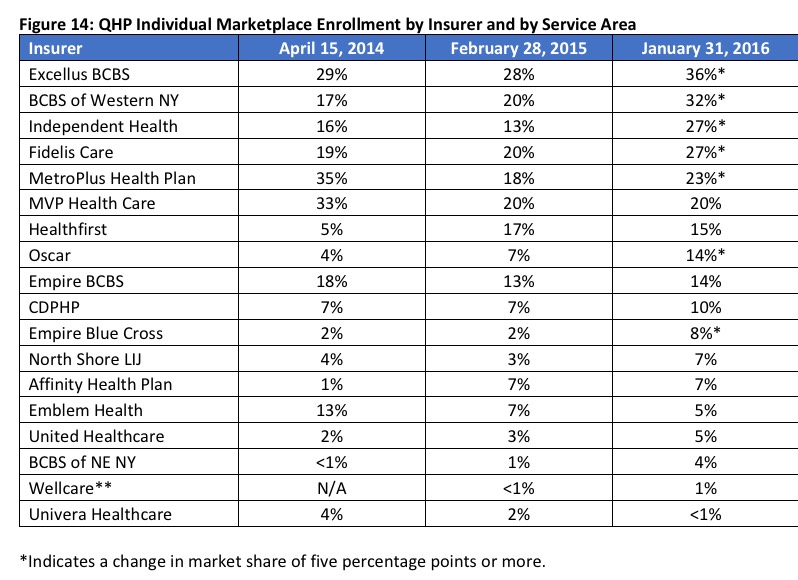

They also include a table showing how the market share of each carrier has shifted around from year to year, which is handy:

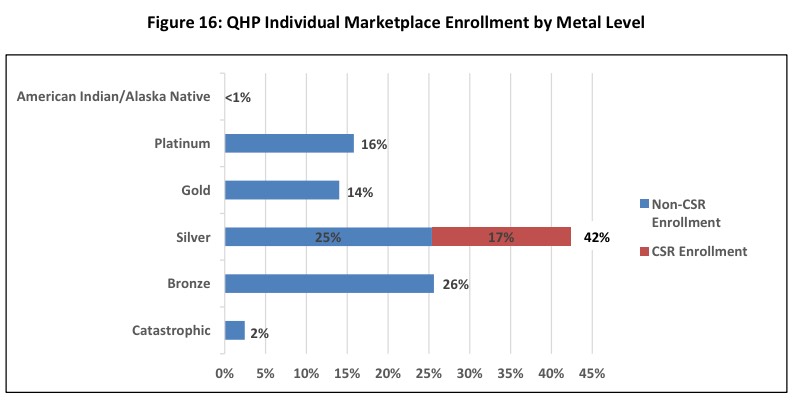

They also have a Metal Level graph which does a nice job of separating out Silver plans by CSR and non-CSR enrollment:

For fans of standardizing the exchange QHPs (including myself and Richard Mayhew), this should be of note:

Thirteen of the 15 individual Marketplace insurers elected to offer one or more non-Standard plans in 2016. Fidelis and EmblemHealth insurers offer only standard plans. As of January 31, 2016, 63 percent of consumers enrolled in standard QHP plans, and 37 percent enrolled in Non-standard QHPs, a decrease from last year when 39 percent enrolled in Non-standard QHPs.

Standard plans are a hit. Personally, I'd recommend pushing these as hard as possible (and potentially even making them mandatory).

There's a bunch more info about standalone Dental plans, about Navigators/Agents/Brokers, etc. as well.

SHOP (Small Business Marketplace):

New York has 13,224 individuals enrolled in exchange-based SHOP plans this year. I don't see hard SHOP enrollment numbers very often, so this is handy info to have.

Anyway, there's a whole mess of other info included in the report; check it out!

Advertisement